- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Understanding The Long Term Care Insurance Market In Canada

By Pushpinder Puri

CEO & Founder

- 13 min read

- June 23rd, 2025

SUMMARY

Canadian LIC shares expert insights on the Long Term Care Insurance market in Canada, covering coverage options, cost factors, eligibility, real-life planning examples, and how insurance protects retirement savings. Backed by 14+ years of client experience, the content helps Canadians understand why Long Term Care Insurance is essential in 2025 and how to choose the right plan to secure their health, dignity, and financial future.

Introduction

One medical emergency or age-related diagnosis can instantly turn a financially independent person into someone who needs full-time care, and we’ve seen how quickly it can drain a lifetime of savings. At Canadian LIC, this is one of the hardest realities we face with our clients. Families come to us after watching loved ones struggle to afford the care they need, often too late to put coverage in place. Long Term Care Insurance isn’t just a product — it’s a plan for preserving dignity, independence, and financial stability when life takes a difficult turn.

In this detailed insight, we share everything you need to understand about the Long Term Care Insurance market in Canada, based entirely on over 14 years of direct client experience, evolving policy options, and the day-to-day financial challenges Canadians face.

What Is Long Term Care Insurance?

Long Term Care Insurance (LTCI) provides coverage for services not typically covered by provincial health plans, such as assistance with daily living activities (bathing, dressing, eating) either in a private facility, home care setting, or nursing home.

At Canadian LIC, we often see confusion around what government healthcare will actually cover. The truth is, most Canadians think care is free, isn’t it? Without insurance, families often pay out of pocket or become full-time caregivers themselves.

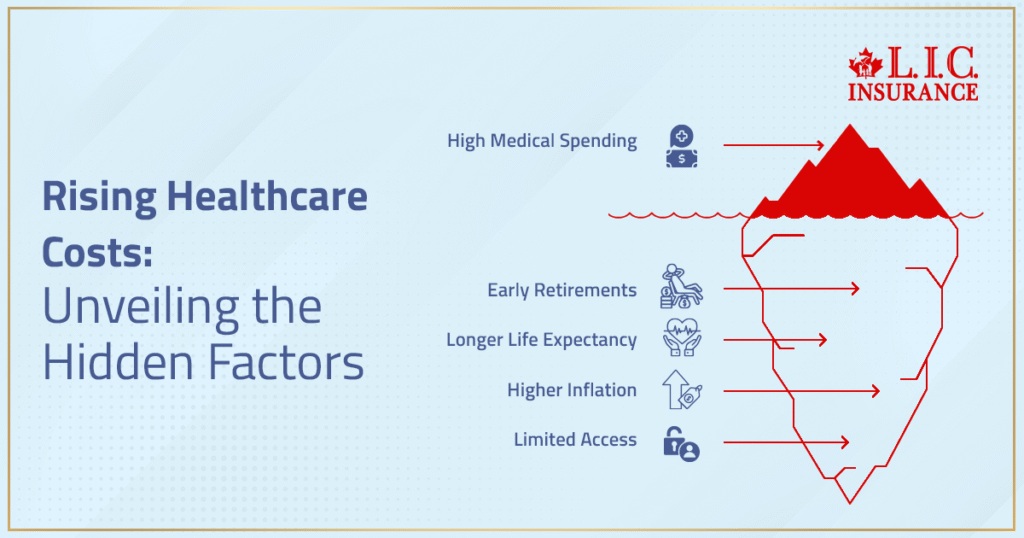

Why Canadians Need Long Term Care Insurance in 2025

With Canada’s aging population, demand for long-term care is rising fast. A growing number of our clients are asking: “Will my retirement plan be enough if I need daily support?”

Here’s what we’re seeing on the ground:

- More early retirements due to health concerns

- Longer life expectancy is driving up long-term care costs

- Higher inflation is putting pressure on out-of-pocket medical spending

Limited access to subsidized nursing homes and long waitlists

These trends are why families now approach us not only for life or disability insurance, but specifically for long-term care planning.

Types of Long Term Care Insurance Options in Canada

We help our clients choose from several Long Term Care Insurance formats based on budget and goals:

1. Stand-Alone Long Term Care Insurance

A dedicated policy that pays a weekly or monthly benefit once the policyholder can’t perform two or more daily living activities.

- Benefit amounts are customizable.

- Premiums may be level or increasing.

- It may include inflation protection or return-of-premium features.

2. Riders Added to Life Insurance

Long-term care riders are attached to whole or universal life insurance.

- Clients can access a portion of their death benefit early to fund care.

- Often used by those who want dual-purpose protection.

3. Critical Illness with Long-Term Care Features

Some critical illness plans offer long-term care support for chronic illnesses.

- Pays out lump sums if a condition requires prolonged care.

- It helps offset home care or support worker costs.

Each option works best for different life stages. At Canadian LIC, we sit down with clients to understand their family history, savings, and medical risks before recommending a plan.

How Much Does Long Term Care Insurance Cost in Canada?

The cost depends on several factors:

- Age and health at the time of application

- Chosen benefit amount and duration

- Optional riders (like inflation protection)

We typically advise clients to apply before age 60 for more affordable premiums. Waiting until symptoms appear usually results in either very high rates or a denial altogether.

We also review government programs like the Canada Caregiver Credit or provincial tax credits to offset expenses, but remind clients that those programs don’t cover everything.

Real Client Story: Why Planning Early Matters

A couple in their early 50s came to us after watching the husband’s mother go through early-onset dementia. She had no coverage, and her care expenses exceeded $100,000 over three years.

We helped the couple secure joint long-term care riders on their universal life policies. They now have peace of mind knowing they won’t leave the same burden on their children.

What Long Term Care Insurance Covers (and What It Doesn't)

Typically Covered:

- In-home care (personal support workers, nurses)

- Long-term care facilities or private nursing homes

- Rehabilitation and therapy services

- Support for activities of daily living (ADLs)

Not Covered:

- Pre-existing conditions not disclosed at the application

- Cosmetic or elective treatments

- Temporary care or hospitalization

- Care is not medically necessary

At Canadian LIC, we break this down with clients, so there are no surprises later.

Who Should Consider Long Term Care Insurance?

We recommend Long Term Care Insurance to:

- People in their 40s to early 60s — while premiums are still affordable

- Self-employed individuals without employer-sponsored benefits

- Clients with a family history of Alzheimer’s, stroke, or Parkinson’s

- Anyone with retirement savings wants to protect

It’s not about fear — it’s about preparing with confidence.

Key Features to Look For When Comparing Plans

We guide clients to compare:

- Elimination Periods: How long before benefits start?

- Daily/Weekly Benefit Amounts: Will it match the cost of care?

- Benefit Duration: Lifetime vs. limited term?

- Inflation Protection: Will your benefit still be enough in 20 years?

- Return of Premium: Will your family get money back if you don’t use the policy?

These small details make a massive difference later. Our job is to make sure nothing gets missed.

Long Term Care Insurance and Retirement Planning

Too often, clients focus only on saving for retirement, not protecting it. We integrate Long Term Care Insurance into every financial plan we build, especially for clients nearing retirement. A $150,000 RRSP can disappear in 18 months of private care if no insurance is in place.

That’s why we help families view LTCI not as an “extra” but as a core pillar of retirement protection.

The Role of Canadian LIC in Long-Term Care Planning

Every family we meet has a different story, health background, and level of preparedness. Our team at Canadian LIC goes beyond brochures and quotes — we:

- Review your health and financial profile

- Recommend carriers that suit your goals (Manulife, Sun Life, RBC, etc.)

- Compare premiums and plan structures

- Assist with applications, disclosures, and annual reviews

- Act as an advocate during claim time, ensuring you get paid fast

We don’t just help you buy coverage. We help you understand it, use it, and protect your family with it.

Final Word

Long Term Care Insurance is often overlooked — until it’s too late. But with rising costs, longer lifespans, and limited government support, planning ahead isn’t optional anymore. It’s necessary.

At Canadian LIC, we’re proud to guide Canadians through this process with clarity, compassion, and real-life experience. If you’ve been putting this off, don’t wait for a crisis. Let’s talk.

We’ll help you create a long-term care strategy that keeps your future — and your family — secure.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs – Long Term Care Insurance in Canada

We’ve had clients panic when hearing about a merger or acquisition involving their insurance provider. The good news? Your contract stays legally binding. However, we always review policy terms annually with our clients to ensure you’re aware of administrative changes, claim submission contacts, or any shift in service standards. When something changes on the back end, we help you stay protected on the front end.

Yes—but it depends on how recent the treatment was and how stable your condition has been. We’ve helped several clients who disclosed anxiety, depression, or PTSD history still get approved by selecting the right carrier. At Canadian LIC, we work closely with underwriters, provide clear documentation, and coach clients on what to expect during the health interview. It’s not always a disqualifier.

Absolutely. Your policy follows you nationwide. That said, not all services are priced the same across provinces. For example, private home care in BC might cost more than in Manitoba. We help our clients plan for this in advance and often recommend flexible benefit structures that won’t penalize you based on where you live or move to later in life.

It depends on the policy terms. Some insurers allow compensation to family caregivers under formal agreements or if they’re registered support workers. We help clients structure this properly — from CRA implications to service agreements — so loved ones can be paid fairly without jeopardizing benefit eligibility or tax status.

We hear this concern often, especially from healthy, active individuals in their 40s and 50s. While some plans don’t offer refunds, others include a return of premium or death benefit option. More importantly, we help clients understand that insurance isn’t about loss — it’s about protection. If you don’t need it, that’s the best-case scenario. But if you do not have it, it can derail everything you worked for.

Some plans offer premium flexibility during financial hardship, but not all. That’s why we guide clients to choose policies with built-in grace periods, reinstatement clauses, or limited pay options (like paying premiums for only 10 or 20 years). We also help set up pre-authorized debit buffers so coverage doesn’t lapse accidentally during tough times.

Yes, if you qualify before diagnosis. However, what many people don’t realize is that early cognitive decline is often subtle and missed during applications. At Canadian LIC, we train our advisors to spot early warning signs in family history and guide clients toward early applications — before diagnosis closes the door. We also push for cognitive assessments where necessary.

Yes — and they’re not interchangeable. We’ve had clients who assumed their group disability plans would cover them during old age. They won’t. Disability insurance replaces income, typically until age 65. Long Term Care Insurance covers services needed after that, when daily function declines due to aging or illness. We help clients structure both for continuous protection throughout life.

Yes, as long as they qualify medically and sign the application themselves. We often see adult children who want to take responsibility for their aging parents’ future. We make the process simple by setting up joint consultations, assisting with paperwork, and structuring payment options so the child funds the premiums while the parent remains the policyholder.

When a claim arises, it’s often an emotional and stressful time for families. That’s why we step in directly — helping gather medical reports, coordinate assessments, and speak with claims examiners on your behalf. We don’t walk away after the sale. Our team stays on to ensure you get the benefits you’re entitled to — as fast and as smoothly as possible.

Key Takeaways

- Long Term Care Insurance fills the gap left by government health plans by covering services like home care, personal support, and nursing facilities.

- The need for long-term care is rising across Canada due to aging demographics, longer life expectancy, and increasing healthcare costs.

- There are multiple types of long-term care coverage options including stand-alone policies, riders on life insurance, and critical illness plans with extended care features.

- Cost varies by age, health, benefit structure, and optional add-ons like inflation protection or return of premium. Applying before age 60 improves affordability.

- Early planning prevents financial strain on families—especially for those with a family history of chronic conditions like Alzheimer’s or stroke.

- Coverage includes in-home care, private facility support, and daily living assistance, but excludes pre-existing conditions, elective treatments, and temporary care.

- Key features like elimination period, benefit amount, and inflation adjustment play a critical role in customizing the right policy for long-term protection.

- Canadian LIC integrates Long Term Care Insurance into full retirement strategies, ensuring that clients protect not just their savings but also their independence.

- Personalized guidance is critical, and Canadian LIC works hands-on with clients to review medical, financial, and family details to recommend the right provider and product.

- Acting before a health crisis hits allows access to better options, lower premiums, and long-term peace of mind for both individuals and their loved ones.

Sources and Further Reading

Below are authoritative, up-to-date resources on Long Term Care Insurance in Canada. Each link is directly clickable and leads to the official source for further details on coverage, costs, features, and planning considerations.

- Sun Life Canada: Long Term Care Insurance

A comprehensive overview of what Long Term Care Insurance is, how it works, what it covers, and how it can help protect your financial security as you age.

Read on Sun Life Canada - RBC Insurance: Long Term Care Insurance Advisor Guide (PDF)

Detailed guide on Long Term Care Insurance options, benefit structures, and real cost examples, including how facility care benefits are paid and what triggers eligibility.

Read the RBC Insurance Advisor Guide (PDF) - Ontario Ministry of Health: Long-Term Care Services

Information about public long-term care services in Ontario, eligibility, and what is and isn’t covered by government programs.

Read on Ontario.ca

These resources offer a solid foundation for understanding Long Term Care Insurance in Canada, helping you make informed decisions about your future care and financial planning.

Feedback Questionnaire:

Feedback Questionnaire: Understanding Long Term Care Insurance in Canada

We’re on a mission to help more Canadians make confident, informed decisions about Long Term Care Insurance. Your answers will help us serve you better.

Thank you for taking the time to share your thoughts. At Canadian LIC, we’re here to help you protect your future with clarity, compassion, and proven experience.

– The Canadian LIC Team

IN THIS ARTICLE

- Understanding The Long Term Care Insurance Market In Canada

- What Is Long Term Care Insurance?

- Why Canadians Need Long Term Care Insurance in 2025

- Types of Long Term Care Insurance Options in Canada

- How Much Does Long Term Care Insurance Cost in Canada?

- Real Client Story: Why Planning Early Matters

- What Long Term Care Insurance Covers (and What It Doesn't)

- Who Should Consider Long Term Care Insurance?

- Key Features to Look For When Comparing Plans

- Long Term Care Insurance and Retirement Planning

- The Role of Canadian LIC in Long-Term Care Planning

- Final Word

Sign-in to CanadianLIC

Verify OTP