- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Life Goals Or Loan Security? Deciding Between Term Life And Loan Protection Insurance

By Pushpinder Puri

CEO & Founder

- 10 min read

- August 29th, 2025

SUMMARY

A detailed comparison of a Term Life Insurance Policy and a Loan Protection Insurance Plan in Canada, showing how each option supports families with debt, income replacement, and long-term security. It highlights why many households view a Term Life Insurance Policy as broader protection, while a Loan Protection Insurance Plan focuses narrowly on debt coverage, helping readers match the right plan to their financial goals.

Introduction

Thinking ahead is never an easy task, especially when it involves the idea that you might not be around to help the people who rely on you. It is an awkward reality, but cancer and heart disease don’t care about your bank account, and not counting the financial costs of death or disability can leave a family vulnerable. That is where insurance comes in, providing options to help secure debts and protect loved ones.

A couple of options frequently float to the surface in these discussions: a Term Life Insurance Policy and a Loan Protection Insurance Plan. In the beginning, the two seem similar, since they both offer financial assistance when it’s needed most. But below the surface, they operate in fundamentally different fashions, and these differences can recast the shape of your family’s future.

For Canadians who are considering their options when it comes to the best Life Insurance coverage, the choice isn’t all about the price of premiums. It’s about matching the protection to your life stage, your financial responsibilities, and your long-term goals. Knowing where Term Life Insurance excels and where Loan Protection Insurance fits in can help you make a decision that not only makes sense but also feels good.

So let’s unpack it together.

Understand Term Life Insurance

A Term Life Insurance Policy is straightforward. You choose a coverage amount. You choose how long you want the coverage to last. If something happens during that period, your beneficiaries receive the payout. They can use it however they want. Pay off debts. Cover living expenses. Fund education. Or keep savings intact.

The key here is flexibility. The payout is not tied to one purpose. It is not locked to a single loan or expense. Instead, it goes where your family needs it most. That makes it one of the best Life Insurance Policies in Canada for people with wide-ranging goals.

Another big advantage is cost. Term Life Insurance rates are usually much lower than those of permanent policies. And with tools now available, you can even get a Term Life Insurance Quotes Online in minutes. It means planning can start fast, without overwhelming paperwork.

Clients often tell us they like the control. They like knowing that if their circumstances change, the payout can adapt. A Long Term Life Insurance Plan for seniors works in the same spirit but tailored to later stages of life, ensuring coverage when health risks grow higher.

Understand Loan Protection Insurance

Now, let’s look at Loan Protection Insurance. This one is more specific. It is tied to a loan. A mortgage, a car loan, a line of credit. If something happens to you, the policy pays off that loan. That is it.

It is narrow but very targeted. For people who worry most about their mortgage, this can feel like peace of mind. The lender is guaranteed repayment. Your family does not inherit that debt.

But here is the catch. The payout does not go to your family. It goes to the lender. And it only covers that specific loan. If you also have other debts or future expenses, your family still has to manage those on their own.

Loan protection can also be more expensive compared to Term Life Insurance. You may pay more for less coverage. Unlike with a Whole Life Insurance Policy, you do not get long-term growth or flexibility.

Comparing Both Options

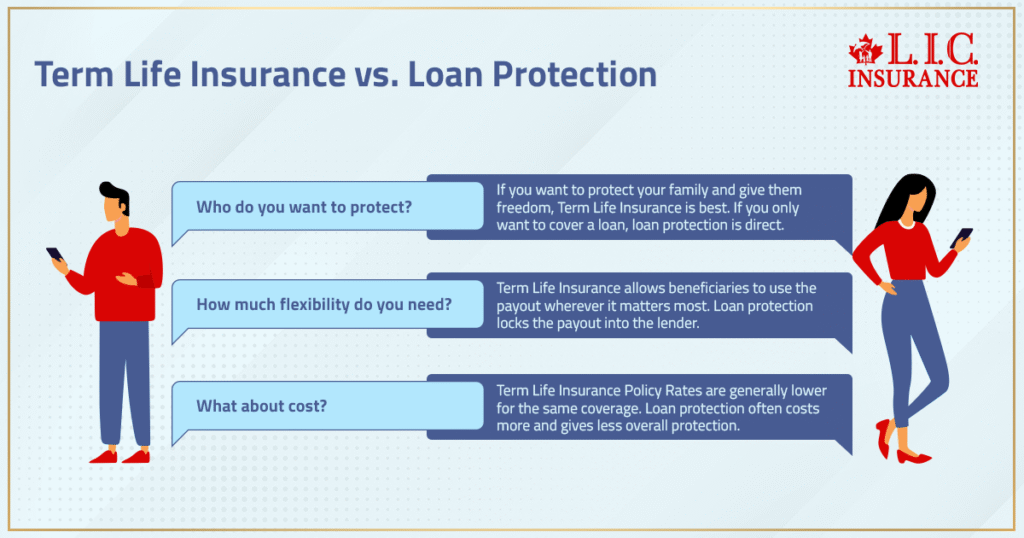

When we sit with clients, we break it down into three questions:

- Who do you want to protect?

- If your main goal is protecting your family and giving them freedom to decide, a Term Life Insurance Plan usually works best.

- If your only focus is making sure one loan is paid, loan protection covers that need directly.

- How much flexibility do you need?

- Term Life Insurance allows beneficiaries to use the payout wherever it matters most.

- Loan protection locks the payout into one path: the lender.

- What about cost?

- Term Life Insurance Policy Rates are generally lower for the same coverage.

- Loan protection often costs more and gives less overall protection.

We often find families leaning toward term coverage because of its reach. It does not just solve one problem. It builds a shield for many problems.

Why Term Life Insurance Aligns With Life Goals

Think about life goals: sending kids to university, leaving behind savings, and protecting your spouse’s retirement. A Term Life Insurance Policy aligns with all of these because it adapts. It fits the bigger picture.

For example, a family may have a $400,000 mortgage, a car loan, and two kids in school. If they only take a loan protection on the mortgage, the payout clears the house debt. But the family is left with no extra help for education or daily living. With a Million Dollar Term Life Insurance Plan, however, the mortgage, the car loan, and future school fees can all be handled. That flexibility is why many Canadians call it the best Life Insurance policy in Canada for young families.

Where Loan Protection Insurance Makes Sense

That does not mean loan protection is always wrong. Some clients like the simplicity. No calculations. No decision-making. They want a guarantee that if they pass away, the mortgage is gone. End of story.

For seniors who are debt-heavy but without dependents, this can be practical. If you are older, you may also look at a Long Term Life Insurance Plan for seniors. Or, if estate planning is not a priority and debt is the only worry, loan protection can provide comfort.

It is not always about what is mathematically better. Sometimes it is about what lets you sleep at night.

Costs Of Coverage

One of the main concerns is cost. A Whole Life Insurance Policy can be expensive, but it builds value over time. A Term Life Insurance Policy is cheaper, but only lasts for a set period. A loan protection plan, on the other hand, is often priced higher relative to its narrow scope.

When you compare the numbers, many families realize they can buy more protection for less cost with term coverage. For example, a 35-year-old can secure a Million Dollar Life Insurance Quote Online for less than the cost of many mortgage protection plans.

We have guided families who saved thousands over the years simply by choosing term coverage instead of loan protection sold by lenders. The difference adds up quickly.

Real-World Scenario

Picture this. A young couple with two children. They have a $500,000 mortgage, a $30,000 car loan, and regular living expenses.

Option one: loan protection on the mortgage. If something happens, the mortgage is cleared. But the car loan remains. Living costs remain. Education costs remain.

Option two: a Term Life Insurance Policy for $1 million. If something happens, the family receives the payout directly. They can clear the mortgage, pay the car loan, and still have money left to manage life and education.

The second option clearly supports life goals more broadly. That is why many advisors recommend it over lender-driven coverage.

Making The Right Choice

The decision comes down to clarity about what matters most. If your focus is family security, flexibility, and cost-effectiveness, a Term Life Insurance Policy usually stands out. If your only concern is a specific loan, then loan protection might work.

We remind clients every day: you do not have to make this choice alone. Comparing options, getting a Life Insurance Quote Online, and understanding how coverage fits your financial plan are all part of smart decision-making.

The Growing Role Of Seniors

One area we see rising is insurance for seniors. With longer lifespans, many are considering coverage not just for debts, but for leaving behind support. A Life Insurance Plan for seniors or a Long Term Life Insurance Plan for seniors can be tailored to these needs.

Even later in life, a policy can help cover final expenses, estate taxes, or small debts. The focus shifts from protecting dependents to ensuring dignity and financial order.

Term Life Insurance Plan vs Loan Protection Insurance Plan

| Feature | Term Life Insurance Policy | Loan Protection Insurance Plan |

|---|---|---|

| Coverage Purpose | Provides broad financial protection for your family, covering debts, income replacement, education, and future goals. | Covers only the specific loan it is tied to (e.g., mortgage, car loan, personal loan). |

| Beneficiary | You choose your beneficiaries (family members, dependents, or anyone you want). | The lender is usually the direct beneficiary to repay the loan. |

| Flexibility | Flexible coverage amount and term length based on your needs and financial goals. | Limited to the balance of the loan and decreases as the loan is paid down. |

| Control of Payout | Lump-sum payment goes directly to your chosen beneficiary, who decides how to use it. | Payout goes directly to the lender to clear the outstanding loan balance. |

| Value Beyond Debt | Protects family lifestyle, replaces income, and secures long-term financial plans. | Protects only the loan, offering no additional financial security beyond that. |

| Cost Efficiency | Often, it is more cost-effective for the coverage provided, especially for healthy individuals. | Premiums may be higher compared to the shrinking benefit over time. |

| Portability | Remains in place even if you refinance, switch banks, or take new loans. | Ends when the specific loan is repaid, refinanced, or transferred. |

| Customizability | Options to add riders (critical illness, disability, etc.) for more complete coverage. | Typically, no customization—coverage terms are tied strictly to the loan. |

Final Thoughts

Life goals and loan security do not always overlap. A Term Life Insurance Policy gives your family a choice. A loan protection plan gives your lender security. Both have their place. But if you want broad protection, flexibility, and value, Term Life Insurance continues to rank as one of the best Life Insurance policies in Canada.

We believe decisions should never be rushed. Look at your debts. Look at your goals. Look at your family’s needs. Then compare coverage. Whether you choose a Term Life Insurance Policy or loan protection, the real goal is the same: protecting the people you care about most.

More on Loan Protection Insurance and Term Life Insurance

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Loan Protection Insurance is designed to cover the loan so you’re not on the hook in the event of the unexpected, such as death or job loss. Term life provides broader Life Insurance protection for your dependent(s) and a more substantial death benefit than a duty-based financial obligation.

Select Term Life Insurance in Canada may ask for a medical exam to verify your health status before approval. A lot of times, it doesn’t have to go through this process with Loan Protection Insurance – and can be underwritten and issued more quickly. Loan Protection Insurance tends to have simpler approval with less scrutiny. Loan Protection Insurance benefits have a shorter waiting time than many traditional life policies.

Yes, both of them can be found online, but they help you with different financial objectives. An online Loan Protection Insurance quote is geared toward your mortgage or other debts you have. An online Term Life Insurance Quote saves money and provides broader financial security for keeping family needs and loan payments in balance.

With Term Life Insurance, Life Insurance premiums are determined by age, health level, and term years and lock in rates for a specified amount of time. Premiums for Loan Protection Insurance are typically linked directly to your loan balance. That makes it workable if your chief concern is paying off loans, but it is less flexible as life goals expand.

With Whole Life Insurance Policies, on the other hand, there exists an investment element of the policy, and long-term financial protection can be built tax-deferred. Loan Protection Insurance does not have a savings, accumulation or cash value feature and therefore may have no value for the surrender or maturity. If you desire both lifelong coverage and a financial investment tool, Whole Life Insurance is a stronger choice.

Key Takeaways

- A Term Life Insurance Policy gives your family broad protection, ensuring debts, living costs, and long-term goals are covered beyond a single loan.

- A Loan Protection Insurance Plan is tied only to one debt, such as a mortgage, and pays the lender directly rather than giving your family financial flexibility.

- Seniors and families often benefit more from Life Insurance policies in Canada that adapt to changing needs, rather than narrow, single-purpose coverage.

- Comparing options like a Life Insurance plan for seniors or a Long Term Life Insurance Plan for seniors with loan protection helps you choose what truly secures your future.

- Looking at Whole Life Insurance Policy rates alongside term coverage shows whether permanent protection or affordable temporary coverage fits your financial picture.

Sources and Further Reading

- Government of Canada – Life Insurance

https://www.canada.ca/en/financial-consumer-agency/services/insurance/life-insurance.html

(Covers key facts about Life Insurance policies in Canada, types of coverage, and consumer protections.) - Insurance Bureau of Canada (IBC) – Life, Health & Disability Insurance

https://www.ibc.ca/on/insurance-101/life-health-disability

(Provides a consumer-friendly breakdown of life, health, and disability insurance and why coverage matters.) - Canadian Life and Health Insurance Association (CLHIA)

https://www.clhia.ca

(National trade association offering insights on Life Insurance in Canada, market data, and consumer resources.) - Investopedia – Term Life Insurance vs. Mortgage Life Insurance

https://www.investopedia.com/ (search: Term Life Insurance vs. mortgage Life Insurance)

(Explains the differences between term life policies and loan/mortgage protection insurance in plain language.) - Financial Consumer Agency of Canada – Credit and Loan Insurance

https://www.canada.ca/en/financial-consumer-agency/services/insurance/credit-loan.html

(Details about Loan Protection Insurance, what it covers, and what limitations to look out for before buying.)

Feedback Questionnaire:

IN THIS ARTICLE

- Life Goals Or Loan Security? Deciding Between Term Life And Loan Protection Insurance

- Understand Term Life Insurance

- Understand Loan Protection Insurance

- Comparing Both Options

- Why Term Life Insurance Aligns With Life Goals

- Where Loan Protection Insurance Makes Sense

- Costs Of Coverage

- Real-World Scenario

- Making The Right Choice

- The Growing Role Of Seniors

- Final Thoughts

Sign-in to CanadianLIC

Verify OTP