- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Group To Individual Life Insurance Conversion In Canada: The 2026 Ultimate Guide

By Harpreet Puri

CEO & Founder

- 11 min read

- January 22nd, 2026

SUMMARY

Know how Canadians can convert a Group Life Insurance Policy into an Individual Life Insurance Plan to maintain protection after leaving a job. It covers eligibility, coverage amount, premium calculation, and how medical exams are waived during Group Life Insurance conversion. Readers learn about benefits, costs, and options from top Life Insurance companies in Canada using updated Term Life Insurance rates by age chart insights.

Introduction

When you lose your job, retire or start your own business, one of the first money-making plans many people gravitate toward is this: What’s going to happen to my insurance? You’ve relied for years on a Group Life Insurance Policy and the impenetrable feeling of safety it provides — but when that coverage disappears with your employer, so can your security blanket.

We see hundreds of people facing this very situation. They don’t know whether they are still covered under their group policy or if they have to begin anew. The good news? You don’t have to. In Canada, the Group Life Insurance conversion feature is the process of converting Group Life Insurance into an Individual Life Insurance Policy without new medical exams, extended waiting periods or rigorous underwriting.

This article is your comprehensive guide to everything you need to know about Group to Individual Life Insurance conversion in 2026—what it means, how it works, who it’s for, what the cost looks like and how to easily make a move into long-term protection without missing out on even a single day of coverage.

Understanding The Concept Of Converting Group Life Insurance

Canadian insurance companies include a Group Life Insurance contract as part of their benefits. It’s an amazing benefit — with no personal medical underwriting or high premiums. But here’s the rub: that coverage is dependent on your employment.

When you retire, change jobs or your group plan lapses, that sense of security goes away — unless you utilize your conversion privileges.

Converting Group Life Insurance is converting a Group Policy to an Individual One within a certain window (usually at least 31 days for life coverage, and in some plans up to 60 days for health and dental conversion, depending on the insurer), usually with the same insurer.

Here’s the best part:

- No medical exam or new underwriting is required.

- For life insurance, your new policy cannot be declined based on health, and many health and dental group conversion plans are designed to accept pre-existing conditions, subject to each insurer’s rules.

- In some health and dental conversion plans, waiting periods may be reduced or waived if you had prior group coverage, depending on the insurer and plan design.

- You maintain continued coverage during life transitions.

It’s a smart move that ensures your financial protection doesn’t end just because your job does.

Why Group Life Conversion Matters More In 2026

Data from the Canadian Life and Health Insurance Association (CLHIA) indicate that over 24 million Canadians have Group Insurance or benefits through their employer. But as work patterns have changed — more people freelancing, retiring earlier or working part-time — so has the number of people who head out on their own each year expanded rapidly.

For many people, that moment of change is financially harrowing. But changing a Group Life or eligible Group Health and Dental Insurance Policy to an Individual Plan allows you to keep the benefits that made those policies so valuable in the first place, such as Life Insurance benefits, accidental death coverage, and, where available, extended health and vision services.

We help clients every week who are:

- Retiring from full-time employment.

- Transitioning to part-time or contract work.

- Moving into self-employment.

- Facing layoffs or career breaks.

A simple Group Life Insurance Policy conversion protects you and your family’s long-term financial goals even when your employment changes.

How Group Insurance Conversion Works In Canada

The conversion process is straightforward but time-sensitive. Here’s what it typically involves:

1. Eligibility Requirements

You must be part of an existing Group Life Insurance Plan at the time of separation from your employer. Once you leave, most insurance providers allow a conversion window of at least 31 days (with some plans offering up to 60 days depending on the benefits being converted). Miss that, and your group conversion rights may lapse permanently.

2. Coverage Amount

You can usually convert part or all of your Group Life Insurance Coverage to an individual plan. Some insurers cap this at a percentage of your original coverage amount, but you’ll still retain the flexibility to choose your desired Individual Coverage level.

3. Premium Calculation

Your new premium is based on your age at conversion and your selected coverage amount. Factors like your annual salary, employment status, and financial goals may also influence your premium type—especially if you opt for a Term Life Insurance Plan or Permanent Life Insurance Policy.

4. No Medical Underwriting

This is the biggest advantage. You don’t have to go through medical underwriting or submit a medical questionnaire. Even if you have pre-existing conditions or recent medical treatments, your new individual life policy cannot be denied. Health/dental conversion options depend on the carrier and plan.

5. Application Submission

You’ll need to notify your insurance company within the conversion window and complete a simple application form with personal details and prior Group Policy information.

6. Issuance Of Individual Policy

Once approved, your Individual Life Insurance Policy activates immediately—giving you continued coverage with no interruption.

Example: How Conversion Premiums Are Calculated

Let’s consider a real case we handled recently.

A client, age 55, living in Ontario, wanted to convert Group Life Insurance worth $50,000 into an individual term life policy offered under the insurer’s standard conversion options until age 65.

Her calculation looked like this:

- Rate per $1,000 coverage: $12.50

- Annual premium: $12.50 × 50 = $625

- Provincial premium tax (2%): $625 ÷ (1 – 0.02) = $638.78

- Monthly premium: $638.78 ÷ 12 = $53.23/month

That’s less than the average cell phone bill—yet it protects her family with Guaranteed Life Insurance benefits for 10 years, regardless of future health issues.

Who Should Consider Converting Group Benefits

The Group to Individual conversion option is ideal for Canadians who:

- Are you retiring or losing employer coverage?

- Are you becoming self-employed or contract-based?

- Have pre-existing conditions that might limit new insurance approval.

- Want to maintain coverage without a medical exam.

- Need comprehensive coverage to replace their group benefits package.

We often help retirees, healthcare workers, and educators who’ve had Group Policies for decades. They worry that without conversion, they’ll face higher premiums or be ineligible due to age or pre-existing health conditions.

Conversion eliminates those worries—it locks in protection seamlessly.

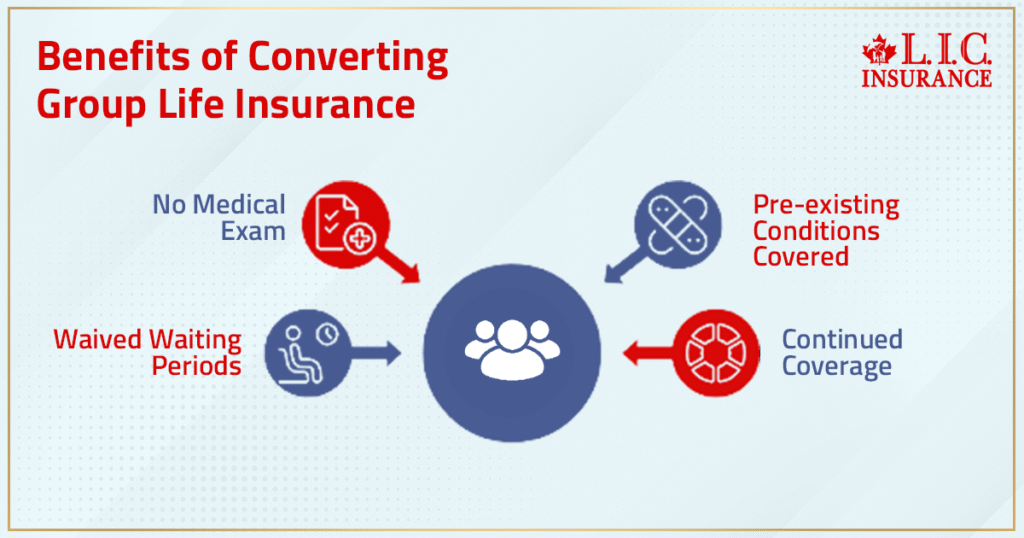

Benefits Of Converting Group Coverage To An Individual Plan

When you convert Group Life Insurance to an Individual Plan, here’s what you gain:

1. Portability

Your coverage stays with you—not your employer. No matter where life takes you, your Individual Plan ensures continued protection.

2. Customization

Unlike standard Group Life Insurance Policies, Individual Policies offer more customization options. You can choose Term, Whole, or Universal Life, adjust coverage amounts, or add riders like critical illness or disability insurance.

3. Reduced Or Waived Waiting Periods

Many health and dental group conversion plans may reduce or waive waiting periods, depending on the insurer.

4. Inclusion Of Pre-Existing Conditions

Life conversion always accepts you regardless of health. Health/dental acceptance depends on the insurer’s conversion rules.

5. Continued Financial Security

Your Individual Policy ensures continued coverage and acts as a safety net during employment transitions. It keeps your family financially protected no matter what happens at work.

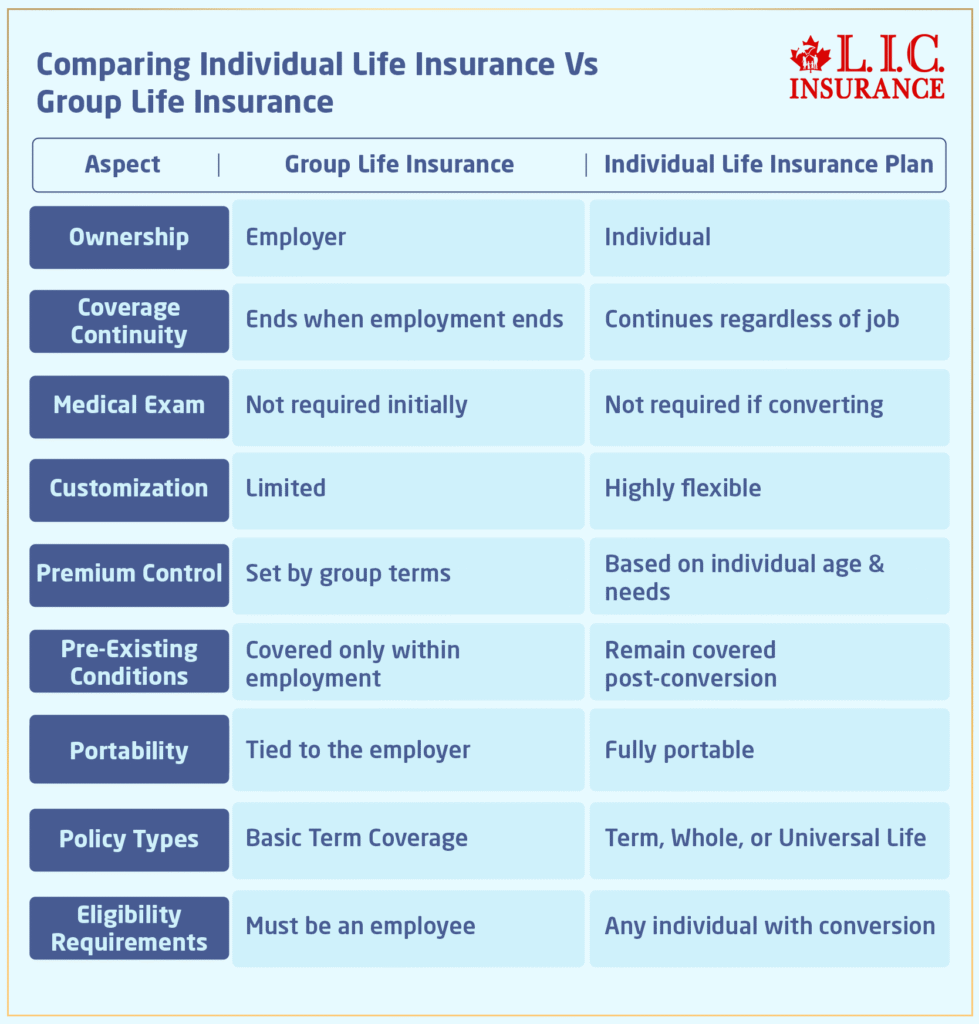

Comparing Individual Life Insurance Vs Group Life Insurance

When comparing Individual Life Insurance vs Group Life Insurance, it’s clear that conversion gives Canadians greater control and flexibility over their Insurance Coverage—and peace of mind that doesn’t depend on their employer.

The Difference Between Porting And Converting Group Benefits

While both allow continued coverage, porting and conversion differ slightly:

| Aspect | Porting Group Benefits | Converting Group Benefits |

|---|---|---|

| Coverage Continuity | Maintains the same plan temporarily | Switches to a new Individual Plan |

| Eligibility Requirements | Usually tied to specific life events | Applies when leaving a job or retiring |

| Employer Role | Involves coordination | Independent of employer |

| Underwriting | May require medical checks | Typically, no medical exam |

| Flexibility | Limited | More customizable |

| Premiums | May increase or decrease | Based on age & coverage amount |

Conversion offers longer-term stability and independence compared to porting, which often expires after a short term or policy limit.

What Benefits Do Converted Plans Include?

Converted Individual Insurance Plans often provide:

When your employer plan includes health/dental conversion, you may receive:

- Vision care (glasses, exams, contacts)

- Hospital accommodation and private nursing care

- Paramedical services (chiropractic, massage, physiotherapy)

- Accidental dental and accidental death coverage

- Medical services and supplies

- Survivor benefit for dependents.

- Final expense benefit for estate costs

If you add Dental Coverage, benefits may include:

- Diagnostic and preventive care (x-rays, fluoride treatments)

- Restorative care (fillings, crowns, root planing)

- Minor prosthodontic repairs

- Routine extractions

Exact benefits depend entirely on the carrier and the group contract’s conversion options.

Depending on your plan, 50–80% of your eligible expenses are typically covered under your Group Insurance Conversion Plan.

Factors To Consider Before Converting Group Benefits

Before deciding, review these factors carefully:

- Health Needs – Evaluate your ongoing health requirements and how Individual Coverage supports them.

- Finances – Compare the annual cost, deductibles, and out-of-pocket expenses between staying uninsured and converting.

- Policy Options – Consider whether you prefer a Term, Whole, or Universal Life Plan.

- Future Employment – If joining a new employer, check their Group Plans before deciding.

- Timing – Don’t miss the 31–60 day conversion window after leaving your job.

When in doubt, our licensed insurance brokers can help you analyze conversion options from top Life Insurance companies in Canada and find a plan that best fits your lifestyle and budget.

How Life Insurance Conversion Supports Long-Term Financial Goals

Moving from Group Life Insurance to an Individual Policy is not just about protection — it’s also about ensuring control over your future.

An Individual Policy provides you with: Known Term Life Insurance rates by age chart references, Long-term affordability, and guaranteed access to coverage

Many Canadians use this opportunity to upgrade from basic coverage to comprehensive coverage, adding Critical Illness or Disability Riders for added security.

Your insurance conversion is an important component of your overall plan to insulate and protect the value of yourself, your health and your family—without a new exam or wait period.

When You Should Act

Timing is everything. Many Canadians don’t know their Group Life Insurance will end after they leave work, and they may find themselves suddenly without coverage.

You have the above wait period (usually 31-60 days) to apply for a conversion. Miss this opportunity and new coverage requires medical underwriting (which means you can be denied), higher premiums or both.

So one of the reasons is to ensure everyone reviews their group benefits and conversion options if they are retiring or resigning. It’s not just good planning — it’s the responsible financial thing to do.

Essential Insights From Canadian LIC’s Life Insurance Advisors

- Converting Group Life Insurance allows employees to retain continued coverage beyond employment.

- No medical exam or new underwriting is required.

- Pre-existing conditions remain covered under life conversion, while health/dental conversion acceptance depends on the insurer.

- Conversion is guaranteed for Life Insurance and available for health, dental and disability only when offered by the original Group Plan.

- Premiums depend on age, coverage amount, and individual plan type.

The Canadian LIC Advantage

We help make the Group Life Insurance conversion process less confusing. Our advisors accompany you step-by-step, from comparing plans to confirming that the coverage is a good fit for your needs and connecting you with Canada’s leading insurance companies.

We know that insurance is more than a policy—it’s a promise. And we will make sure that promise persists when this group policy ends.

If your job is in transition or retirement looms, consider converting now. Because financial security should never depend on a paycheque — it should depend on a plan that is there for you, if your situation changes.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes, most insurers allow a Group Insurance conversion even if your insurance provider changes. What matters is your eligibility window after employment ends. We help confirm which Group Life Insurance Plan terms still apply so your Individual Coverage stays uninterrupted.

When you convert Group Life Insurance, you can add extra protection under your Individual Life Insurance Policy. Riders such as Critical Illness or Disability can be layered in for comprehensive coverage. Our advisors tailor these Individual Plans to match personal financial goals and risk tolerance.

If the conversion window expires, new medical underwriting applies, and higher premiums may follow. You’d need a fresh medical exam and could lose coverage for pre-existing conditions. That’s why we track waiting periods closely to help clients maintain coverage without disruption.

Absolutely. Once issued, your Individual Life Insurance Plan is portable across Canada. Even if you move provinces or shift to self-employment, the group conversion you completed remains valid. Our team ensures provincial tax rates and coverage rules stay compliant with each insurance company.

Your insurance provider checks employment records, policy number, and coverage amount under the Group Policy. They confirm you fall within eligibility and conversion options as outlined by the Group Plan. We coordinate directly with insurers, so you can convert Group Life Insurance smoothly.

No, having an existing Individual Life Insurance Policy from Group Life Insurance conversion doesn’t restrict new applications. In fact, maintaining continuous Insurance Coverage may improve your risk profile. We use this history to negotiate better rates with top Life Insurance companies in Canada.

Yes, many insurance providers allow increases or riders after the conversion process. Your coverage amount can grow as your financial goals change. We review each Individual Plan periodically to ensure the protection still fits your income, debts, and family responsibilities.

Dependents can often retain their portion of Group Life Insurance coverage through conversion. Each dependent can apply for an Individual Policy without a medical exam. We help families manage these transfers so everyone’s continued coverage remains intact during job or retirement transitions.

Some Group Insurance Coverage includes health and dental benefits that convert with Life Insurance. When you convert Group Life Insurance, you may extend select Health Insurance and vision benefits under the new Individual Plan. Our advisors help you compare options for maximum continued coverage.

Typically, insurance carriers issue the new Individual Policy within days of receiving the application and premium. Because there’s no medical examination, the approval process is fast. We handle the paperwork so your Life Insurance conversion activates with no gap in coverage.

Key Takeaways

- Converting Group Life Insurance to an Individual Life Insurance Plan helps maintain financial protection after retirement, job change, or self-employment.

- The Group Life Insurance conversion process in Canada doesn’t require a medical exam, ensuring a smooth transition and continued coverage.

- Premiums for converted individual policies depend on age, coverage amount, and selected plan type, offering flexibility through top Life Insurance companies in Canada.

- Conversion options typically include coverage for pre-existing conditions and waive waiting periods for health or dental benefits.

- Employees can secure long-term individual coverage by applying within 31–60 days after their group coverage ends.

- A converted Individual Life Insurance Policy offers greater customization, portability, and independence than employer-based Group Life Insurance Policies.

- Working with an experienced insurance provider or broker like Canadian LIC ensures accurate premium calculations and seamless policy conversion.

Sources and Further Reading

- Canadian Life and Health Insurance Association (CLHIA) – Industry reports and guides on life and health insurance coverage trends across Canada.

https://www.clhia.ca - Office of the Superintendent of Financial Institutions (OSFI) – Regulatory insights and guidelines for Canadian insurance companies and policyholder protection.

https://www.osfi-bsif.gc.ca - Financial Consumer Agency of Canada (FCAC) – Detailed consumer information about group and Individual Life Insurance, conversion options, and coverage rights.

https://www.canada.ca/en/financial-consumer-agency.html - Statistics Canada (StatCan) – Data and reports on employment trends, benefits participation, and national insurance coverage demographics.

https://www.statcan.gc.ca - Autorité des marchés financiers (AMF) – Provincial regulatory body in Quebec overseeing financial products, including life and health insurance conversion policies.

https://lautorite.qc.ca - Insurance Bureau of Canada (IBC) – Educational materials about group benefits, coverage transitions, and consumer rights in Life Insurance.

https://www.ibc.ca - Manulife Canada – Life Insurance Conversion Options – Corporate guide explaining how employees can convert Group Life Insurance coverage into individual protection.

https://www.manulife.ca - Sun Life Canada – Group Benefits & Conversion Options – Official information outlining conversion timelines, eligibility, and premium structures for individual coverage.

https://www.sunlife.ca - Canada Life – Group Life to Individual Life Conversion Guide – Details on maintaining coverage continuity and available conversion benefits after employment changes.

https://www.canadalife.com - Industrial Alliance (iA Financial Group) – Advisor-focused resources discussing conversion options from group to individual life and health insurance plans.

https://ia.ca

Feedback Questionnaire:

We’d love to hear from you!

Your feedback helps Canadian LIC understand what Canadians are really experiencing when converting their Group Life Insurance Policy to an Individual Life Insurance Plan. Please share your thoughts below — it only takes 2 minutes.

📩 Submit your response and stay informed about Life Insurance solutions that truly fit your goals.

IN THIS ARTICLE

- Group To Individual Life Insurance Conversion In Canada: The 2026 Ultimate Guide

- Understanding The Concept Of Converting Group Life Insurance

- Why Group Life Conversion Matters More In 2026

- How Group Insurance Conversion Works In Canada

- Example: How Conversion Premiums Are Calculated

- Who Should Consider Converting Group Benefits

- Benefits Of Converting Group Coverage To An Individual Plan

- Comparing Individual Life Insurance Vs Group Life Insurance

- The Difference Between Porting And Converting Group Benefits

- What Benefits Do Converted Plans Include?

- Factors To Consider Before Converting Group Benefits

- How Life Insurance Conversion Supports Long-Term Financial Goals

- When You Should Act

- Essential Insights From Canadian LIC’s Life Insurance Advisors

- The Canadian LIC Advantage

Sign-in to CanadianLIC

Verify OTP