- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Canada Tax Filing Checklist 2025: What You Need Now And What Is Changing In 2026

By Harpreet Puri

CEO & Founder

- 13 min read

- February 18th, 2026

SUMMARY

A detailed look at the Canada tax filing checklist 2025 with tax planning Canada strategies, capital gains tax changes for 2026, and key updates affecting taxable income, RRSP contribution decisions, Canadian Tax Free Savings Account planning, and charitable donations. Covers income sources, medical expenses, business expenses, and Canadian personal tax filing tips to strengthen your financial position.

Introduction

Every year, the arrival of tax season is as surprising as ever to the Canadian population: it always comes with a bang, and it is always sooner than you can imagine. The Canada Revenue Agency (CRA) reports that over 30 million people submitted personal income tax returns last year, and every filing season opens up new rules, new contribution room and new tax implications that can have an impact on both your financial situation and entire financial picture. These are some of the hard-working families that we are meeting on a daily basis, and they are overwhelmed, not because they do not understand how to do the taxes, but because there is already too much happening in their lives.

One of those years is 2025, and it is really worth considering having things planned early, which will be beneficial. And with such profound changes making their way in 2026, capital gains tax in particular, being prepared is no longer a choice but a strategic tax planning Canada deserves at the moment.

You have your Canada tax filing checklist 2025 in this guide, which we are writing just like we speak to our clients, straight, sensible and worried about keeping your family financially well.

Canada Revenue Agency: What Documents To Collect Before You File

The best way to reduce stress at tax time is to start with the right documents. Pulling together your past paperwork may not be exciting, but it saves hours later.

Here’s what we ask our clients to gather before filing:

✔️ Your previous year’s tax return

This helps identify income sources, tax credits, tax slips, and deductions you claimed earlier. It keeps your tax year consistent and avoids missing items.

✔️ Your latest CRA Notice of Assessment

This shows:

– updated RRSP contribution room

– unused losses

– taxes owed or refund amounts

– correspondence from the Canada Revenue Agency CRA

✔️ Federal tax slips

You may receive several depending on your income sources:

– T4: Employment income

– T5: Investment income

– T3: Mutual funds and trusts

– T4RSP: RRSP withdrawals

– T4A(P): Canada Pension Plan benefits

– T2202: Tuition

– T5013: Partnership income

✔️ Other tax documents

These often determine your largest deductions and credits:

– professional dues

– medical expenses

– charitable donations

– employment expenses

– rental income statements

– property taxes

– investment counsel fees

Having proper documentation is half the battle. And when you bring these to your tax professional, everything moves quicker — and cleaner.

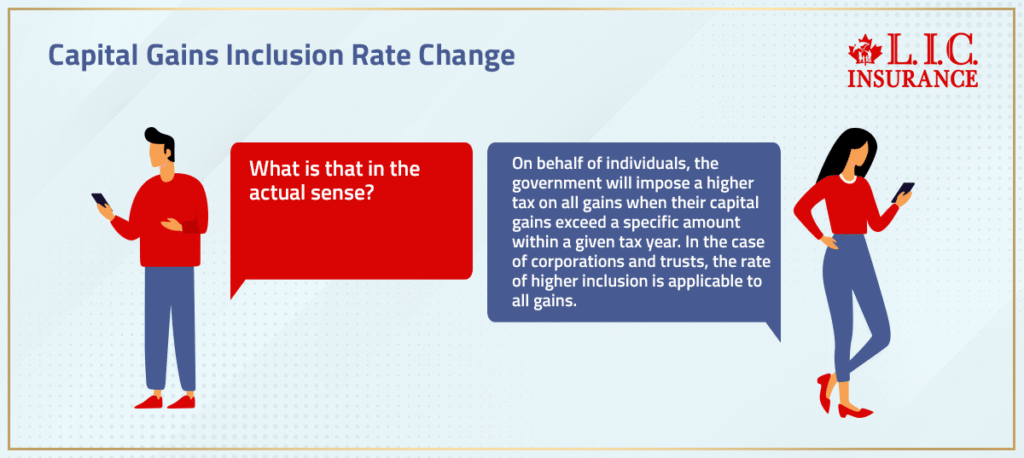

Capital Gains Tax: What’s Changing For 2026 (And What You Should Do Now)

The debate that has been the subject of the Canadian financial news is the proposed raising of the capital gains inclusion rate. The government officially announced its postponement of the change to January 1, 2026, although the change was originally planned to be effective in mid-2024.

What is that in the actual sense?

On behalf of individuals, the government will impose a higher tax on all gains when their capital gains exceed a specific amount within a given tax year. In the case of corporations and trusts, the rate of higher inclusion is applicable to all gains.

This affects:

– publicly traded securities

– real estate (not your principal residence)

– business sales

– investments with long-term investment growth

If you’re planning a major sale in 2025, the timing now has clear tax implications. We walk clients through the fair market value, what counts as investment income, and strategies to minimize tax liability during this transition year.

The takeaway?

2025 is your year for thoughtful, proactive tax planning.

Income Tax: Understanding Your Main Sources And Slips

Your income tax bill depends entirely on how your income is structured. Canadians often underestimate this part — but it influences deductions, credits, and even benefits.

Key income sources include:

– employment income (T4)

– rental income

– investment income (T3, T5)

– self-employed business income

– mutual funds

– RRIF withdrawals

Different income types trigger different tax brackets, tax credits, and tax deductions. This impacts your taxes owed and overall tax savings. Getting this right improves your entire personal tax situation.

Medical Expenses: What Counts And What Most Canadians Miss

Medical expenses remain one of the most misunderstood areas of personal income tax. You can claim far more than most people realize.

Eligible items include:

– prescription drugs

– dental services

– travel for medical treatment

– health insurance premiums (in some cases)

– medical devices

– attendant care

– disability support

You may receive more tax benefits upon having a disability tax credit, for which you or a relative qualifies. These credits are non-refundable, which implies that they lower your taxable amount yet fail to establish a refund of their own.

The money left unclaimed by many households is the reason why they did not follow receipts. And not to do that in 2025, particularly as health costs are on the increase.

Canada Pension Plan: Why CPP Slips Matter For 2025 Filing

Retirement income sources shape your taxable income differently.

CPP benefits reported on T4A(P) impact:

– marginal tax brackets

– OAS clawback potential

– RRSP strategy

– future retirement income planning

We remind clients that their CPP income interacts with their Registered Retirement Savings Plan contributions. Reviewing both together gives a clearer picture of how to optimize your RRSP contribution room and overall tax savings.

Business Expenses: What The Self-Employed Must Prepare For 2025

If you’re self-employed, tax filing becomes more complex — but also more flexible.

Common deductible business expenses include:

– vehicle expenses

– meals (50%)

– home office

– equipment and supplies

– accounting software

– advertising

– subcontractors

– bank fees

These assist in cutting down the net business finances, which reduces your taxes.

Self-employed people need to have record-keeping, and the inability to find the receipt is the first cause of people overpaying. Good bookkeeping translates to superior tax planning and fewer surprises.

RRSP Contribution: What To Do Between Now And March 2025

RRSPs remain one of Canada’s most effective tax savings tools.

You can contribute up to your available RRSP contribution room, and contributions made in the first 60 days of 2025 apply to the 2024 tax year.

RRSP strategies help reduce:

– taxable income

– tax bill

– income tax in high-income years

And even if you don’t contribute yet, you want to track your contribution room and match it to your long-term financial goals.

Charitable Donations: What You Can Claim In 2025

This applies whether you donate monthly, annually, or spontaneously.

You can claim:

– charitable donations made to registered charities

– official receipts

– payroll deductions

Increased amounts of donation are charged with high interest rates. The better you plan your gifts to charity, the more favourable the contribution to the government in terms of tax.

The little bits of charity you can give out mean a lot- particularly with provincial credits.

Family Members: Credits, Benefits, And Shared Tax Strategies

Families have unique ways to lower their collective tax burden.

Strategies we help clients consider include:

– pooling medical expenses

– optimizing childcare deductions

– transferring credits between family members

– income splitting (legally allowed situations)

– reviewing TFSA contribution room

– coordinating Tax Free Savings Account strategies

The CRA will verify the TFSA contribution limit in 2025 shortly, and we will always advise our clients to get ahead of the game as soon as the official figure is announced.

A small amount of planning during tax time can transform your whole financial year into a blended, growing, or multigenerational family.

Income Sources: A Full Checklist For 2025 Filing

Here’s a clean, ready-to-use list our clients rely on:

☑️ employment income

☑️ investment income

☑️ rental income

☑️ retirement income

☑️ self-employment

☑️ mutual funds

☑️ foreign income

☑️ capital property sales

☑️ business finances

☑️ property taxes

☑️ government benefits

Cross-check this list early so nothing slips through the cracks.

What’s Changing In 2026: The Capital Gains Inclusion Rate And Alternative Minimum Tax

Two major changes arrive in 2026 that may significantly affect your taxes:

1. Higher capital gains inclusion rate

A larger portion of your gain becomes taxable.

2. Changes to the alternative minimum tax (AMT)

Minimal tax could increase on high-income households, based on the investment income and deductions made.

We are already assisting customers in configuring investment portfolios, re-evaluating their fair market values, and synchronizing sales with their long-term objectives in 2025-2026.

The Role Of Tax-Free Savings Accounts And Home Savings In Your 2025–2026 Plan

A Canadian Tax Free Savings Account is an investment-growth environment that is flexible and tax-free. Although the TFSA contribution limit for 2025 has not been confirmed yet, the total TFSA contribution room is to be reviewed annually.

The first home savings account (FHSA) and home savings account provide new opportunities (tax deductions, tax-free growth, and withdrawals) in case you are planning to purchase a home.

These are the accounts that can be strong when they are applied strategically with the RRSPs, particularly in a larger tax planning plan.

How We Help You Stay Ahead During Tax Time

Our role isn’t just to hand you a checklist — it’s to coach you through the financial decisions that shape your entire tax year.

Clients rely on us to:

– simplify taxes

– Review personal tax returns

– prepare for new legislation

– optimize deductions

– coordinate income for family members

– analyze tax implications

– reduce tax liability

– strengthen their financial position

We keep things honest, simple, and tailored to your real life — not cookie-cutter advice.

Conclusion: Your 2025 Filing Sets Up Your 2026 Tax Strategy

2025 is a transition year. These regulations are today gearing Canadians towards the largest tax change since the start of the twenty-first century, the capital gains inclusion rate increase.

The smartest move?

Get organized now. Plan conversations over tax planning. Know where you will get your income. Review your documents early. And be ready for the changes of 2026, many years ahead.

We are here to assist you in every detail, to be calm, to be straight and to have the financial stability of your family in mind.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Begin by examining the financial events of the year that influenced you- changes in your income or employment, new investment income or the situation of your family members. This provides a better perspective of your tax planning Canada strategy without contacting forms. It is there that you can determine which tax credits or tax deductions are new that you may be eligible to receive. It is an economical method of saving taxes without being bogged down in documentation.

The majority of Canadians pay too much because they fail to review their complete personal tax picture at the beginning. Noticeable savings can be made by a mere examination of the way your income sources are interacting with deductions. The simplest changes in timing or classification of expenses can decrease your tax bill. We take this process step by step with a strategy-first approach, rather than a last-minute stress strategy with clients.

The changes will impact the capital planning in the long term since capital gains will have a direct influence on your taxes to pay in the years to come, particularly when large assets are concerned. Knowing your fair market value today will assist you in projecting the most effective schedule of selling. The idea is to match the income of investment with the new inclusion rate in a manner that saves your financial standing. It is then that astute tax planning is necessary.

The alternative minimum tax does not only apply to high-net-worth households; it may happen suddenly because of certain deductions as well as specific sources of income. Its impact is sometimes felt in families whose investment portfolio or larger charitable contribution does not make them realize it. It is all about striking a balance between deductions so that the minimum tax does not take away your strategy of choice. The advance planning will save unpleasant surprises in the tax year.

Certainly, being an independent business owner requires you to pay a lot in taxes to the government because you must be very precise in order to declare expenses and earnings when they occur. A small lapse in documentation can affect non-refundable tax credits and the general tax cuts. An active business expense system assists in stabilizing incomes/taxes in changing months. It also gives your financial position a lot of strength even after tax time.

Yes, most particularly when you are planning it according to your income level and when it falls within the tax year. The interactivity of the donations with other tax credits can have a positive outcome, which forms a more powerful benefit. The effect can become more powerful when you organize contributions with family members. An organized strategy of donations to charities allows for being more economically efficient.

This is because your Tax Free Savings Account does not reflect on your tax returns, but certainly influences long-term plans on tax planning in Canada. The way you spend your TFSA contribution room may affect the growth of investments in non-taxable accounts. Even later, when the contribution limit to the TFSA is not confirmed in 2025, it is worth aligning the contribution limit with your larger goals. TFSA can be optimized effectively when combined with the RRSP contribution plans in the balance of tax planning.

Landlords usually do not take into account that rental income is related to such deductions as repairs, interest, and property taxes. Real-time monitoring of fair market conditions and expenditures makes it clean at the time of filing. This is aimed at preventing mismatches that make tax returns unnecessary. By maintaining systematic records, rental revenues will be predictable instead of being a stressful factor.

The interaction of investment income with tax levels and credits offered to first-time investors is a factor that they should consider. Trading at the right time will impact the exposure to capital gains tax, particularly concerning the new regulations that will be effective in 2026. Early review of securities statements of publicly traded securities prevents errors in the future. It is all a matter of creating a disciplined basis of long-term investing.

A tax professional is significant in case you have experienced variations in the sources of income, growth in the investment or any significant life occurrences. Complicated matters may change your tax bill or cause you to lose some tax benefits you may overlook. An expert will assist you in making sure that you do not make the usual errors that will result in re-evaluation. In some cases, professional assistance is the most wholesome step to take, especially when the family desires clarity.

Key Takeaways

- Getting organized early makes tax season easier. Pulling together tax slips, previous year’s tax return, and CRA documents helps avoid missed deductions and strengthens your tax planning Canada strategy.

- 2025 is a transition year for major tax changes. The upcoming 2026 shift in the capital gains inclusion rate means Canadians should review investment income, timing of sales, and long-term plans with care.

- Your income sources shape your entire tax year. Employment income, rental income, business finances, and investment income each affect tax credits, taxable income, and overall tax liability differently.

- Families benefit from coordinated filing. Pooling medical expenses, aligning charitable contributions, and reviewing Tax Free Savings Account strategies help family members lower their collective taxes.

- Self-employed individuals must stay meticulous. Accurate tracking of business expenses, vehicle expenses, and proper documentation is essential for maximizing deductions and protecting your financial position.

- RRSP contribution decisions matter. Reviewing RRSP contribution room early supports stronger tax savings and better long-term retirement planning.

- Tax-free accounts remain powerful tools. The Canadian Tax Free Savings Account and first home savings account help Canadians grow investments tax free while aligning with future home or retirement goals.

- 2026 will reshape the tax landscape. The new capital gains tax rules and adjustments to minimum tax make proactive tax planning crucial for anyone managing investments or preparing major financial moves.

Sources and Further Reading

Canada Revenue Agency – Personal Income Tax

Covers income tax rules, tax slips, credits, deductions, and filing steps.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals.html

CRA – Tax Slips (T4, T5, T2202, etc.)

Details on each slip required for the Canada tax filing checklist 2025.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-slips.html

CRA – Notice of Assessment & RRSP Contribution Room

Where taxpayers can verify their RRSP contribution room and previous year data.

👉 https://www.canada.ca/en/revenue-agency/services/e-services/e-services-individuals/account-individuals.html

CRA – Medical Expenses You Can Claim

A complete list of eligible medical expenses for tax credits.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/medical-expenses.html

CRA – Disability Tax Credit

Official details on eligibility and claiming the DTC.

👉 https://www.canada.ca/en/revenue-agency/services/disability-tax-credit.html

CRA – Charitable Donations Tax Credit

Information on claiming donations and which receipts are eligible.

👉 https://www.canada.ca/en/revenue-agency/services/charities-giving/charities/donating-tax-credit.html

CRA – Capital Gains & Inclusion Rate Rules

Details on capital gains tax, inclusion rate, and reporting.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/capital-gains.html

Department of Finance – Federal Budget Tax Measures

Updates on capital gains changes and alternative minimum tax (AMT).

👉 https://www.canada.ca/en/department-finance/news.html

CRA – Alternative Minimum Tax (AMT)

Explains how AMT is calculated and who may be affected.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/alternative-minimum-tax.html

CRA – Business Expenses for Self-Employed Individuals

Information on deductible business expenses and record-keeping.

👉 https://www.canada.ca/en/revenue-agency/services/tax/businesses/small-businesses-self-employed-income.html

CRA – Rental Income Guide

How to report rental income and claim related expenses.

👉 https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4036.html

Financial Consumer Agency of Canada – Tax Planning Basics

Neutral tax planning guidance and financial literacy tools.

👉 https://www.canada.ca/en/financial-consumer-agency/services/managing-money/taxes.html

CRA – TFSA Rules & Contribution Room

Official rules on Tax Free Savings Accounts and contribution rules.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account.html

CRA – First Home Savings Account (FHSA)

Details on FHSA structure, contributions, and withdrawals.

👉 https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html

CPP Benefits (T4A(P) Slip Information)

Explains how CPP benefits impact taxable income.

👉 https://www.canada.ca/en/services/benefits/publicpensions/cpp.html

Feedback Questionnaire:

We’d love to understand your experience and the challenges you face with tax filing in Canada.

Your feedback helps us guide families with clearer, more practical tax planning support.

IN THIS ARTICLE

- Canada Tax Filing Checklist 2025: What You Need Now And What Is Changing In 2026

- Canada Revenue Agency: What Documents To Collect Before You File

- Capital Gains Tax: What’s Changing For 2026 (And What You Should Do Now)

- Income Tax: Understanding Your Main Sources And Slips

- Medical Expenses: What Counts And What Most Canadians Miss

- Canada Pension Plan: Why CPP Slips Matter For 2025 Filing

- Business Expenses: What The Self-Employed Must Prepare For 2025

- RRSP Contribution: What To Do Between Now And March 2025

- Charitable Donations: What You Can Claim In 2025

- Family Members: Credits, Benefits, And Shared Tax Strategies

- Income Sources: A Full Checklist For 2025 Filing

- What’s Changing In 2026: The Capital Gains Inclusion Rate And Alternative Minimum Tax

- The Role Of Tax-Free Savings Accounts And Home Savings In Your 2025–2026 Plan

- How We Help You Stay Ahead During Tax Time

- Conclusion: Your 2025 Filing Sets Up Your 2026 Tax Strategy

Sign-in to CanadianLIC

Verify OTP