- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Partial Withdrawals In Life Insurance: What Counts And How They Work

By Harpreet Puri

CEO & Founder

- 10 min read

- October 27th, 2025

SUMMARY

Partial withdrawals allow access to the cash value in a permanent Life Insurance Policy without cancelling it. The blog explains how Universal Life Insurance and Whole Life Insurance Policies in Canada offer flexibility through accumulated cash value. It outlines the risks, tax implications, and impact on the death benefit. Term Life Insurance Policies are excluded, and real-life uses like retirement income, education, and emergencies are covered.

Introduction

You may feel like the more successful your business, the more at risk you are of losing everything you’ve built. Corporate-Owned Life Insurance can provide a means to secure key people, fund continuity plans and house retained earnings.

No matter if you prefer cheap Life Insurance products or permanent tax-deferral solutions, the important thing is to know your choices.

Corporate-Owned Life Insurance is an attractive solution for Canadian business owners who want both protection and performance. The average Canadian doesn’t realize just how much value is tucked inside his or her Life Insurance Policy. Canadians currently have over $5.3 trillion in Life Insurance in force, according to CLHIA. And a lot of that is thanks to policies with cash value — policies that quietly accumulate wealth over many years, often offering tax relief, sitting there as financial buffers which many families never invade.

But sometimes, life hits hard. Emergencies pop up. And that’s where partial withdrawals get tricky. For those with a Life Insurance Policy in Canada that has accumulated cash value, drawing on that reserve can help — without destroying the whole contract.

Let’s take a closer look at how partial withdrawals work, what they mean for your Life Insurance Coverage and what the true tax implications are.

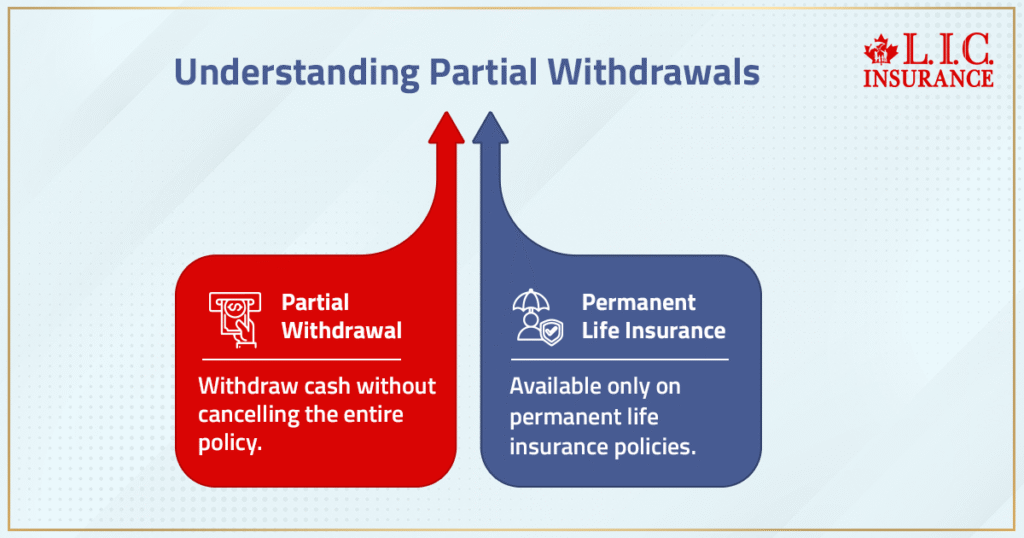

What Is A Partial Withdrawal From A Life Insurance Policy?

A partial withdrawal (also called a partial surrender) means accessing a portion of your Life Insurance Policy’s cash value without cancelling the entire policy. You’re not borrowing the money. You’re literally withdrawing it—like dipping into savings.

But this option is only available on Permanent Life Insurance Policies, such as:

- Whole Life Insurance Policies in Canada

- Universal Life Insurance Plans

Term Life Insurance Coverage, on the other hand, doesn’t have a cash value. So partial withdrawals? Not an option there.

Why Policy Owners Choose To Make A Partial Withdrawal

Canadians use partial surrenders for a variety of reasons, often tied to life’s curveballs or strategic planning. Here’s what we’ve seen:

1. Emergencies Or Financial Hardship

When borrowing money from a bank is either impossible or expensive, the policy owner might access their Life Insurance cash value to:

- Cover medical bills

- Pay for unexpected home repairs

- Get through a temporary job loss

2. Funding A Child's Education

Many Canadian parents use their Whole Life Policy or Universal Life Insurance Policy as a backup RESP. If RESP limits are maxed out, the accumulated cash value can be withdrawn to help with tuition, books, or even a student apartment deposit.

3. Making A Down Payment On A Home

In tight mortgage markets, people look at all angles for liquidity. Tapping into a Life Policy might provide that extra $10K–$20K they need to meet the lender’s minimum.

4. Funding Retirement Income

Many retirees withdraw funds from the policy’s cash value as part of a broader retirement plan, especially when market volatility makes RRIFs risky in the short term.

How A Partial Withdrawal Works

Let’s break it down.

Step 1: Contact The Insurance Company

You (or your insurance agent) contact the insurance company to request a partial withdrawal. They’ll give you a breakdown of:

- Available cash surrender value

- Surrender charges or fees

- Impact on the policy’s death benefit

Step 2: Specify The Amount You Need

You don’t have to withdraw the full cash value. You can request a specific lump sum amount.

Step 3: Submit The Paperwork

The policy owner signs the necessary forms. The funds are usually deposited or sent by cheque within a few business days.

Note: If you have an outstanding loan balance against the policy already, the insurance company might require that to be paid off first or deducted from your available value.

Tax Implications Of Life Insurance Withdrawals In Canada

This is where things get spicy.

Are Partial Withdrawals Tax-Free?

Not always. If the amount you withdraw exceeds the adjusted cost basis (ACB) of the Life Insurance Policy, then yes, you may have to pay income tax on the excess.

What Is The Adjusted Cost Basis?

It’s a formula set by the CRA that factors in your premium payments and any previous policy loans or surrenders. Once the cash surrender value exceeds this ACB, taxes kick in.

What About Policy Loans?

Taking a policy loan against the Life Insurance cash value is typically tax-free. But if the policy lapses or is surrendered while there’s an unpaid loan, you may owe taxes.

Tip: Always consult a tax advisor or financial advisor before making withdrawals.

Impact On The Policy’s Death Benefit And Long-Term Value

Every dollar you withdraw:

- Reduces the accumulated cash value

- May reduce the policy’s death benefit

- Could trigger additional penalties or surrender charges if done within a specified period of opening the policy

Your insurance costs might also increase over time if the remaining cash value can’t support the internal charges of the Universal Life Policy.

So if you withdraw too much or too often, your policy might:

- Shrink in value

- Lose living benefit features

- Or worse, lapse altogether

Alternative Option: Life Settlements

Partial withdrawal not giving you enough liquidity? There’s another door.

A life settlement lets you sell your Life Insurance Policy to a third party in exchange for a larger lump sum. You give up the policy altogether, and the buyer becomes the new policy owner and pays the premiums going forward.

Who Can Consider Life Compromises?

- Age 65+

- Own a Permanent Insurance plan (or convertible Term Life Insurance)

- Have a death benefit of $100,000+

- Possibly in declining health

In some cases, a life settlement can yield 4x–6x more than a partial surrender.

How Much Can You Withdraw?

There’s no universal answer. It depends on:

- Your Life Insurance Policy’s cash value

- Any policy loans or unpaid premiums

- The rules set by your insurance company

Most policy owners can access 60–90% of the accumulated cash value depending on age, policy type, and premium payments.

Final Word From Canadian LIC

We’ve guided more than a few hundred clients through education on Permanent Life Insurance – be it a Universal Life Insurance Plan, a Whole Life Insurance Policy in Canada or even one of the custom hybrids.

Our job is to present to you the real math on your policy—the tax impact, how the cash flow benefit works, and how it’s possible that making a partial withdrawal or taking out a policy loan can actually aid without blowing up the future.

Because life is like that sometimes, but your Life Insurance shouldn’t be.

Contact us today or schedule your strategy session online. Let’s check out your policy, run down your surrender charges and make sure you aren’t left with thousands of tax-sheltered dollars sitting in your Life Insurance Policy — doing no one any good.

More on Life Insurance

- Top Whole Life Insurance Policies In Canada With The Highest Dividends

- Universal Life Insurance Plan Vs Term Life Insurance Plan

- Is There A Limit To a Whole Life Insurance Policy?

- Is There A Penalty For Cancelling Term Life Insurance?

- How Long Does It Take To Get Approved For Term Life Insurance?

- How Many Years Is A Term Life Insurance Policy?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yep. In a Whole Life Insurance Policy in Canada, future dividends may decrease if the policy’s cash value drops too low. Since dividends are often based on how much is inside, a partial withdrawal can mess with growth if you’re not careful. Always ask before touching it.

Not always — but in some Universal Life Insurance Plans, if the policy’s cash value drops below required reserves, you might have to pay premiums just to keep it active. We’ve seen cases where a withdrawal triggered an unexpected premium jump five months later. Sneaky, right?

Yes, it can. Some Life Insurance companies may limit your ability to top up or add more to your Universal Life Insurance Policy once a partial withdrawal has been made. We’ve seen policy owners get capped without warning. Always check before you touch it.

If you’re building your estate around a Life Insurance Policy, pulling from the cash value can shift the final numbers your heirs receive. It might also alter trust distributions or policy ownership outcomes. Estate plans tied to whole life need a second look after any withdrawal.

Once it’s done, it’s done. A partial surrender isn’t a loan — it’s permanent. The funds are gone, and the policy’s cash value doesn’t auto-rebuild unless you feed it. We’ve had policy owners regret acting fast, so breathe and consult before deciding.

They both unlock cash — but one doesn’t involve your house. If your Life Insurance Policy has enough accumulated cash, it can sometimes beat a home equity loan in speed and cost. No bank, no appraisals, no lien. Just paperwork and payout.

If you’ve already done a partial withdrawal from a permanent Life Insurance Policy, it doesn’t impact your rights to convert a Term Life Insurance Policy — but timing matters. Once that conversion window closes, it’s gone. We’ve seen people wait too long and regret it.

Yes. Some policy riders tied to your Life Insurance Policy — especially living benefits — can be reassessed after you touch the cash value. It’s not guaranteed, but we’ve seen insurers flag it. Don’t assume those top-ups will be available post-withdrawal.

You absolutely can. We’ve had clients use Universal Life Insurance Policies to access funds quickly and avoid selling volatile stocks. It’s not just about emergencies — sometimes you spot a window, and your policy’s cash becomes your move.

Yes, and often in ways you wouldn’t expect. Some Universal Life Insurance Plans have internal bonuses based on accumulated cash or how long funds sit untouched. A partial withdrawal can quietly kill that growth track. Always ask before you act.

Key Takeaways

- Partial withdrawals let you access cash value from a Whole Life or Universal Life Insurance Policy without cancelling it entirely. It’s a way to get help now without giving up the future.

- Cash value builds over time in permanent policies — but not in Term Life Insurance Policies, which don’t offer any savings or withdrawal features.

- Withdrawals can impact your death benefit, reduce future policy performance, and may trigger tax implications if you take out more than the adjusted cost basis.

- Policy loans might be a better option than withdrawals in many cases, especially when tax-free access or preserving the full death benefit is important.

- Life settlements are another option, where you sell the policy entirely. They’re worth exploring if you’re 65+, no longer need coverage, and want a larger payout.

- Premium payments may increase or policy performance may drop after repeated or large withdrawals, especially with Universal Life Insurance, where internal charges fluctuate.

- Financial advice is essential before touching your policy’s cash value. Real numbers matter — surrender charges, outstanding loan balances, and rider clauses can all affect the outcome.

- Partial withdrawals are a tool — not a solution by default. Use them intentionally, not emotionally, and only after understanding the trade-offs.

Sources and Further Reading

Official Sources

- Canadian Life and Health Insurance Association (CLHIA)

URL: https://www.clhia.ca/web/CLHIA_LP4W_LND_Webstation.nsf/page/ConsumerInformation

Covers: Canadian Life Insurance market data, types of policies, and financial literacy tools. Frequently cited for total coverage in Canada and policy trends. - Canada Revenue Agency (CRA) – Life Insurance & Taxation

URL: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/financial-institutions/income-tax/information-circulars/ic89-3-policyholders-taxation.html

Covers: Tax implications of withdrawals, adjusted cost basis (ACB), policy loans, and taxable events related to permanent Life Insurance Policies in Canada. - Financial Consumer Agency of Canada (FCAC)

URL: https://www.canada.ca/en/financial-consumer-agency.html

Covers: Guides on understanding Life Insurance Policy options in Canada, how Universal Life Insurance and Term Life Insurance Policies differ, and general consumer protection rules.

Additional Reading & Thought Leadership

- Sun Life Canada – Accessing Cash Value from Permanent Life Insurance

URL: https://www.sunlife.ca/en/tools-and-resources/money-and-finances/understanding-life-insurance/cash-value-in-life-insurance-how-does-it-work/

Covers: Examples of policy withdrawals, cash surrender value, partial surrenders, and when to consider loans or full surrenders. - Manulife – Understanding Your Life Insurance Policy’s Cash Value

URL: https://www.manulife.ca/personal/insurance/life-insurance/understanding-cash-value-life-insurance.html

Covers: Cash value mechanics, policy loans, how to withdraw funds, and surrender charges in Whole Life and Universal Life Insurance Policies. - Empire Life – Policy Withdrawals & Loans Guide

URL: https://www.empire.ca/investment-solutions/insurance/policy-loans-withdrawals

Covers: How policy owners can withdraw or borrow from permanent Life Insurance Policies, including notes on accumulated cash, interest payments, and the policy’s death benefit impact.

Feedback Questionnaire:

We’re glad you took the time to read through. Before you go, help us understand your situation better — so we can offer the right support (not spam).

IN THIS ARTICLE

- Partial Withdrawals In Life Insurance: What Counts And How They Work

- What Is A Partial Withdrawal From A Life Insurance Policy?

- Why Policy Owners Choose To Make A Partial Withdrawal

- How A Partial Withdrawal Works

- Tax Implications Of Life Insurance Withdrawals In Canada

- Impact On The Policy’s Death Benefit And Long-Term Value

- Alternative Option: Life Settlements

- Who Can Consider Life Compromises?

- How Much Can You Withdraw?

- Final Word From Canadian LIC

Sign-in to CanadianLIC

Verify OTP