- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Corporate-Owned Life Insurance In Canada: Benefits And Tax Guide For Business Owners

By Harpreet Puri

CEO & Founder

- 13 min read

- April 8th, 2026

SUMMARY

Corporate-owned Life Insurance in Canada supports business owners with strategic protection, long-term tax advantages, and efficient access to the Life Insurance death benefit. The structure strengthens succession plans, enhances cash value growth, and allows corporations to manage wealth through the Capital Dividend Account while maintaining flexible planning across changing corporate needs.

Introduction

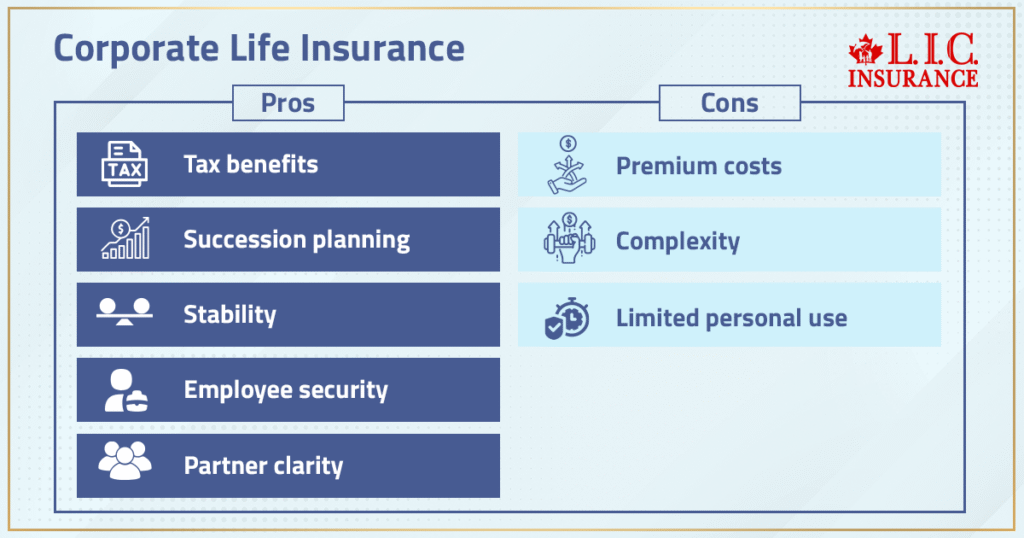

A solid company stands on the shoulders of people—owners, partners, key employees who bear the load of operations, relationships and long-term vision. We have met with hundreds of business owners who have literally built something from nothing, but also wound up in the situation where they were concerned that 1 event in life could potentially destroy it all. When most of a family’s wealth is tied up in a privately held corporation, the business owner depends on that entity to safeguard their loved ones. And this is where corporate-owned Life Insurance becomes one of the handiest instruments around.

A recent release from Innovation, Science and Economic Development Canada reports that 98.1% of employer businesses in the country are small businesses, many staffing primarily one or two people. In a world where businesses rely on a key person or founder, that risk exists, and a company’s cash flow, long-term contracts and corporate investments can all be shaken by even a temporary disruption. Company-owned Life Insurance—constructed purposely and written in conjunction with the Income Tax Act—fills that void, allowing the business to protect itself against such volatility while benefiting from longer-term tax advantages, wealth-creation potential and financial protection strategies.

Corporate-Owned Life Insurance In Canada: Benefits Tax Guide For The Business Owner

Yet when we sit down with Canadian business owners, many feel a combination of pride and pressure. They built something meaningful — but such success carries responsibilities: Employees who rely on their plans and guidance, families that count on the stability of the corporation they lead, partners who require clarity about what comes next, as such corporate Life Insurance for business owners is considered a key tool in dealing with these obligations.

This sort of planning allows for the corporation, and not the individual, to own the policy. The company pays the premiums; you receive the Life Insurance death benefit, along with access to tactical tax benefits that are nonexistent when using a personal insurance policy. If structured correctly, it can also minimize tax liability, insulate the company from abrupt upheavals and provide for long-term succession.

A strong COLI strategy supports:

- Business continuity during a crisis

- Financial protection of the corporation and its shareholders

- Tax advantages through the Capital Dividend Account

- Future planning for family members and employees

- Corporate stability during ownership transitions

The end goal is simple: strengthen the business while ensuring the people behind it stay protected.

What Is Corporate-Owned Life Insurance In Canada?

Corporate-Owned Life Insurance isn’t complicated when explained the right way. The corporation owns the policy, pays the premiums, and receives the insurance proceeds. The life insured—also called the insured person or person insured—is usually a shareholder, partner, or key employee whose loss would create a financial impact.

Here’s the core structure:

- The policy owner is the corporation.

- The corporation pays COLI premiums using after-tax corporate funds.

- The business receives the Life Insurance proceeds received at the time of the death claim.

- The arrangement sits inside the corporate ownership structure, not the personal estate.

- The benefit supports both operational needs and long-term planning.

Since the company owns Life Insurance Policies directly, the coverage is in line with corporate strategy: tax planning, executive benefits, business continuity and wealth creation. And when you contrast the life that is corporate-owned versus personal coverage, the corporate structure provides for some special tax advantages that personal insurance could only dream of.

How Corporate-Owned Life Insurance Differs From Personal Coverage

A Personal Life Insurance Policy pays a tax-free benefit directly to individual beneficiaries. It protects families, but doesn’t solve corporate issues like share redemption, executive continuity, or business cash flow.

Owned Life Insurance at the corporate level offers distinct advantages:

- The insurance policy becomes a corporate asset.

- Insurance proceeds enter the corporation first.

- These funds can support buyouts, operations, or tax-free distributions through capital dividends.

- The corporation—not the individual—decides how to use the net proceeds.

This setup is especially beneficial for private corporations where most family wealth sits inside the company. It lets business owners combine insurance planning with succession planning, business continuity, and future taxation strategies.

Capital Dividend Account And Corporate-Owned Life Insurance

For business owners, the Capital Dividend Account (CDA) often becomes the biggest financial benefit of a corporate-owned policy. The CDA allows a private corporation to distribute certain amounts to shareholders as tax-free dividends instead of taxable income.

Under CRA guidelines, the CDA receives a credit when a company receives Life Insurance proceeds following the death of the insured person. The calculation is simple:

CDA credit = death benefit – adjusted cost basis (ACB)

This credit is the amount that a corporation may pay to its resident Canadian shareholders as a capital dividend. For entrepreneurs or executives focused on extracting funds as efficiently as possible, this is one of the most potent aspects of the strategy.

Capital dividends will help to eliminate double taxation at death and provide for a clean method that may allow the corporation to make support for families, finish buyouts or continued succession planning. Whether the business is a standalone company or an entity operating under a corporate holding structure (such as those used for wealth planning purposes), the CDA is an important vehicle for removing money from the corporation with little or no tax implications.

Understanding Adjusted Cost Basis And Net Proceeds

The adjusted cost basis, or ACB, of the policy is the total amount contributed by the company to any particular point in time. The ACB gradually decreases each year for the NCPI until the CDA credit accumulates as the policy ages.

So as the ACB decreases in each taxation year, this spread between the death benefit and the ACB widens. That delta is the CDA credit, which can be paid out by the corporation on a tax-free basis.

Now, try to save as much extra cash on withdrawals and policy loans (when they are not necessary), which will help protect the integrity of your policies later for even larger tax-free CDA credits.

Capital Dividend Planning For Private Corporations And Holding Companies

For a single-owner private corporation, CDA planning is straightforward. But many business owners operate in multi-layer structures involving:

- Operating companies

- A holding company

- Multiple private corporations

- Family trusts

- Corporate reorganizations

In these situations, asset flow, shareholder agreements, and ownership structure must be handled carefully to avoid accidental tax consequences, such as:

- Unintended double taxation

- Issues involving non-resident shareholders

- Incorrect corporate ownership of the policy

- A truncated CDA credit due to structural misalignment

Clear planning ensures that insurance proceeds are received by the right entity, at the right time, following all specific rules under the Income Tax Act.

Why Permanent Life Insurance And Participating Whole Life Work Best For Corporate-Owned Life Insurance

We explain to clients that corporate-owned insurance isn’t simply about the cheapest premium. It’s about protecting long-term goals. Permanent Life Insurance—particularly a Participating Whole Life Insurance Policy—delivers stability and corporate liquidity that a temporary contract simply cannot.

Permanent Policies offer:

- Lifetime financial protection

- Growing cash value and potential cash surrender value

- Tax-deferred cash growth inside the policy

- More predictable planning for executives and shareholders

When a corporation purchases Whole Life Insurance, the policy becomes an asset that sits quietly on the balance sheet and strengthens the company’s long-term position. This makes it useful not just for protection but also for balancing risk, planning executive compensation, and maintaining corporate liquidity.

Cash Value, Cash Surrender Value, And Corporate Liquidity

Corporate-owned permanent policies accumulate cash value over time. This forms a resource the company can access if needed through:

- Policy loans

- Collateral assignments

- Surrenders in specific scenarios

Access to cash surrender value can help fund:

- Executive benefits

- Emergency expenses

- Corporate investments

- Short-term liquidity needs

Because permanent policies also include a savings component, the corporation benefits from long-term cash value accumulation that grows without annual tax reporting, as long as the contract meets the exempt rules.

Corporate-Owned Life Insurance For Key Person Insurance And Executive Benefits

Every corporation has people whose absence would create immediate challenges. A founder, a senior executive, a technical specialist—these individuals are the lifeblood of the operation. Key Person Insurance allows the corporation to protect itself from this risk.

The corporation holds Key Person Insurance on:

- Founders

- Senior executives

- Revenue-driving specialists

- Other key employees

If a key person dies, the insurance proceeds offer room to stabilize operations, replace the person, or cover short-term losses. It also helps the corporation maintain business continuity during one of the most difficult periods it could face.

Beyond protection, permanent corporate policies can also support:

- Long-term executive benefits

- Retention programs

- Targeted executive compensation packages

- Performance-based rewards tied to policy values

These strategies help keep top talent engaged and invested in the company’s success.

Corporate-Owned Life Insurance And Buy-Sell Agreements

For corporations with multiple owners, one event can wreak havoc: the death of a partner. Families need money quickly. The remaining partners are looking to retain control. The company will require immediate money to buy the deceased owner’s share.

When properly designed, a buy-sell agreement combined with C-O products adds clarity and certainty.

The corporation receives the death benefit, providing:

- Clean, immediate funding for redemption

- Predictable net proceeds for the deceased owner’s family

- Protection from disputes and forced sales

The agreement ensures succession planning remains intact. Owners know the transition will occur smoothly, without scrambling for financing or risking the company’s stability.

Comparing Term Insurance And Whole Life Insurance Inside The Corporation

Term insurance has its place. It offers pure insurance protection at a lower cost, especially for short-term needs, such as debt coverage or temporary partnership obligations. But it has no cash value and doesn’t arm you for everything. For longer-term strategies centred on wealth transfer, tax planning and succession, Whole Life Insurance is generally the better fit.

When comparing costs, many business owners look at:

- Term Life Insurance rates by age chart Canada

- Life Insurance rates by age chart Canada

Younger insureds pay significantly less for term, but the lack of long-term value makes permanent coverage more strategic for corporate planning. A Life Insurance quote online provides a quick start, but designing a full COLI strategy takes deeper analysis.

Understanding COLI Premiums And Long-Term Net Cost

COLI premiums function differently from personal premiums. They sit on the corporate books, they affect retained earnings, and they pair with long-term tax advantages. Over time, the strategic use of COLI premiums can create far more corporate value than temporary, expiring contracts.

Business owners often evaluate:

- The net cost of permanent coverage

- Potential future tax-deductible borrowing tied to collateral assignments

- The relationship between premiums and future capital dividend opportunities

- How premiums paid align with long-term corporate goals

The outcome is a strategy shaped around stability and tax efficiency, not just short-term savings.

Planning With Holding Companies And Multi-Entity Structures

When a corporation works alongside a holding company or multiple private corporations, corporate-owned policies must be placed carefully. A misalignment can result in unintended tax consequences, reduced CDA access, or inefficient cash flow.

Strategic planning includes:

- Ensuring correct entity ownership

- Managing potential deemed disposition risks

- Coordinating CDA elections across companies

- Evaluating the presence of non-resident shareholders

- Reducing exposure to double taxation

With the right structure, corporate-owned life strategies help move wealth tax-free across entities and support long-term growth for families and shareholders.

Key Considerations, CRA Rules, And A Strong Advisory Team

Every COLI strategy must follow the specific rules of the Income Tax Act. Policies must maintain exempt status to protect tax-deferred cash growth. CRA guidelines influence:

- How the policy’s ACB declines

- How capital dividends are paid

- Whether CDA credits apply fully

- How corporate reorganizations affect taxation

To protect corporate value, we regularly collaborate with your tax advisor, accountant, or legal team. Our job is to ensure the insurance structure supports your broader planning without adding unnecessary complexity.

How Canadian LIC Uses Corporate-Owned Life Insurance As A Strategic Tool

We see corporate-owned insurance as more than a policy. It’s a long-term asset that strengthens the corporation and protects the people who built it.

Our approach supports:

- Business continuity

- Protection of key person roles

- Smooth execution of buy-sell agreements

- Growth of cash value inside the corporation

- Extraction of tax-efficient funds through the capital dividend account

- Long-term stability for families, partners, and employees

We have seen corporate-owned plans provide business owners with the confidence to transition, assist children moving into leadership roles and make available to families tax-free distributions that would otherwise be taxed heavily.

If your business does have retained earnings, along with an involved planning process dealing with long-term succession, tax effectiveness, or executive retention, corporate-owned Life Insurance may become one of the most powerful tools you have in your financial plan.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Corporate-owned Life Insurance helps bring order to confusing times, when a company sorely requires direction. It can allow a business owner to protect their future cash flow, because it creates a line item that the corporation knows they can utilize without disrupting operations. A long-term insurance policy is that much more confidence for lenders, partners, and families associated with the business. Over time, it turns into another layer of corporate power alongside existing business investments and planning.

Yes, it does so by providing the corporation with a reliable source of funds that is not connected to unpredictable markets or short-term credit facilities. This makes sure that transitions don’t get stopped short just because things change abruptly. Corporate-owned Life Insurance “dedicates to the timing of corporate decisions but does not force transactions to be done in a hurry.” Such flexibility is often what enables a succession plan to remain consistent with the business owner’s initial intent.

When income increases, the importance of formal financial security also rises, and corporate Life Insurance provides this in abundance. It provides the corporation with stable financing precisely at times when pressure is highest, giving leadership room to think straight. Private companies are like instruments that offer protection and some long-term value. Corporate ownership of life is that mix without disrupting day-to-day capital investment.

A company-owned policy shows that the firm has thought about both the people and operations, and builds confidence in employees. It offers leadership a means of creating focused executive programs that don’t deplete active budgets. With long-term protection set up, your valuable employees rest easy knowing that the company is stable against even rough financial patches. It’s that confidence-building that builds loyalty at every step.

Company priorities change as the company scales, new partners come on, or ownership changes. A review of the insurance policy helps to ensure that coverage is being effectively maintained in support of the corporation and not being forgotten or continued based on old assumptions. Tiny tweaks can often boost long-term financial protection and tax efficiency. Regular reviews also help keep corporate-owned life in step with a company’s evolving ambitions.

It is logical to have more people insured if leadership grows or new key employees begin taking on significant responsibilities. This spreads risk and keeps the company from being too focused on a single insured person or one avenue of corporate protection. It also strengthens the company’s succession by giving people beyond the founders a stake in our long-term trajectory. It comes naturally as they scale their insurance strategy for many companies.

The power of corporate-owned life is really in how it can help facilitate decision-making prior to ever having to make a death claim. It also provides the company with a financial asset that can make planning discussions with advisers and lenders more productive. In the long run, the mere existence of this policy affects how a company thinks about growth, retention and big investments. It is a strategic weapon embedded in the very structure of corporate security.

Because it is corporate policy that shores up the financial architecture on which the company relies. It brings stability in places personal insurance can’t reach, particularly for operational or longer-term planning purposes. The company profits from protection that is embedded — not disconnected — from its balance sheet. For many owners, it is one of the only vehicles that actually does both support business continuity and long-term financial goals.”

Rapidly growing companies often have varying capital requirements, and corporate-owned Life Insurance delivers a stable anchor during those changes. It provides the corporation with an added level of protection long-term as growth accelerates. Leadership can decide that there is structured, organized support behind them. That stability enables growth, not wary growth.

Yes, because a policy owned by a corporation is a sign of disciplined planning and sound financial management. Lenders repay in some respects at least corporations which anticipate risks with regard to their status, employees , or executives. With the life assurance policy in place, it is comforting to know that the corporation can be covered in the event of unforeseen financial liabilities. This often increases your ability to borrow and enhances long-term credit relationships.

And as families establish businesses that last for generations, corporate-owned life provides a mechanism to formalize those kinds of future transitions. It ensures the company is not pushed into snap judgments when power moves to a succeeding generation. The policy encourages planning that respects the company’s legacy as well as its future journey. This is doing something about the culture while not squandering what previous generations forged.

When ownership changes or partners adjust their roles, liquidity becomes essential. Corporate-owned life offers predictable funding during these periods, keeping negotiations calm and organized. It lets the corporation move forward without disrupting operations or corporate investments. This steadiness helps maintain long-term trust among shareholders.

Absolutely. The corporation is responsible, not personal income or personal life insurance. This wall helps the business owner to keep company and personal planning separate without commingling responsibilities. The corporation is more effectively able to absorb shocks before they reach the family. Eventually, this helps take the stress out of those big planning decisions.

When business is conducted across locations or departments, risk becomes distributed as well. A corporate-owned life policy helps a corporation remain stable if one of its key people from a region experiences an unforeseen event. This makes the policy reinforce the internal consistency and maintain long-term plans. This is an absolute necessity for organizations with multi-location deployments.

Corporate restructures, expansions or changes in leadership are likely to cause the company’s protection requirement to change. These policies should be reviewed to keep the insurance structure responsive to these new realities. The company can modify policyholders, restructure ownership models or improve coverage as it changes. This way, you keep the insurance framework alive, a dynamic means of strategy as opposed to a dead paper agreement.

Professional corporations have high-income patterns and require long-term planning. The corporate-owned life provides a structured asset helping them achieve financial goals on a constant basis. It enables experts to enhance protection now and in the future, without disturbing flows of income. Eventually, the policy will be a resource that supports corporate resilience and strategy.

Yes, because it connects the executive’s long-term worth to his or her stewardship of the company. Corporate-owned life, rather than providing purely short-term incentives, can be used to create an executive benefit that grows at the pace of the corporation. This is an indication of commitment by leadership and tends to loyalty. For executives, a stability of this nature is often more significant than short-term compensation.

While external markets are unpredictable in a financial downturn, the structure of a corporate-owned policy remains constant over the long term. Having this predictable buffer while the corporation is under cash flow hardship or operational challenge is essential. This also indicates to a corporation’s employees and shareholders that our discipline is secure even when market circumstances are uncertain. For our part, the stable underpinning allows us to maintain our eyes on long-term objectives.

Accountants understand that corporate-owned Life Insurance can undergird tax-efficient planning better than many other tools they have in their toolbox. It provides an opportunity to mitigate long-term exposure to taxable income and enhances succession and continuity planning. Advisers appreciate how it works in conjunction with the existing systems, like corporate investments and retained earnings. This makes it a natural complement for long-range corporate planning.

It’s part of the bread and butter that maintains a business running through the thin times. The company receives an organized outlet to address the financial loss of a key executive or employee. This saves pressure on reserves, and it also protects working capital. This allows the company to address adversity from a position of strength rather than weakness.

Sources and Further Reading

- “Corporate-Owned Life Insurance (CL) Strategy Guide” — Canada Life PDF article on corporate Life Insurance advantages. acp.canadalife.com

- “How Corporate-Owned Life Insurance Can Accumulate Wealth” — BDO Canada Tax Q&A article on COLI. BDO Canada

- “Corporate Owned Life Insurance Considerations” — Sun Life Financial PDF detailing key COLI tax & planning issues. suncentral.sunlife.ca

- “Corporate Life Insurance – Opportunities To Die For” — Deloitte Canada perspective on COLI, CDA and succession. Deloitte

- “Corporate-Owned Life Insurance And Non-Resident Heirs” — DG & Chait LLP bulletin on COLI issues with non-resident shareholders. dgchait.com

Key Takeaways

- Corporate-owned Life Insurance in Canada strengthens long-term planning for a business owner by combining protection, liquidity, and structured tax advantages within the corporation.

- A corporate policy allows the corporation to receive a Life Insurance death benefit, creating stability for partners, families, and key employees during unexpected transitions.

- Permanent coverage, especially a participating Whole Life Insurance Policy, supports cash value accumulation, helping corporations build assets that grow alongside business goals.

- The capital dividend account becomes a valuable tool, allowing private corporations to move insurance proceeds to shareholders as tax-free distributions when a death claim occurs.

- Corporate-owned life helps manage share purchases, key person risks, and succession planning—areas where personal insurance cannot protect corporate investments effectively.

- The structure minimizes long-term tax liability by pairing CDA credits with a declining adjusted cost basis, giving corporations an efficient path for future planning.

- Business owners benefit from clearer decision-making, stronger executive retention strategies, and more predictable financial protection across changing corporate needs.

- Working with advisors ensures that corporate-owned policies remain aligned with the Income Tax Act, ownership structure, and future growth plans of the corporation.

Feedback Questionnaire:

We’d love to understand your experience so we can create guidance that actually helps business owners like you. Please take a moment to share what you feel — your insights shape our next steps.

IN THIS ARTICLE

- Corporate-Owned Life Insurance In Canada: Benefits And Tax Guide For Business Owners

- Corporate-Owned Life Insurance In Canada: Benefits Tax Guide For The Business Owner

- What Is Corporate-Owned Life Insurance In Canada?

- How Corporate-Owned Life Insurance Differs From Personal Coverage

- Capital Dividend Account And Corporate-Owned Life Insurance

- Understanding Adjusted Cost Basis And Net Proceeds

- Capital Dividend Planning For Private Corporations And Holding Companies

- Why Permanent Life Insurance And Participating Whole Life Work Best For Corporate-Owned Life Insurance

- Cash Value, Cash Surrender Value, And Corporate Liquidity

- Corporate-Owned Life Insurance For Key Person Insurance And Executive Benefits

- Corporate-Owned Life Insurance And Buy-Sell Agreements

- Comparing Term Insurance And Whole Life Insurance Inside The Corporation

- Understanding COLI Premiums And Long-Term Net Cost

- Planning With Holding Companies And Multi-Entity Structures

- Key Considerations, CRA Rules, And A Strong Advisory Team

- How Canadian LIC Uses Corporate-Owned Life Insurance As A Strategic Tool

Sign-in to CanadianLIC

Verify OTP