- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

How The RESP And Related Benefits Work Together To Maximize Your Child’s Education Savings

By Pushpinder Puri

CEO & Founder

- 11 min read

- September 11th, 2025

SUMMARY

The blog explains how a Registered Education Savings Plan in Canada supports your child’s post-secondary education. It covers RESP benefits, RESP contributions in Canada, Canada Education Savings Grant, RESP grant eligibility and limits, and how government grants, RESP savings, and investment income grow tax-deferred to fund your child’s future education across trade schools, universities, and apprenticeship programs.

Introduction

Every dollar saved early has a compounding impact on your child’s education. We guide thousands of families through every step of using a Registered Education Savings Plan in Canada. The RESP is not just a savings tool. It is a government-backed system built to support your child’s future education.

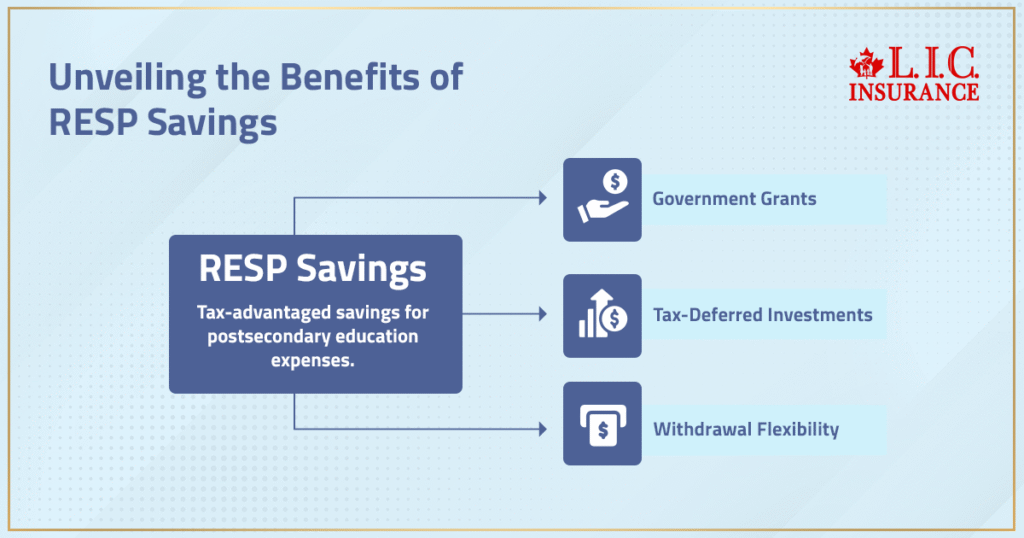

Why RESP Matters For Your Child's Education

Postsecondary education is expensive. The price of tuition, housing, and school supplies continues to go up, whether your little one decides to go to college, university, trade schools, apprenticeship programs, or any other. We need more school outlets. RESP savings are like a tax scheme – except that it is all perfectly legal – to increase your education savings while lowering your tax bill.

You get more than a parking spot for money. You get government grants, investments that are tax-deferred, and flexibility in how you withdraw, in ways pertinent to your family’s needs.

Understanding The Education Savings Plan RESP Structure

The RESP is like a tax-sheltered investment account. You contribute money. That money is generating income and growing tax-deferred. Your child enrolls in full-time or part-time programs at a qualifying educational institution, and money is withdrawn as education assistance payments.

Withdrawals are taxed in your child’s name. Because students tend to be low-income or no-income, they tend to pay little or no income tax on RESP withdrawals.

There are three types of RESP accounts:

- Individual RESP: One child, one subscriber.

- Family RESP: For one or more beneficiaries who must be related by blood or adoption.

- Group RESP: Offered by dealers who pool savings across multiple children.

RESP Contributions In Canada And Key Limits

The maximum RESP contribution per beneficiary is $50,000. There is no annual contribution limit; however, the contribution room grows by $2,500 each year to qualify for grants.

There is no tax deduction for RESP contributions. However, investment income grows tax deferred, and government grants add extra value.

Keep these contribution points in mind:

- You do not receive a tax refund for contributing to an RESP.

- Income earned inside the plan is not taxed until withdrawal.

- If you exceed the maximum RESP contribution, penalties apply.

RESP contributions can come from family members, not just parents. Grandparents, guardians, or siblings can open a plan or contribute to an existing one.

How The Canada Education Savings Grant Works

The Canada Education Savings Grant is the core government match for RESP contributions. It rewards families who save early and regularly.

Here’s how it works:

- The basic grant is 20 percent of the first $2,500 contributed annually.

- That equals $500 in grant money each year.

- The lifetime maximum CESG per child is $7,200.

- If you miss a year, you can catch up one year at a time.

Low- and middle-income families may qualify for additional grants:

- 10 percent or 20 percent extra, depending on family income.

- CESG top-ups apply to the first $500 contributed each year.

The RESP grant eligibility and limits depend on family income, contribution activity, and the age of the child. The government stops giving CESG at age 17.

How The Canada Learning Bond Adds More Value

The Canada Learning Bond is another federal grant for children born in 2004 or later whose families meet income requirements.

Key facts:

- No contribution is required to receive the bond.

- $500 is deposited in the first year of eligibility.

- $100 is added annually until age 15.

- The total can reach up to $2,000.

This benefit is especially helpful for low-income families building education savings.

Provincial Governments Add Their Own Grants

In addition to federal grants, some provincial governments offer their own RESP incentives. Examples include:

- Quebec Education Savings Incentive (QESI)

- British Columbia Training and Education Savings Grant (BCTESG)

- Saskatchewan Advantage Grant for Education Savings (SAGES)

These additional grants provide more RESP benefits when you contribute through a qualified financial institution.

Contribution Strategies For Maximum RESP Benefits

To maximize grant money and RESP savings, you need a consistent contribution plan.

Follow these practical tips:

- Contribute $2,500 per year to receive the full $500 CESG.

- If you missed past years, contribute $5,000 to receive $1,000 in grant money.

- Avoid overcontributing. The lifetime maximum per child is $50,000.

- Start early to give your investment income more time to grow tax-deferred.

Even if your budget is tight, start with what you can. Small monthly deposits still earn interest and compound over time.

Family RESP And Planning For Multiple Children

If you have more than one child, a family RESP helps streamline contributions and maximize benefits.

Here’s why it works:

- One plan, multiple children.

- You control how RESP funds are allocated.

- If one child decides not to pursue post-secondary education, the money stays in the plan and supports another child.

- Contribution flexibility within the family unit.

Keep in mind that the Canada Education Savings Grant limits apply per child, not per plan. Grant tracking must be done separately for each child’s RESP.

What Happens When Your Child Decides To Use The Funds

When your child starts a full-time program or part-time programs at an approved educational institution, you request educational assistance payments.

Here’s how withdrawals work:

- Educational assistance payments include grant money and income earned.

- These are taxable to the student, not to you.

- Your original contributions can be withdrawn tax-free.

Your child’s RESP must be used for a qualified post-secondary program. This includes:

- University or college degrees

- Trade schools

- Apprenticeship programs

- Some foreign institutions

Your child can attend school anywhere in Canada or internationally, as long as the institution is approved.

RESP Withdrawals And Tax Implications

Understanding RESP withdrawals is critical for tax planning.

- Educational assistance payments are taxable income for your child.

- If your child has no other income, they often owe no income tax.

- If your child does not attend school, grant money is returned to the government.

- Income earned can be transferred to your Registered Retirement Savings Plan, up to $50,000, if you have enough contribution room.

RESP withdrawals must be documented. Keep receipts for tuition and school supplies to support the claim.

Investment Options And Risk Considerations

You are allowed to invest your RESP funds in various products based on your risk tolerance. Options include:

- Mutual funds

- GICs

- Bonds

- ETFs

Consult a financial advisor to tailor the RESP investment strategy to your child’s age, your savings goals, and market outlook.

Younger children allow for a longer investment horizon. Older children require safer, short-term investments.

What If Your Child Does Not Pursue Post-Secondary Education

If your child decides not to attend an educational institution, the RESP account remains open for up to 36 years.

Options include:

- Use RESP funds for another child if in a family plan.

- Transfer income earned into an RRSP (up to $50,000), if you have enough contribution room.

- Withdraw contributions tax-free.

- Pay income tax on earnings plus a penalty.

You cannot keep grant money. It must be returned to the Canadian government if the child is not an eligible beneficiary.

Key Benefits Of Using a RESP With Canadian LIC

We support families in making smart RESP decisions. Here’s what we offer:

- RESP account setup and contribution planning

- Ongoing reviews to track RESP contributions and maximize annual grants

- Family RESP coordination for multiple children

- Education savings tracking and advice

- Support during RESP withdrawals and education assistance payments

We help you avoid missed grants, overcontributions, and unnecessary taxes.

Why RESP Works Better Than Regular Savings

A regular savings account lacks grant support, tax deferral, and income-shifting. With a Registered Education Savings Plan in Canada:

- Investment income grows tax-deferred.

- Grants add thousands in bonus value.

- Withdrawals are taxed in the hands of the student, often tax-free.

Education savings plans are better structured through an RESP than through an unregistered account.

How To Start Contributing To An RESP

Getting started is simple. You need:

- Your child’s SIN

- Your own SIN

- A valid ID

- A decision on plan type: individual plan or family plan

Contributing to an RESP with us means you are guided through RESP grant eligibility and limits. We help you structure annual contributions and avoid missing government grants.

We review your family income and optimize strategies for additional grants, Canada Learning Bond eligibility, and provincial benefits.

Make The Most Of Government Grants Before Deadlines

Government grants have limits. Your child stops receiving CESG after age 17. Some grants require RESP contributions from the previous years. To secure all RESP benefits, contribute before those cutoffs.

Stay informed on:

- Annual contributions

- Maximum contribution limits

- Lifetime maximum CESG and CLB

- RESP withdrawals and income tax impacts

Let us help you avoid a lost opportunity. We monitor every child’s RESP for contribution room and grant tracking.

Education Savings Plans Need Professional Guidance

RESP rules are strict. Deadlines matter. Grant eligibility depends on proper contributions and accurate documentation.

Our team supports families like yours with:

- RESP grant applications

- Tracking income earned and grant money

- Calculating lifetime contribution limits

- Planning RESP withdrawals

- Coordinating plans across multiple children and family members

Education savings plans work best when managed by a licensed advisor with experience. Our specialists help you align your financial goals with RESP strategies built for your child’s future.

More on Registered Education Savings Plan

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

You’re allowed to open an RESP at any time before the beneficiary reaches 18 years of age. But if you want to get RESP benefits, such as the Canada Education Savings Grant the government may offer, you’ll have to top up your contribution by the end of the year your child turns 17. By beginning earlier, you have the opportunity to grow your education savings over time, become eligible for a number of government grants, and you can be more strategic in the way you contribute.

Yes. RESP contributions in Canada are flexible. You control the amount and frequency. Even if you pause due to family income changes, you don’t lose grant eligibility permanently. You can catch up later and still reach the lifetime maximum contribution for your child’s RESP.

RESP savings are permitted for full-time or part-time studies at some international schools. The school should be in the list of DLI, which is also important according to the Canadian government. Families should verify qualifications before taking a withdrawal from education assistance accounts.

If you are able to make contributions to your child’s RESP, withdrawals from the plan are taxed in your child’s name. They are taxable income in the hands of the student who received an educational assistance payment. Your own income tax return isn’t affected, even if you are the subscriber (donor) or contributor to the RESP.

Yes, through a family RESP. This plan can cover multiple children as the named eligible beneficiary, if they are related to you (the account owner) as a brother or sister, or are adopted. It means this is how grant money can be kept in the family, even if one of your children doesn’t decide to go to college.

If your child does not attend or leaves a post-secondary school, they don’t lose the money put into RESPs. You can keep the plan open or move the money if you are on a family plan. Your government grants have to be given back, but any income you made could be transferred to your Registered Retirement Savings Plan.

Yes. Only a post-secondary educational institution is eligible to receive withdrawals from an RESP. This category encompasses universities, colleges, trade schools, and apprenticeship programs. Eligible provisions for Programs: Each Program shall comply with the eligible minimum duration and structure in accordance with RESP grant eligibility.

You can change your investment options in a RESP depending on your child’s age and your risk tolerance. As the child’s future education nears, a financial adviser can help steer you from high-growth options to more conservative ones. It’s all about timing and risk matching.

Key Takeaways

- A Registered Education Savings Plan in Canada helps families save for a child’s post-secondary education with tax-deferred investment income and RESP benefits.

- The Canada Education Savings Grant provides 20% on annual RESP contributions in Canada, up to a lifetime maximum of $7,200 per child, with eligibility tied to family income.

- The Canada Learning Bond adds up to $2,000 for eligible low-income families, with no need to contribute to access the grant money.

- A family RESP supports more than one child and allows flexible allocation of RESP savings among family members if one child decides not to attend a post-secondary program.

- RESP withdrawals for education assistance payments are taxable in the student’s hands, usually resulting in little to no income tax due to low student income.

- Contributions grow tax deferred, but original contributions are withdrawn tax-free, and income earned may be transferred to an RRSP if RESP funds go unused.

- Government grants and additional grants from provincial governments can further increase total education savings, especially when used with consistent annual contributions.

- RESP accounts must be used for programs at eligible educational institutions, including trade schools, colleges, universities, and apprenticeship programs.

- Contribution limits include a $50,000 lifetime contribution limit per child and the need to avoid overcontributions to prevent penalties.

- A financial advisor can help align RESP strategies with your child’s future education plans, ensuring all grant eligibility rules and tax implications are managed correctly.

Sources and Further Reading

Official Government Resources

- Government of Canada – RESP Overview

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/registered-education-savings-plans.html

Provides comprehensive details on how the Registered Education Savings Plan in Canada works, including types of RESP accounts, contribution rules, and tax treatment. - Canada Education Savings Grant (CESG)

https://www.canada.ca/en/employment-social-development/services/learning-bond/education-savings.html

Explains Canada Education Savings Grant eligibility and limits, the 20% matching structure, and additional grants for low- and middle-income families. - Canada Learning Bond (CLB)

https://www.canada.ca/en/employment-social-development/services/learning-bond.html

Details on CLB eligibility, automatic grants, and how to apply without contributing to the RESP. - Employment and Social Development Canada (ESDC)

https://www.canada.ca/en/employment-social-development.html

Home page for all federal grant programs related to education savings, including RESP benefits, savings tips, and parent outreach tools.

Additional Resources

- Financial Consumer Agency of Canada – RESP Guide

https://www.canada.ca/en/financial-consumer-agency/services/education-savings/resp.html

Provides actionable advice for families planning RESP contributions in Canada, including RESP savings calculators and planning tools. - Provincial Government Grants

- British Columbia: https://www2.gov.bc.ca/gov/content/education-training/k-12/support/bctesp

- Quebec: https://www.revenuquebec.ca/en/citizens/tax-credits/quesi/

- Saskatchewan: https://www.saskatchewan.ca/residents/education-and-learning/parents-and-guardians/sages

Each page includes program-specific details and how to combine provincial grants with the RESP and Canada Education Savings Grant.

- Universities Canada – Approved Institutions List

https://www.univcan.ca/universities/member-universities/

Helpful for verifying if a post-secondary school or trade school qualifies under RESP withdrawal rules.

Feedback Questionnaire:

IN THIS ARTICLE

- How The RESP And Related Benefits Work Together To Maximize Your Child’s Education Savings

- Why RESP Matters For Your Child's Education

- Understanding The Education Savings Plan RESP Structure

- RESP Contributions In Canada And Key Limits

- How The Canada Education Savings Grant Works

- How The Canada Learning Bond Adds More Value

- Provincial Governments Add Their Own Grants

- Contribution Strategies For Maximum RESP Benefits

- Family RESP And Planning For Multiple Children

- What Happens When Your Child Decides To Use The Funds

- RESP Withdrawals And Tax Implications

- Investment Options And Risk Considerations

- What If Your Child Does Not Pursue Post-Secondary Education

- Key Benefits Of Using a RESP With Canadian LIC

- Why RESP Works Better Than Regular Savings

- How To Start Contributing To An RESP

- Make The Most Of Government Grants Before Deadlines

- Education Savings Plans Need Professional Guidance

Sign-in to CanadianLIC

Verify OTP