- Can I Cancel My Critical Illness Insurance

- Knowing Your Policy: The First Step To Making Informed Decisions

- Can You Cancel Anytime? Unveiling The Flexibility Of Critical Illness Insurance

- The Process: How To Cancel Your Critical Illness Insurance

- Reassessing Your Needs: When Is It Right To Cancel?

- Conclusion: Make Your Life Secure With The Right Protection

When life changes, insurance needs change too. Many people often wonder, “Can you cancel critical illness insurance if it no longer fits their situation? If you’re asking yourself, “Can I cancel my critical illness insurance?”, you’re not alone — and this guide will walk you through it. Imagine you’ve just started a new working chapter overseas, leaving the comfort of your familiar surroundings. During this significant life change, you discover that the Critical Illness Insurance you bought at home is no longer suited for you. Or, after you’ve reassessed your financial objectives, you realize that your current Critical Illness Insurance Policy needs some changes. These are all common situations faced by numerous others, and they all lead to one question: “Can I cancel Critical Illness Insurance?” The process of cancelling your policy can be complex. But with knowledge of the right steps and what to expect, the process can become super simple for you. If you want to cancel your Critical Health Insurance Plans, this blog will make it easier for you by using real-life examples and giving you help to ensure you make decisions that you won’t regret.

Knowing Your Policy: The First Step to Making Informed Decisions

Before determining the process involved in cancelling, you need to know what your Critical Illness Insurance Coverage really is. When 40-year-old graphic designer John decided to evaluate his financial commitments, he was overwhelmed. He found that the terms of his policy differed from what he had expected them to be, specifically regarding coverage and cancellation conditions. Critical Illness Insurance Quotes often highlight the best aspects of a policy but might not always delve into cancellation policies clearly. Start by reviewing your policy documents or contacting your insurance provider to get clear, concise information. This step is crucial in avoiding surprises like cancellation fees or conditions.

Can You Cancel Anytime? Unveiling the Flexibility of Critical Illness Insurance

Most Critical Health Insurance policies do allow cancellations, but exactly what will happen may significantly vary in terms and conditions. For instance, a teacher by the name of Emily chose to cancel her cover after she improved significantly in health status. She later realized that although she could cancel at any time, the return of premium had some prerequisites that she had to be informed about while taking the policy. Notably, one should know the timing and the financial implications of cancelling at that time. Some policies will have charges whenever you cancel, while premiums may not be refundable if you have paid up to a specific period. These will affect your financial planning, so you should have them in mind.

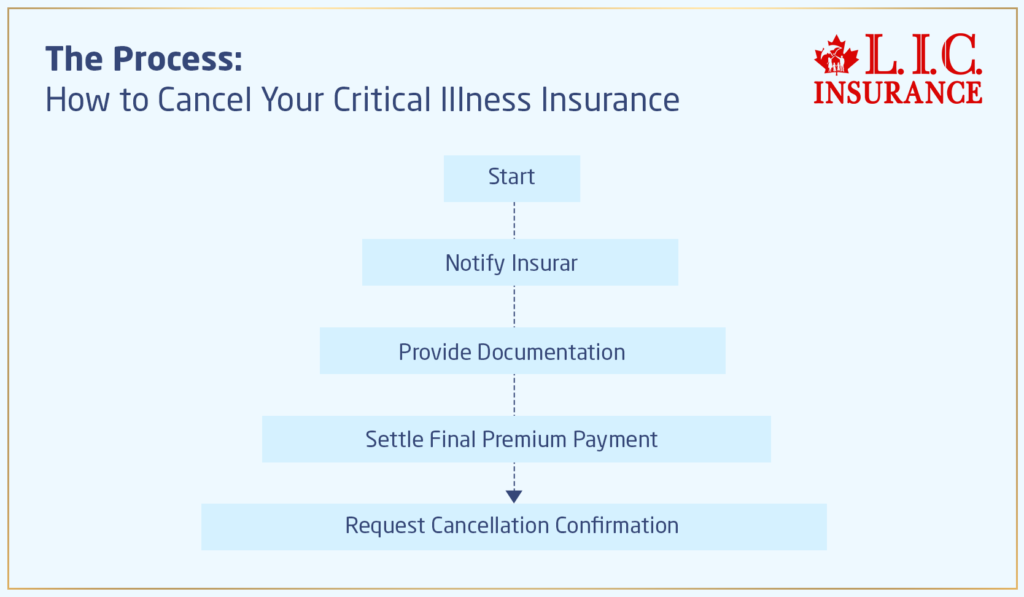

The Process: How to Cancel Your Critical Illness Insurance

How Timing Affects Refunds When Cancelling Critical Illness Insurance

One important but often overlooked aspect when asking “Can I cancel my critical illness insurance?” is how the timing of your cancellation affects any potential refund or financial recovery. While most articles broadly state that policies can be cancelled, few address how insurers handle refunds based on the cancellation date — a factor that could impact your decision significantly.

If you’re wondering, “Can you cancel critical illness insurance,” and still recover part of the money you’ve paid, the answer often depends on when you act. Many insurers offer a “free-look period” — typically 10 to 30 days after the policy starts — during which cancelling results in a full refund with no questions asked. However, if you cancel after this window, refunds usually become prorated. This means you might only receive a portion of prepaid premiums, and administrative fees could further reduce the amount you get back.

Additionally, if you paid your premiums annually instead of monthly, you might be eligible for a larger prorated refund compared to a monthly payer. Therefore, timing your decision carefully — even by just a few weeks — can make a meaningful financial difference. Always check your policy documents or speak to a licensed insurance advisor before proceeding to ensure you maximize any potential refund benefits.

Cancelling a policy for Critical Illness Insurance should be a crucial decision that should be well arranged with proper planning and a lot of attention to the details. Keep reading further to understand how to easily cancel your policy in an efficient and effective manner so that you understand each step properly.

Step 1: Information

First, you should formally notify your insurer of your intention to cancel the policy. Generally, you notify your insurer through a written notice. This could be a letter sent through post or a document emailed to the customer service department. Some of them have the critical health plan, which has an online cancellation form. This can be a convenient and more rapid method. Consider the story of Alex, a software developer who moved to a country with a universal healthcare system. Alex needed to cancel his policy but delayed sending the notification. This oversight led to unnecessary charges for a policy he no longer needed. Remember, the date you notify your insurer will often be considered the start of the cancellation process, so timely notification is crucial.

Step 2: Documentation

You will likely have to provide certain documents to your insurer to finalize the cancellation after you notify them. Very often, insurers require a signed cancellation form with a written request. Make sure the document includes your policy number, your date of cancellation, and your contact information. Let me give you an example. Maria was a retired nurse, so all this documentation seemed overwhelming to her. So, she sent an email without a formal signature, which got rejected for the first time. So, to keep you out of such pitfalls, always double-check with your insurer about the exact requirements. Getting it right the first time can spare you from the headache of re-submissions and potential delays.

Step 3: Final Premium Payment

Your cancellation might also involve settling any outstanding Critical Illness Insurance premiums. These circumstances may follow your billing cycle and the terms of your policy. If your premium is paid on a monthly basis, then ensure all the paid premiums are up-to-date. In case there are some outstanding amounts, please clear them before you put in your request for cancellation, as this could reflect on your cancellation request.

Consider Rahul’s experience: he assumed his final premium would be prorated and delayed payment, which led to a temporary freeze on his cancellation process. To prevent this, clarify with your insurer whether you need to settle the full month’s premium or only the portion up to your cancellation date.

Step 4: Confirmation

Finally, you should always request confirmation of your successful cancellation of the policy. This should be in writing, more likely with a formal letter or even an email. This step is required for a number of reasons. First, in the event of a claim of non-cancellation, this is documentary evidence of completion. Second, you can no longer be liable for the payment of future premiums. Consider Linda, who believed she had cancelled her policy but never received confirmation. Months later, she was shocked to see a bank statement indicating a deduction of the premium amount. It seemed her cancellation was never processed. Get your cancelling confirmation right away and keep it somewhere safe to avoid problems like these.

Throughout the cancellation process, maintain open communication with your insurer. Ask questions if any part of the process or any of the quotes for Critical Illness Insurance is unclear. Many find this conversation scary, but remember, as a policyholder, you have the right to be in control of your Critical Illness Insurance at your discretion.

Reassessing Your Needs: When Is It Right to Cancel?

Deciding to cancel your Critical Illness Insurance is a major decision that should align closely with your life’s evolving circumstances. Whether it’s a change in your health, finances, or family responsibilities, each factor must be carefully weighed to ensure you’re making the best choice for your future. Let’s explore these considerations through a detailed breakdown featuring real-life scenarios that might resonate with your own experiences.

Significant Changes in Health

Scenario: Maria was diagnosed with a chronic illness five years ago and purchased a critical illness policy soon after. Recently, her condition has significantly improved due to advanced treatments and lifestyle changes. She now finds herself reconsidering the necessity of her critical illness cover.

What to Consider: If your health has improved dramatically or if medical advancements have reduced your potential risk, it might be a suitable time to review your policy’s value. However, it’s crucial to consider the possibility of recurring or new serious illnesses and discuss these changes with a healthcare professional before making a decision.

Financial Shifts Impacting Your Budget

Scenario: After Sam lost his job, the monthly premiums for his Critical Illness Insurance began taking a toll on his dwindling savings. He started to question if the premiums were justifiable given his tight budget.

What to Consider: Review your financial situation comprehensively. If premium payments are becoming a burden, consider cancelling or looking for a more affordable option. On the other hand, remember the financial impact a sudden illness could have without the safety net of insurance. It might also be a good moment to consult with a financial advisor to explore cost-effective strategies or alternative coverage options that won’t compromise your financial security.

Life Stage and Family Responsibilities

Scenario: When Chloe and her partner first got their Critical Illness Insurance, they were just starting a family. A decade later, with their children heading off to college soon and their savings solidly built up, they wonder if their policy is still necessary at the same level of coverage.

What to Consider: Your life stage plays a significant role in insurance needs. As dependents grow up and become financially independent, or as you approach retirement, your insurance requirements may diminish. Evaluate your current and future responsibilities—might there be less financial strain if a health issue arises now compared to earlier in your life? Engage in a family discussion about these topics to make a well-rounded decision.

Consulting Professionals for Tailored Advice

Scenario: Before making any final decisions, Jack consulted with a licensed insurance advisor who specialized in insurance. Together, they reviewed his current policy, discussed his financial goals, and evaluated the risks and benefits of cancelling or adjusting his coverage.

What to Consider: Insurance isn’t one-size-fits-all, and the decision to cancel should come after thorough consultation with experts. A financial advisor or insurance advisor can offer insights specific to your situation, helping to illuminate aspects you might not have considered. They can assist in reviewing the terms of your policy, including any potential return of premium or the implications of cancellation.

When you decide whether to keep, change, or cancel your Critical Illness Insurance, think about what each step will mean. Reading through these real-life examples will help you figure out if your own case has any of the things that would cause your insurance to change. Working with professionals and getting reevaluated regularly will make sure that your insurance coverage fits your needs and follows the current and most probable path that lies in your life right now. Being sure of your choice comes from knowing you’ve thought about all the details and talked to the right people for advice.

Conclusion: Make Your Life Secure with the Right Protection

While the idea of cancelling your Critical Illness Insurance might seem like a relief in certain situations, ensuring that you are adequately covered should remain a priority. If your circumstances have changed or you’re seeking a policy that better suits your current needs, consider exploring other Critical Illness Insurance options.

Canadian LIC is the epitome of those seeking reliable and wide insurance solutions. With a variety of Critical Illness Insurance Quotes and plans to fit different needs, Canadian LIC can help you find your way through the complicated world of insurance. Don’t let doubt shape your future; contact Canadian LIC right now at +1 416 543 9000 to get a plan that protects your health and the health of your family in the best way possible.

The decision to take the initiative to reconsider or even cancel your Critical Illness Insurance can be a big decision, but with the right information and support, it can be one that will lead you toward a more secure financial future. Whether it’s the need for readjustment of your cover or cancellation, make sure that, as the case may be, your insurance is in line with your life situation so that one less thing can be on your mind regarding life’s inevitabilities.

Find Out: The differences between Life Insurance and Critical Illness Insurance

Find Out: Critical Illness Insurance Benefits

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQs: Understanding the Nuances of Canceling Your Critical Illness Insurance

Getting Critical Illness Insurance Quotes is quite easy. You can visit the websites of insurance providers or use comparison tools online. Take the case of Ravi. He wanted to balance the cost with the coverage and he did just that. He gathered quotes using an online comparative tool and conversed with many insurers over the telephone directly to know the subtle features of each of the policies. Remember, you should compare not only the cost but also the Critical Illness Insurance benefit and exclusions for each plan.

Surely, you can. Just like what happened with Susan. She decided to cancel her old policy after reviewing the same and finding the policy totally deficient. She described all that. Then, she compared other Critical Health Insurance policies and chose one that provided better coverage and matched her new health needs and lifestyle. Remember to have your new policy in place before cancelling the old one to avoid any gaps in coverage.

If you are indeed in a financial crunch like Tom, revisit the policy again and see if there are provisions that give adjustments in premium rates or breaks in payment. Tom got in touch with his insurance provider, and after seeing his financials, they gave him a temporary premium reduction. Remember to always be open with your insurance company. They may have solutions to keep you insured at some level without having to cancel your policy.

This depends on your specific policy. Angela learned that the hard way when she cancelled her policy and faced a cancellation fee she wasn’t expecting. Always make sure that you have read the fine print in your policy document so you understand under what circumstances your coverage might be associated with cancelling your coverage. When in doubt, call your insurer’s customer service to clarify.

It’s considered best practice to review your Critical Illness Insurance Policy at least once a year or when there have been major life changes. Mark always reviewed his policy once a year on his birthday, and this was helpful in tweaking his coverage as his family grew and his health changed. Regular reviews ensure your policy continues to meet your needs and provide you with an opportunity to make needed adjustments.

Reinstating a cancelled policy can be complicated. For instance, suppose Lisa decided to cancel her policy; after a while, she was again scared by a health issue, after which she understood that it is very important to have coverage. Now, she will have to apply for new insurance. Meanwhile, the medical test and other procedures have increased the premium cost of her policy because her age and disease have further deteriorated. If you’re unsure about cancelling, consider other options, like adjusting your coverage instead of fully cancelling it.

To ensure that your Critical Illness Insurance Plans cover all the needs you could have in the future:

Assess your health risks and financial situation in the round.

Speak with an insurance expert who can help draft a policy suitable for your conditions.

Take Jeremy’s story—he worked with an insurance broker to tailor a policy focused on diseases in his family history.

Yes, upgrading your plan is a great option if your needs have grown. Consider Priya’s experience—after her father was diagnosed with a hereditary condition, she realized her current policy wouldn’t cover all potential medical expenses. She contacted her insurer to discuss upgrading her policy to include more comprehensive coverage. Always assess your Critical Health Insurance Plans periodically, and don’t hesitate to enhance your coverage if your circumstances or health risks change.

It’s a crucial difference. Critical Illness Coverage pays a lump sum when you’re diagnosed with a covered condition—meaning that you can use that money for other needs than medical bills. Health Insurance typically pays for the costs of a sickness or injury as they occur. James learned this first-hand when he had surgery and received a payout from his Critical Illness Insurance to pay bills around the house during his recovery—a benefit his health insurance did not provide.

Most Critical Illness Insurance policies include a waiting period before the coverage starts. Maria had to wait 90 days before her policy was in effect. During this time, no benefits would be paid out even if a critical illness was diagnosed. This is really good to know so that you can plan your coverage accordingly. This can be found in your policy or information given to you through your provider.

Yes, definitely, family history can impact the rate at which one offers a critical illness plan. When Alex applied for insurance, he disclosed that his family had a history of heart disease. This influenced his premiums, but it also ensured he got the coverage adequately formed according to his risks. Always keep your medical history transparent so that you get coverage that covers your needs.

The first step is to understand why your claim was denied in the first place. Sophia’s claim of Sophia was denied at first because the insurer thought the diagnosis was of a different condition. She read the terms and conditions of the policy and collected all necessary medical documents to prove her point to the insurer. If your claim is denied, ask the insurer to give reasons, and in case you feel the decision is incorrect, you can appeal the decision by having adequate proof or by getting legal advice.

Look out for the claim settlement ratio from your insurer. Since claims are an important part of the Critical Illness Insurance Policy, it is important to buy a plan from an insurance company with a good claim settlement record. Daniel compared several providers by reading online reviews and asking for recommendations from friends who had filed claims before. He chose a provider known for fair handling of claims and good customer support. Make an informed decision by researching different Critical Health Insurance Plans.

One can get better quotes on Critical Illness Insurance policies by comparing different plans over the internet. Michael learned this when he was searching for a budget-friendly option. He used an online comparison tool that allowed him to see various plans side-by-side, focusing on the coverage and the premiums. Do not just compare the price, but compare what is covered. Sometimes, it is worth paying a little more for a plan that offers more coverage.

Exclusions are key. For example, Anita learned that her Critical Illness Insurance would not cover pre-existing conditions, as she had been admitted for fever before the policy was purchased. Most plans exclude sign and symptom cancers or require the illness to reach a specific severity level before paying out. Make sure you get all the details on any exclusions that may apply to you.

Generally, the settlement of a claim commences at the time of submission of a valid claim, along with all relevant medical evidence to establish the diagnosis. Take Carlos, for example, who was diagnosed with a critical illness that his policy had covered. At the time of filing his claim, following the assessment and validation of his medical documents, the insurer disbursed the entire sum assured to him in one payment. This amount also assists him in managing his treatment costs without waiting for the treatment to be over to obtain a reimbursement of his out-of-pocket costs.

Yes. Most critical illness companies will allow you to add coverage for your kids. Lisa did add her children to her policy for a very minimal additional premium. For her, this proved to be very reassuring since she knew that if anything happened to one of her children, the policy would come to the rescue with some assistance to help take care of the child and any related expenses. Check with your provider to see exactly what options for family coverage are available.

Well, that depends entirely on you, your lifestyle, and your financial background. The best amount of Raj’s insurance coverage that he decided to take was one that could cover his total liabilities, ongoing monthly household expenses, and any estimated emergency medical costs. Think of how much money you would need to keep your life running smoothly and meet your liabilities in case you were not able to earn money for a long time. A financial advisor can help you come up with a close estimation.

As a rule of thumb, in most places, the lump-sum payouts from Critical Illness Insurance policies are paid out tax-free, but this may still vary from place to place based on local laws. Natalie did get a payout, but it was best to walk in and discuss the matter with her tax advisor. Go through the tax rules in the area of your residence, or consult a tax professional to learn about your obligations or benefits related to you.

People need to think carefully about Critical Illness Insurance challenges, like where to find cheap quotes and how taxes might affect payouts. We have provided these FAQS on Critical Illness Insurance as a testimony of what an average man or woman may have to face in life and how to prepare oneself just in case you find yourself in this decision-making position regarding insurance for your family or personally. The right Critical Health Insurance Plan should take that worry away, reassuring you that financially, you are not at the mercy of unpredictable health reactions.

Sources and Further Reading

Consumer Reports – Insurance Section: This resource provides unbiased reviews and comparisons of various insurance plans, including Critical Illness Coverage. It can help you understand the features and limitations of different policies.

National Association of Insurance Commissioners (NAIC): NAIC offers comprehensive guidelines and educational materials to help consumers understand insurance policies, including the specifics of Critical Illness Insurance.

The Balance – Critical Illness Insurance Guide: An extensive guide that covers the basics of Critical Illness Insurance, what it covers, what it doesn’t, and how to choose the right policy for your needs.

The Balance – Critical Illness Insurance

Investopedia – Insurance Section: Provides detailed articles on Critical Illness Insurance, including how to compare quotes, understand policy features, and the financial implications of cancelling a policy.

HealthInsurance.org: Offers insights into how health insurance complements Critical Illness Coverage, helping you make informed decisions about both types of insurance.

These sources can provide additional depth and context to the topics discussed in the blog, enhancing your understanding of Critical Health Insurance Plans and related decisions.

Key Takeaways

- Review your Critical Illness Insurance Policy thoroughly before considering cancellation.

- Evaluate changes in health, finances, and family responsibilities to determine if your policy still fits.

- Seek advice from financial advisors or insurance experts for tailored guidance.

- Understand the financial implications of cancelling, including the loss of premium investments.

- Before cancelling, consider if adjusting your coverage could be a better solution

- Ensure you follow the correct procedures for cancellation as outlined by your insurer.

- Secure new coverage before cancelling existing insurance to avoid protection gaps.

- Regularly review and update your insurance to align with your current needs.

Your Feedback Is Very Important To Us

Thank you for sharing your experiences. Your feedback is crucial in helping us enhance our understanding and support for individuals dealing with Critical Illness Insurance.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com