- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Canada’s Average Income: What You Need To Know

By Pushpinder Puri

CEO & Founder

- 15 min read

- January 13th, 2026

SUMMARY

Many Canadians feel incomes are rising, but savings are shrinking. The post breaks down Canada’s 2026 average income ($64K–$65K), household vs median income, and income by age group. It compares earnings to real cost-of-living budgets and shows how inflation tightens margins. It explains how insurance fits into annual income planning, highlights provincial differences, and shares practical steps to balance protection, savings, and long-term goals.

Introduction

Introduction: The Gap Between Income and Reality

Many Canadians today are feeling like they’re making more money but somehow saving less. Does that sound familiar?

At Canadian LIC, we hear this story all too often. A young couple in Ontario wrote recently about how their combined income had increased over the last three years. But their lifestyle hadn’t changed significantly — and neither had their savings. After paying rent, groceries, child care, insurance, and occasional medical bills, they started wondering, “Where is our money actually going?”

This is the reality for more and more Canadians. That’s also why figuring out the average income in Canada and where it stands next to the average cost of living in Canada is as essential as ever in 2026.

No matter if you are in your 20s and getting ready to get your career off the ground or in your 50s and planning for retirement, knowing where you fall in relation to the average income by age group helps you make better decisions. Especially factoring in basics such as annual income with insurance coverage isn’t free, of course, but neither is lack of coverage.

Let’s parse this out in a way that resonates with the phase of life you’re in.

Average Income in Canada 2026: National Overview

According to the latest data released by Statistics Canada, the average income in Canada in 2026 is estimated to be around $64,000–$65,000 annually, a modest increase from 2026 due to wage growth in healthcare, tech, and skilled trades.

But this figure doesn’t tell the whole story. Income can vary significantly by:

- Province or territory

- Job Sector

- Education level

- Age group

At Canadian LIC, we’ve worked with clients from all corners of the country—from teachers in Saskatchewan to electricians in Newfoundland—and no two stories are alike. What matters is how your income lines up with your expenses, goals, and long-term security.

Average Household Income And Median Income In Canada 2026: What The Numbers Really Show

While individual income figures help establish a baseline, most Canadians don’t manage their finances alone. Rent, mortgages, groceries, childcare, and insurance are usually shared. That’s why understanding the average household income Canada data — and how it compares to the Canadian median income — gives a much clearer financial picture.

In 2026, the average income per household in Canada sits significantly higher than individual earnings because many households rely on two or more income earners. According to national income trends, the average household income in Canada is estimated to be in the $105,000–$110,000 range before taxes, depending on province and household composition.

But averages can be misleading.

That’s where the median income for Canada becomes more useful. Median income represents the midpoint, where half of Canadians earn more and half earn less. In 2026, the Canadian median income is estimated to be closer to $68,000–$70,000 for individuals, which reflects what most people actually experience day to day.

For families, the median family income in Canada and the median household income in Canada paint an even clearer picture. Median household income typically falls below the average household income because high earners skew the average upward. In practical terms, this means many Canadian families are earning less than what headline “average income” numbers suggest, while still facing rising housing, food, and insurance costs.

At Canadian LIC, we see this disconnect often. Two households can earn the same average income per household in Canada, but their financial stability looks completely different depending on debt levels, number of dependents, and insurance planning. That’s why we never rely on averages alone when helping clients plan protection and long-term security.

Understanding the difference between the average household income in Canada, the median household income in Canada, and the median family income in Canada allows Canadians to assess their situation realistically — not based on inflated national averages, but on what most households actually live on.

A Closer Look: Average Income by Age Group in 2026

Knowing the average income by age group gives you context. It tells you what’s typical for someone in your life stage. Here’s a snapshot based on current economic data:

| Age Group | Average Annual Income (2026) |

|---|---|

| 20–24 years | $35,500 |

| 25–34 years | $54,000 |

| 35–44 years | $73,500 |

| 45–54 years | $79,000 |

| 55–64 years | $67,000 |

| 65+ years | $44,500 |

We had a client from Alberta — a 42-year-old mechanic — who said he felt he was falling behind because he hadn’t crossed the $80K mark. He learned that, compared to others his age and in his industry, he was actually doing better than most. It made him feel secure enough to purchase life and disability insurance, which he’d been delaying for years.

On occasion, witnessing the numbers from a national perspective quiets the self-doubt.

The Reality Check: Average Cost of Living in Canada 2026

Income alone doesn’t tell you if you’re financially healthy. You also need to consider the average cost of living in Canada, which continues to rise.

Here’s a general monthly breakdown for an individual living in a city like Toronto, Vancouver, or Calgary:

| Expense Type | Monthly Cost (2026 Estimate) |

|---|---|

| Rent (1-bedroom apt) | $2,300–$2,500 |

| Utilities & Internet | $270 |

| Groceries | $550 |

| Transportation | $200–$300 |

| Insurance (basic) | $150–$250 |

| Misc. (clothing, phone, etc.) | $400–$600 |

| Total Monthly | $4,000–$4,500 |

| Total Annual | $48,000–$54,000 |

So, if you’re earning the average income in Canada of $64,000–$65,000, you may only have around $10,000–$16,000 left annually after expenses, before taxes and long-term savings.

That’s not much. And for families with children, mortgage payments, or aging parents to care for, the margin shrinks even more.

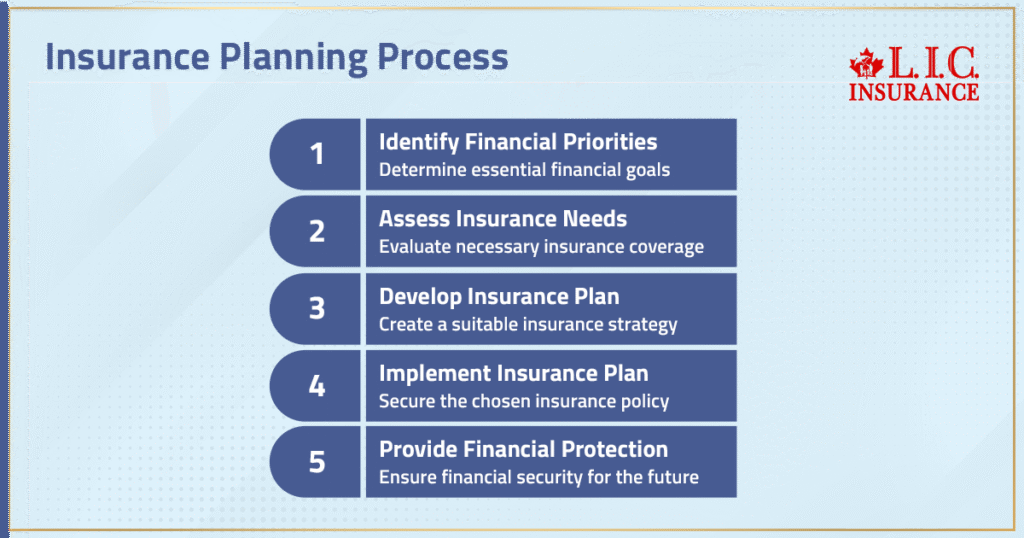

Where Insurance Fits In: Annual Income With Insurance

Insurance isn’t an optional line item—it’s a financial backstop. But we get it. When you’re attempting to spread your income over all of your bills, a few hundred dollars a month for insurance can start to feel like a burden.

As one of our Mississauga clients—a single mom working in healthcare—told us: “I want to cover my son, but I also want to keep the lights on.”

This is the point at which planning becomes really important. Utilizing a cheap term life and critical illness insurance plan, we showed that her annual income would be bolstered by insurance. It cost her around $68/month. That’s $816 a year.

Yes, it’s an added cost. But now, she has financial protection that could change her child’s future if something happens to her.

That’s how LIC does business with its clients, linking income with priorities. We explain how to tweak coverage to match what they actually bring home, not just national averages.

Provincial Differences in Income and Cost of Living

It’s no surprise that where you live in Canada affects both how much you earn and how much you spend.

Here’s a quick comparison of average income and estimated living costs in major provinces:

| Province | Avg. Income (2026) | Annual Cost of Living |

|---|---|---|

| Ontario | $64,300 | $48,000 |

| British Columbia | $61,200 | $50,400 |

| Alberta | $68,900 | $45,600 |

| Quebec | $58,000 | $43,000 |

| Nova Scotia | $54,000 | $41,000 |

| Manitoba | $56,500 | $42,500 |

We helped a family in Montreal evaluate if they could afford a bigger insurance plan. When we compared their income to their cost of living, they were comfortable including critical illness coverage in their plan. Their premium? Only $38/month.

Again, it’s not just about national averages — it’s about making the numbers work where you live.

How Inflation Impacts Income in 2026

Many millions of Canadians live in the economic reality that inflation continues to create. Though wages have risen modestly across much of the economy, prices for things like housing, groceries, and gas have surged even more rapidly. It made the average income in Canada go less far.

We assisted a retired Halifax couple who depended primarily on fixed pension income. Despite having an income that approached the national average, they were struggling more in 2026 than they had just two years prior. Groceries were around 20% more expensive for them. Home heating costs were up more than 15%.

They considered cancelling the life insurance to save money. But after sitting down with our advisor, they changed their policy instead, maintaining their coverage while lowering the premiums. We cooked up simple tweaks to help them manage the bite of inflation without sacrificing protection.

These are the types of personalized, practical conversations that we have every day.

Balancing Income, Insurance, and Long-Term Goals

Most Canadians want to protect their family, save for retirement, and enjoy life, without stressing over every dollar. But that’s easier said than done.

We often guide clients on how to balance their annual income with insurance, savings, and daily needs. Here’s what we usually recommend:

- Review Your Net Income

Start by looking at what you take home after taxes and deductions. That’s your real budget.

- Set a Monthly Insurance Budget

We suggest keeping your total insurance costs under 10% of your monthly take-home pay. For many people, that’s just $100–$200 for life, health, or disability coverage.

- Factor in Emergency Funds

Aim to save at least three months’ worth of expenses. We helped a self-employed contractor in Toronto set this up by automating small weekly deposits from his income. Within eight months, he had a $6,000 cushion and still maintained his coverage.

- Review Your Coverage Annually

Income and expenses change. We recommend that all of our clients review their policies at least once a year. Keeps their plan relevant and affordable.

We know that income can fluctuate. We have a tech consultant in British Columbia who had a banner year in 2023, only to be laid off in 2024. He went back to work in 2026 under significantly reduced pay. As a result of having created his insurance using a buildable structure, we simply tailored his existing coverage to fit this new budget—without building everything from square one.

How Canadians Use Their Income Differently by Life Stage

Your priorities shift as you grow. That’s why we always tie the average income by age group to lifestyle needs when advising our clients.

In Your 20s:

Most clients here want flexibility. They look for starter policies—with low premiums and basic coverage. We helped a 24-year-old client in Ottawa find a term life insurance policy for just $18/month. She wanted coverage for student debt and to lock in low rates while young.

In Your 30s and 40s:

This is usually the busiest time—careers, mortgages, kids. Income is higher, but so are responsibilities. We often see couples looking to combine family coverage with savings plans, like an RESP and RRSP, while sticking to a budget.

One couple from Winnipeg told us they wanted insurance “that works with our kids’ tuition and mortgage payments.” We layered term life with critical illness and adjusted the premiums to fit their income range. That’s what made it doable for them.

In Your 50s and 60s:

Retirement planning becomes the focus. Clients in this age group are often more interested in long-term policies or converting term to whole life insurance. They want security and tax-efficient estate transfer options.

We advised a 58-year-old entrepreneur from Calgary to shift from income-based planning to legacy planning. We tailored a whole life plan to help reduce estate taxes and preserve wealth for his grandchildren.

Key Questions Our Clients Ask at Canadian LIC

We speak to Canadians every day who have one goal—to make the most of their income. Here are the most common questions we hear:

Q: I’m earning just below the average income in Canada. Can I still afford insurance?

Yes, and we help people like you every day. You don’t need a huge policy to start. Even $20–$30/month can offer strong protection. We customize based on your budget.

Q: What’s the smartest way to mix savings and insurance?

Start small and grow over time. Begin with essential coverage. Then, add to your savings as your income rises. We help you build both protection and security together.

Q: Should I cut insurance if inflation gets worse?

No, but you should reassess. Instead of cancelling, you can reduce coverage or adjust benefits. We work with clients to make smart, affordable changes without losing protection.

Q: Does it make sense to spend more on insurance as I earn more?

Yes—if your responsibilities grow. Higher income usually means more assets and dependents. We help you scale your plan so it always fits your lifestyle.

Final Words: Understanding Income Means Taking Control

It’s hard not to feel overwhelmed by national averages, escalating costs, and economic uncertainty. But once you know your real numbers — your income, your expenses, your use of them — you start taking control.

You have the average income in Canada to give you a baseline. The average cost of living in Canada lets you know the minimum you need to survive. Average income by age group helps reveal how you compare with others in your stage of life. And if you work for a company that provides annual insurance coverage, it allows you to defend your future at every income level.

Every Canadian deserves the right advice — advice that is tailored to them, honest, and helpful. That’s how we’ve been able to help thousands make smart, affordable decisions for their families.

You don’t have to make six figures to feel secure financially. You’re just missing the right plan — and, as always, the right people beside you.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

In 2026, the average salary in Canada is approximately $64,000–$65,000 per year. However, this number changes based on age, location, and industry. However, this number changes based on age, location, and industry. Many clients we speak to earn less or more, depending on their job and where they live.

A falling average yearly income refers to the impact of inflation and reduced job hours in some sectors. Even if gross salaries haven’t dropped, rising expenses make income feel smaller. We’ve had clients say, “It feels like my money doesn’t go as far anymore,” and we’ve seen this trend growing.

Average income includes all types of income—salary, bonuses, freelance earnings, and more. An annual salary is just what you earn from your job as a fixed yearly amount. At Canadian LIC, we always look at the full income picture before giving insurance advice.

The average Canadian salary in 2026 is slightly above $64,000, but in major cities, the cost of living can absorb most of that income. We’ve had young clients in Toronto say they struggle to save even with decent pay. That’s why we help them budget for insurance within their take-home income.

Some of the highest-paying Canadian job sectors in 2026 include:

- Technology

- Healthcare

- Engineering

- Financial services

- Legal professions

Clients working in these sectors often seek more insurance coverage to match their growing responsibilities and income.

In 2026, the fastest-growing industries include:

- Clean energy

- Artificial intelligence

- Cybersecurity

- Senior healthcare

- E-commerce and logistics

We often help clients in these industries build financial protection early while their income is rising quickly.

Yes. The gender income gap in Canada remains a concern in 2026. On average, women still earn less than men in similar roles across various sectors. At Canadian LIC, we’ve helped many women plan ahead financially by customizing affordable policies based on their unique income levels and future goals.

Different roles, risks, and skill requirements cause income gaps across different Canadian job sectors. For example, someone in construction may have a seasonal income, while someone in tech has a steady monthly salary. That’s why we always adjust insurance plans to fit each client’s income style.

No. Many Canadians earn below the average income, but they still build strong financial plans. It’s more about managing what you earn, not how much you earn. We’ve helped part-time workers and freelancers create insurance plans that protect their families without breaking the bank.

Yes. Even if you earn less than the average salary, you can still afford insurance. We offer flexible plans starting as low as $15/month. Our advisors work with people across all income levels to build coverage that fits real life.

Key Takeaways

- The average income in Canada in 2026 is approximately $62,800, but this varies based on age, location, and occupation.

- Rising expenses are making many Canadians feel like their income isn’t going as far, even when salaries go up—a clear sign of a falling average yearly income in real value.

- The average cost of living in Canada is between $44,000 to $50,000 per year for a single adult in most urban centres, leaving a limited margin for savings and insurance.

- Understanding your income compared to the average income by age group helps you plan better. For example, Canadians aged 35–44 earn around $71,000, while those 65+ earn closer to $43,000.

- Income levels and expenses vary across provinces. Earning the average salary in Canada doesn’t guarantee financial ease in high-cost cities like Toronto or Vancouver.

- The gender income gap still exists in many industries, with women earning less on average than men, even in equal roles.

- People working in different Canadian job sectors like tech, healthcare, and skilled trades tend to earn more than those in retail or hospitality.

- The fastest growing industries in 2026 include clean energy, AI, cybersecurity, logistics, and senior healthcare—sectors with higher income potential.

- It’s important to understand how your annual salary supports essential expenses like insurance, savings, and debt. This helps build financial security.

- At Canadian LIC, advisors work closely with clients from all income levels to tailor insurance plans that match their real budget, no matter where they fall on the income scale.

Sources and Further Reading

1. Statistics Canada – Wages, Salaries and Income Data

Website: https://www.statcan.gc.ca

Why it’s useful: It offers the most recent and reliable data on the average income in Canada, wage trends, income by province, age, gender, and employment sector.

2. Government of Canada – Job Bank Labour Market Insights

Website: https://www.jobbank.gc.ca

Why it’s useful: It provides data on the average salary in Canada, job trends by province, and information on the fastest growing industries and wage changes across different Canadian job sectors.

3. Canadian Centre for Policy Alternatives – Gender Pay Gap Reports

Website: https://www.policyalternatives.ca

Why it’s useful: Offers in-depth research on the gender income gap in Canada, including causes, implications, and policy recommendations.

4. Fraser Institute – Economic Research on Income & Cost of Living

Website: https://www.fraserinstitute.org

Why it’s useful: Analyzes changes in Canadian cost of living, tax burden, and purchasing power in different provinces.

5. Ontario Living Wage Network – Living Wage Reports

Website: https://www.ontariolivingwage.ca

Why it’s useful: It offers data on the real cost of living and how the average salary compares to what is needed to live comfortably in Ontario and other provinces.

6. Conference Board of Canada – Labour Market Outlook

Website: https://www.conferenceboard.ca

Why it’s useful: Regularly publishes national and provincial insights on average Canadian salary, workforce demand, and the performance of fastest growing industries.

7. Canada Mortgage and Housing Corporation (CMHC) – Housing Affordability Data

Website: https://www.cmhc-schl.gc.ca

Why it’s useful: It helps explain how housing costs affect the cost of living, especially for individuals and families earning the average income.

8. Globe and Mail / Financial Post – Canadian Personal Finance Columns

Websites:

- https://www.theglobeandmail.com

- https://www.financialpost.com

Why they’re useful: They publish ongoing analysis, opinion pieces, and expert interviews about income trends, salary expectations, and job market movement.

Your Feedback Is Very Important To Us

We’re working to better understand the challenges Canadians face when it comes to income, cost of living, and financial planning in 2026. Please take a moment to share your feedback.

Thank you for your time! Your answers will help us support Canadians like you in making informed, confident financial decisions in 2025 and beyond.

IN THIS ARTICLE

- Canada's Average Income: What You Need To Know

- Average Income in Canada 2026: National Overview

- Average Household Income And Median Income In Canada 2026: What The Numbers Really Show

- A Closer Look: Average Income by Age Group in 2026

- The Reality Check: Average Cost of Living in Canada 2026

- Where Insurance Fits In: Annual Income With Insurance

- Provincial Differences in Income and Cost of Living

- How Inflation Impacts Income in 2026

- Balancing Income, Insurance, and Long-Term Goals

- How Canadians Use Their Income Differently by Life Stage

- Key Questions Our Clients Ask at Canadian LIC

- Final Words: Understanding Income Means Taking Control

Sign-in to CanadianLIC

Verify OTP