- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

How to Use Your Critical Illness Insurance Payout Wisely: A Practical Planning Guide for Canadians (2026)

By Harpreet Puri

CEO & Founder

- 11 min read

- December 22nd 2025

SUMMARY

A practical roadmap for Canadians on using a Critical Illness Insurance payout wisely, covering medical gaps, income protection, recovery planning, and long-term stability. The discussion includes Critical Illness Insurance Canada options, key benefits, coverage details, and how to assess Critical Illness Insurance claims while comparing Critical Illness Insurance quote online choices to stay protected.

Introduction

One huge diagnosis, and everything is different in an instant. Estimates from the Canadian Cancer Society show that almost half of us will be affected by some form of cancer in our lifetimes. The Canadian Institute for Health Information (CIHI) has also found that thousands of Canadians end up experiencing a heart attack or stroke annually, and out-of-pocket payments for medical care have increased as provincial Health Insurance doesn’t cover new treatments, consultations with specialists or rehabilitation programs comprehensively.

This is what Canadian LIC sees on a daily basis: clients who are making a Critical Illness Insurance Canada claim, and suddenly they get their Critical Illness Insurance payout, which they never expected to be using so soon! When that tax-free sum arrives, it’s not just money. It’s protection. It’s a breathing room. It’s a reset button when life seems to be spinning out from underneath you.

But here’s the part most people don’t know:

The payout is only as strong as the plan it’s attached to.

“I’ve learned from working with Canadians on thousands of Critical Illness Insurance benefits, Critical Illness Insurance Coverage reviews, and Critical Illness Insurance claims that it’s the moment when the deposit drops when advice is most important,” adds Mr. Wolfenden. And if you’re shopping for a Critical Illness Insurance quote online, the reason is never far away — protection with purpose.

Let’s show you how to make sure these Canadians who turned 65 in 2026 will be able to spend their lump sum with clarity and confidence.

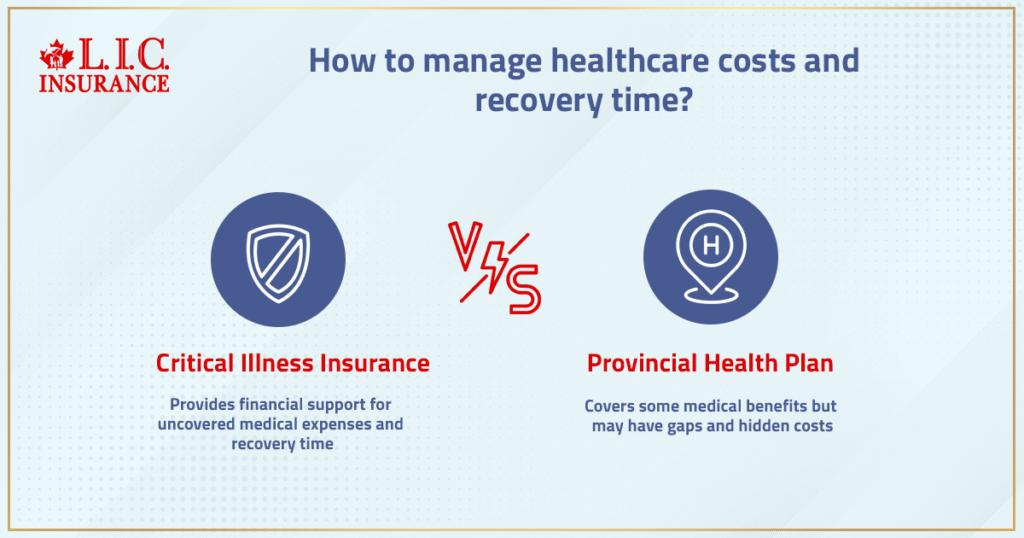

Why A Critical Illness Payout Matters More In 2026

Canada’s health care was robust, but even a robust system has its limits. It’s a vast menu of medical benefits that will soon cover some, but far from all, so-called “low complexity” conditions that once only privileged patients could access. And the covered treatments also come with hidden medical expenses: travel to find services, drugs not on formularies, private diagnostic tests and home-based recovery gizmos.

For that patient, a Critical Illness Insurance Policy is a lifeline since the payout can bridge these gaps. It frees up better decision-making and eases the financial burden when a serious health diagnosis or illness strikes.

In 2026, prescription costs and therapies are continuing to rise, and more families are having to cough up out-of-pocket dollars for services not covered by the provincial health plan. When Canadians get a tax-free lump sum, they are buying time — time to recover, time to have their questions answered and time to rebuild their lives.

That’s why comparing your Critical Illness Insurance cost, finding out what is on your critical illness ISA claims list, and working through some of the things listed today is more important than ever.

Understanding Your Critical Illness Coverage Before Making Decisions

For each critical illness policy, we need to get them to explain exactly what the covered illness is, the covered condition is and what severity it needs to be. Some even have early-stage Critical Illness Insurance Coverage for some cancers, such as blood cancer in its early stages, and other advanced diagnoses such as kidney failure, major organ transplants or specified severity heart conditions. However, some are not covered. Learn which of the cancers are not covered by critical illness insurance.

Canadians frequently wonder why two policies providing the same coverage have different prices. It’s basic — your medical history, age, how you live and whether you engage in risky behaviours factor into how high a premium the insurance company assesses.

Knowing if your diagnosis is considered a covered critical illness, another severe health condition, or a severe health condition will have an impact on how fast we can move your claim along.

Enter Canadian LIC. We decipher the fine print, so you don’t have to.

What Happens When A Lump Sum Payout Arrives

A lump sum benefit is there when you need it most.

This tax-free, lump-sum payout is where the power resides.

It is overwhelming first that most families feel: joy, fear, relief and uncertainty braided together.

It’s a godsend, a living benefit, but with no guidance, that same lump sum payment can vanish quicker than you think.

Ours is to take that feeling and turn it into direction.

How Critical Illness Insurance Works During A Crisis

If you are wondering how Critical Illness Insurance works, it is not complicated at all.

It offers immediate financial security when you’re going through one of the darkest times of your life.

A claim can be made after the expiration of those waiting and survival periods, which are typically built into the policy. After those conditions are satisfied, the insurer authorizes payment.

That could be before your Health Insurance kicks in, or when the government program you qualify for doesn’t quite cover what you need. For many, the payout helps cover unforeseen costs, provides time to coordinate life or Disability Insurance Coverage or can take care of treatment, unlike life insurance, which only generates a death benefit.

We help our clients understand how all the moving parts work together — especially when a critical illness insurance plan and disability insurance are in play.

Step 1 — Cover Immediate Medical Gaps And Additional Expenses

This is the first priority.

From co-payments to particular treatments, there are added costs immediately. What in Brazil are serious matters: diagnostic medical examination, post-operation medication, the journey to a specialist or therapies outside the government’s list.

Many believe that’s what government health care would cover — and they’d be wrong, especially when you’re dealing with complex treatments, rare drugs or intricate procedures.

This is also where the payout comes into play.

It bridges the gap of Health Insurance, prevents you from leaning on loans and treatment delays.

Step 2 — Replace Lost Income And Stay Financially Stable

A major diagnosis often results in months of being out of work.

The payout can offer relief for lost income, expenses that have increased from month to month, school fees, groceries or mortgage payments. It shields your household from a significant financial burden in the event of a catastrophic diagnosis, medical condition or illness.

Recovery is always derailed by concern about the bills.

When a client sits with us, we outline a basic income-replacement plan so that they can really go home and start healing rather than hustling.

Step 3 — Build A Short-Term Income Plan With Your Living Benefit

Part of the payout should be allocated to sustain your next six to twelve months.

This is how the living benefit is at its best.

It complements current coverage, provides for daily expenses and fills the void until disability or workplace benefits kick in.

We compute spending habits, we calculate the amount of Critical Illness Coverage premiums you might still be paying, and we look at how well your Critical Illness Insurance lump sum works within a complete critical illness plan or a stand-alone Critical Illness Insurance Policy.

Step 4 — Secure Medium-Term Stability And Protect Your Recovery

When the pressure is off, we aim for stability.

“It’s only now that you can weigh the actual value of your remaining capital in Critical Illness Insurance. Depending on your diagnosis, you may also need long-term care planning, fiduciary investments, and special support.

Your payout continues to grow securely, but is now accessible thanks to insurance advisors.

We explore your medical history and assist with making sure it blends with your retirement savings plans, and check to make certain all of your insurance carriers and the insurance companies will be responsive to your changing reality.

Step 5 — Prepare For Long-Term Needs And Protect Your Future

Long-term planning often gets ignored.

But when the diagnosis is serious and the illness acute, everything changes.

We work with clients to establish reserves, manage pre-existing medical conditions, review obligations and ensure they keep the financial value of their tax-free payout.

Your future counts, even when it feels up in the air.

We help make it steady.

Step 6 — Strengthen Your Safety Net With Disability Insurance

A lot of Canadians don’t understand how disability insurance and Critical Illness Coverage work for us together.

They both protect income, but they do so in different ways. A critical illness insurance benefit is accelerated. Disability payments arrive over time. Together, they cover your family, so the financial burden isn’t as great; you have income ongoing to support your family, and people don’t have to worry about taking a long time off work.

Our advisers assist with the integration of both, so they work together rather than get in each other’s way.

Step 7 — Review Your Existing Policies And Get A Critical Illness Insurance Quote Online

This is where clarity returns.

When the payout is set, we rethink everything in your protection plan. Include Critical Illness Insurance on the list of things you occasionally have to buy again. Sometimes you need to upgrade.

However, many families request a Critical Illness Insurance quote online, particularly when they need to make sure they have Critical Illness Insurance for the future and don’t know which partner will offer the best deals on Critical Illness Insurance.

We keep you covered no matter what, even if you make a claim. Canadians need the time and the guidance to rebuild wisely.

Early Stage Critical Illness Claims: What Canadians Need To Know In 2026

Policies differ widely here. Some help in early-stage critical illness conditions, such as early-stage blood cancers, while others mandate advanced diagnosis.

Waiting period, survival period and the type of covered condition make a difference.

Here’s where your policy’s fine print can mean the difference between whether a claim is covered, so you’ll want to know this information ahead of time.

We decode these specifics so that families are not left guessing in the most difficult times.

How Insurance Providers Support You Through A Critical Illness Claim

We go to the insurance companies ourselves and deal with all the minutiae involved with each company.

The pace at which a case is resolved is dependent on your health history, pre-existing conditions and the protocols of the insurance company.

We want to take that burden off your shoulders and allow you to concentrate on treatment instead of paperwork.

This is the value of a good DRE advisor.

Calculating Your Budget After A Lump Sum Payout

Budgeting after a payout feels overwhelming, so we break it down simply:

- Handle urgent needs first

- Build income stability

- Prepare for unexpected expenses

- Protect your lump sum from erosion

- Manage out-of-pocket expenses

- Keep room for additional expenses

- Reduce financial stress and monthly expenses

This roadmap keeps families grounded and confident.

How To Build A Recovery-Friendly Financial Plan With A Survival Period In Mind

Your plan must respect the survival period, your treatment plan, and your evolving medical needs.

We help navigate long-term therapy, post-treatment finances, and ensure protection stays in place.

Recovery is unpredictable — your plan shouldn’t be.

Where Canadian LIC Supports You During And After Your Critical Illness Journey

This is where our history becomes your foundation.

When illness insurance comes to Canada, clients feel their world contract and are spending time in hospital rooms, examining test results and asking questions that never end.

We pore over documents with families, sort through priorities, review documents, re-evaluate goals and assist families in regaining control.

You’re not getting just advice — you get a partner who knows what this moment really is.

Final Guidance For Using Your Critical Illness Insurance Payout Wisely

Payout is only powerful when it’s purposeful.

At a time when the world feels thrown off balance, the right plan manages to feel steady, clear and gives you space to restore on your own terms.

We not only explain your policy.

We help you live through it.

And we stand with you as you construct your life brick by brick, led by dignity and strength.

More on International Student Insurance

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

The payout of a Critical Illness Insurance Policy can allow families to change long-term plans without being hurried into decisions that no longer work for them. That includes keeping other commitments you have, such as saving for education or travelling to treatments, even if your priorities change after a devastating health diagnosis. The payout, properly channelled, can become a means to safeguard your future rhythm and cover the kinds of care that turn up as you go along. And you remain in full control because the money arrives as a tax-exempt, lump sum, available when life changes again.

Health events can shift your view of risk, so taking a look at the Critical Illness Insurance you’ve got now helps ensure you’re not left exposed in the future. There are modified options an insurer can offer after a claim based on your medical history, but the right advisor makes those choices work. This review also helps to coordinate your coverage with your remaining needs — for income, recovery time and lifestyle changes. For a lot of families, it’s the step that shields them from nasty surprises after serious illness.

Yes — a Critical Illness Insurance Policy is designed to complement what provincial healthcare already provides by giving you choice where the system has limitations. When your stability is disrupted by a covered illness, the payout allows you to pick better recovery environments or travel to different specialists, doctors, or gain access to therapies that aren’t part of the government lists. It occupies the distance between what is medically needed and what actually helps you heal. It is for that flexibility that families appreciate Critical Illness Insurance Canada now more than ever.

Every insurer has some kind of scaffolding around diagnosis, timing and the defined covered condition, but true clarity comes from how much evidence the insurance company tabulates. They consider specialist reports, the medical exam, and whether the condition qualifies as severe under the policy. A good consultant will help guide you through the process by presenting your information in an order that underwriters can easily grasp. It minimizes delay, and it makes the claim stronger without creating pressure in valuing a serious health issue.

This form of lump sum benefit is meant to serve as a financial cushion when life throws you a curveball — whether it’s keeping your household on track or altering long-term plans. It provides families with a grounding force while they adjust to changes in lifestyle brought on by critical illness or long recovery periods. Many customers apply a portion to protect future plans, such as saving for retirement or supporting dependents through an uncertain period. With the proper structure, that sum quietly protects you from insidious financial stress that accrues hour by hour, day by day.

Each kind of protection addresses different financial risks, and together they enhance your capacity to absorb the loss of income if recovery ends up taking longer than predicted. Disability insurance maintains a monthly cash flow, and critical illness protection fills larger gaps associated with changes in life. This style of working can keep you on an even keel when a severe illness or heart attack delays how fast you bounce back to full strength. Advisors commonly design the two layers to operate well without replicating one another.

Absolutely — there are smarter ways to structure your protection than to just let time take its course when it comes to premiums on Critical Illness Insurance after a big claim, or life change. Certain insurers modify coverage options; others propose new terms that correspond with your fresh state of health. This practice ensures that you aren’t forced to pay for a part of a plan that no longer suits your lifestyle. And it helps ensure that even as your priorities change, the policyholder can continue to afford to keep your critical illness policy in force.

As with all other types of insurance, the true value comes from how well it fits your life, not how much you’ll pocket if you end up filing a claim. Counting on Critical Illness Insurance is no different. Regular check-ins can also keep your policy in sync with new risks, updated financial goals and evolving treatment options. This allows your plan to remain current as advances in medicine add costs or alternative therapies. We assist clients in maintaining that balance so that protection remains meaningful for the long term.

We know most people are overwhelmed, so we work hard to demystify each step of the process — from selecting a Critical Illness Insurance Plan to common questions about pre-existing conditions. Many families are after coverage that preserves them and their loved ones, both in terms of their emotions and financially, having witnessed a loved one suffer from cancer or some other serious health issue. The point is to craft a plan that honours your actual fears and future obligations. And then, having been issued, that policy comes to be a foundation you can count on.

Doing comparisons online can teach you how various insurance companies organize the benefits, waiting period and lump sum aspects. It tells you whether the newer plans offer wider coverage, better pricing or more flexible recovery benefits. Some will find that the updated policies now offer early-stage coverage for critical illness or longer lists of covered critical illnesses. It’s a clever way to ensure your protection is up to date, competitive and matches what your life looks like today.

Key Takeaways

- A Critical Illness Insurance payout becomes most powerful when paired with structure.

The tax-free amount gives Canadians breathing room, but its real value comes from knowing how to direct it toward recovery, stability, and long-term security. - Critical Illness Insurance Canada fills the financial gaps that provincial healthcare cannot.

Modern treatments, travel for care, and recovery needs often fall outside public funding, making coverage essential for reducing sudden strain after a severe health diagnosis. - Using the lump sum wisely means more than paying medical expenses.

It supports income replacement, future flexibility, and long-term commitments—helping families stay grounded during months of uncertainty. - Reviewing Critical Illness Insurance benefits after a claim keeps your protection relevant.

A major diagnosis can reshape your financial picture, so reassessing coverage, insurance providers, and updated options ensures you remain protected moving forward. - A well-planned approach protects both health and finances during recovery.

From handling out-of-pocket costs to aligning with retirement savings goals, the smartest plans keep liquidity first while ensuring long-term strength. - Disability insurance complements Critical Illness Insurance work strategies.

Both play different roles in managing lost income, and combining them creates a more powerful safety net when recovery takes longer than expected. - Getting a Critical Illness Insurance quote online helps you compare evolving coverage options.

Policies change, providers update definitions, and benefits expand—comparison keeps your protection current, affordable, and aligned with your real risks. - Canadian LIC’s role becomes crucial when life feels unsteady.

Advisors help turn a lump sum into direction, clarity, and confidence—guiding families through decisions that matter most during a serious illness.

Sources and Further Reading

- Canadian Cancer Society – Cancer Statistics: https://cancer.ca/en/research/cancer-statistics Canadian Cancer Society+1

- Canadian Institute for Health Information – Patient Cost Estimator (Hospital Stay Costs): https://www.cihi.ca/en/patient-cost-estimator cihi.ca+1

- Statistics Canada – Number and Rates of New Cases of Primary Cancer: https://www150.statcan.gc.ca/t1/en/tv.action?pid=1310011101 Statistics Canada

- Canadian Cancer Statistics 2017 (Government of Canada) – https://www.canada.ca/en/public-health/services/chronic-diseases/cancer/canadian-cancer-statistics.html Canada

Feedback Questionnaire:

“How Are You Managing Your Critical Illness Insurance Payout?”**

We truly want to understand what Canadians are going through during one of the most stressful chapters of life. Your answers help us improve guidance, tools, and support for families navigating a Critical Illness Insurance payout and the planning that follows.

IN THIS ARTICLE

- How to Use Your Critical Illness Insurance Payout Wisely: A Practical Planning Guide for Canadians (2026)

- Why A Critical Illness Payout Matters More In 2026

- Understanding Your Critical Illness Coverage Before Making Decisions

- What Happens When A Lump Sum Payout Arrives

- How Critical Illness Insurance Works During A Crisis

- Early Stage Critical Illness Claims: What Canadians Need To Know In 2026

- How Insurance Providers Support You Through A Critical Illness Claim

- Calculating Your Budget After A Lump Sum Payout

- How To Build A Recovery-Friendly Financial Plan With A Survival Period In Mind

- Where Canadian LIC Supports You During And After Your Critical Illness Journey

- Final Guidance For Using Your Critical Illness Insurance Payout Wisely

Sign-in to CanadianLIC

Verify OTP