- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

TFSA Rules For Spouses In Canada (2025): Who Can Contribute And How

By Harpreet Puri

CEO & Founder

- 13 min read

- August 14th, 2025

SUMMARY

Learn how TFSA contribution rules apply to spouses in 2025, clarifying how the tax-free savings account system works for couples. It highlights individual contribution limits, spousal gifting strategies, and common mistakes that lead to overcontributions. It also covers how to compare the best TFSAs in Canada and how to request a tailored tax-free savings account quote that fits both short- and long-term goals.

Introduction

We’ve discussed how TFSAs are a game-changer for Canadian couples, and we have seen the power of TFSAs in action. Yet every year in Canada, we continue to come across spouses who inadvertently over-contribute to their TFSA and either face fines for the privilege of having done so or are effectively unable to enjoy all that is available to them fully.

This blog isn’t about fluff. It’s about clarity. Be married, not be cohabitating or just thinking about it — in the 2025 edition of exactly how your TFSA works for couples: who can contribute what to a TFSA, why you should care about the contribution limit on your household, and also how spousal support could fit without giving rise to tax complications.

Let’s take a look at exactly what thousands of Canadian couples are missing out on with the tax-free savings Canada account system, and how to get it right this time.

Understanding What A TFSA Is And What It’s Not

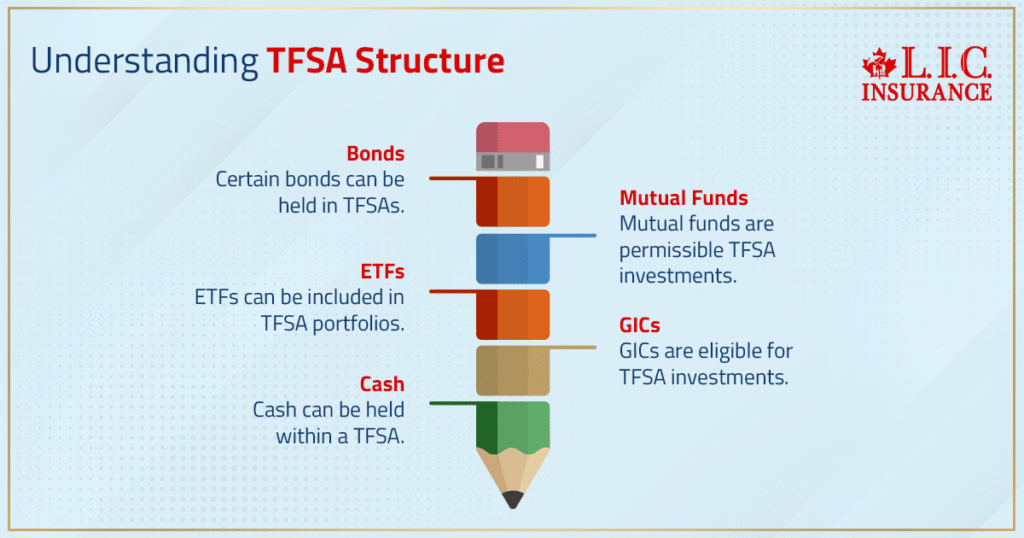

The TFSA isn’t just a savings account—it’s a powerful tax-sheltered investment tool. You can hold cash, GICs, ETFs, mutual funds, and even certain bonds within it.

But there’s one detail that every couple must understand: TFSAs are individual accounts. Unlike RRSPs) Registered Retirement Savings Plans (RRSPs), you cannot open a “joint TFSA” with your spouse or partner. Each person has their own account, their own room, and their own set of contribution rules.

We often hear things like:

- “Can I contribute to my wife’s TFSA if she’s not working?”

- “Can I open a TFSA in my husband’s name?”

- “Can we split one TFSA and share the interest?”

These are smart questions—and they stem from love and support. But unless you follow the correct spousal TFSA rules, your good intentions could lead to unexpected tax headaches.

Who Can Contribute To A Spouse’s TFSA?

Let’s say your partner earns less or chooses to stay home to care for the kids. You want to help them grow their financial security. Great! But here’s what the Canada Revenue Agency (CRA) allows—and doesn’t.

- Yes, you can give money to your spouse so they can contribute to their own TFSA.

- No, you cannot contribute directly to their TFSA yourself.

Why does this matter?

Unlike RRSPs, TFSAs don’t have spousal accounts or income-splitting options built into the structure. You’re allowed to gift funds with no attribution rules, meaning the interest or gains your spouse earns on those gifted TFSA funds won’t be taxed back to you. That’s powerful.

We guide couples through this strategy all the time. It’s legal. It’s smart. And it works beautifully—when you know the rules.

TFSA Contributions Limit In 2025: Get TFSA Contribution Room Information

A new Tax Free Savings Account TFSA contribution limit is issued to every Canadian adult once a year. Remaining for 2025, there is still a limit of $7,000; therefore, any unused room going back to 2009, when you were 18+ and a resident in Canada, continues to accumulate.

Two separate rooms for partners. That means a household could combine to shelter up to $14,000 annually, on top of all unused room rolled over.

CAUTION: You cannot donate your unutilized TFSA room to your spouse, but that is a whole other kettle of fish. The per-person limit is connected to your SIN and is unique for each person at CRA.

For example, if you give your spouse $10,000 as a gift to put in their TFSA but they only have $5,000 of contribution room left, there will be an overcontribution penalty of 1% a month on the excess.

This is why we always recommend that clients ensure partner capacity before gifting large amounts. A single honest mistake is all it takes to generate months (or even years) worth of compounding penalties.

What Happens If You Contribute Too Much?

TFSA overcontribution is one of the most common TFSA issues we see here, and it’s mostly couples trying to help each other out!

What if you both forget that your partner already contributed in the year? You shot them $5,000 more if there was even any space left on their hands. The result is they are now $5000 over in their TFSA contributions.

CRA doesn’t send a warning. They begin silently to take 1% per month, a tax on the portion over that.

That’s $600 per year. Just gone.

How about in a few years, if you’ve left it alone? The thousands, as in we’ve seen it happen. All because a couple wanted to hold hands and rally for each other, but did not know how the CRA likes to handle their overcontributions.

Which is why we make sure the couple verify the room every single time before each transfer. It’s not about paranoia. This is all about saving every hard-earned dollar you worked for.

How Couples Can Maximize Their TFSA Strategy Together

Here’s the good news: Even though TFSAs are individual accounts, couples can use them together strategically.

We’ve helped spouses create plans that:

- Use the higher-income partner’s funds to gift contributions to the lower-income spouse

- Invest in different TFSA portfolios based on each spouse’s risk tolerance

- Plan for future tax-free withdrawals for education, home renovations, or travel

- Diversify investments between fixed-income and equity to balance risk

- Use the TFSA as a retirement income stream that won’t affect OAS/GIS eligibility

Done right, two TFSAs can become a tax-free wealth engine for your household.

But done carelessly, they can become a source of confusion, tax notices, or missed opportunities.

That’s why we’re here.

Choosing The Best TFSAs In Canada: It’s Not One-Size-Fits-All

Every bank and financial institution markets its TFSA as “the best.” But what we’ve found is that the best TFSAs in Canada look different for every household.

Some couples prefer:

- High-interest TFSAs for liquidity and emergency funds

- Self-directed TFSAs to invest in stocks, ETFs, and bonds

- Managed portfolios where a team handles the asset mix

- GIC-based TFSAs for security in volatile markets

There is no universal best TFSA. There’s only the one that fits your goals, risk comfort, and cash flow needs.

And if you and your spouse aren’t aligned on that? We’ll sit down with both of you—virtually or in person—and tailor a solution that works for your shared future.

Spousal TFSA Withdrawals: Can You Take Out Money For Your Partner?

A common scenario is that life happens — perhaps a spouse needs funds for unexpected medical expenses, car repair, or temporary job loss. Then have the other one pull out of their TFSA and give them the money?

Absolutely. Funds in a TFSA are no longer subject to CRA contribution rules ONCE they have been withdrawn. No strings attached — give them away, use them to spend, or reinvest in your product.

However, be aware that you can not add $10 000 to your account before the next year’s reset calendar (if you take this example).

We advise couples, time and again, not to use the TFSA like a checking account. It is a powerful tool — but only when it is used with intention.

How To Get A Tax-Free Savings Account Quote That Actually Fits You

If you’ve ever searched for a Tax-Free Savings Account Quote, you’ve probably seen endless rate comparisons and confusing fine print. But here’s what we do differently.

We ask the right questions:

- What’s your financial goal for this TFSA?

- Are you saving for short-term access or long-term growth?

- What’s your risk tolerance?

- Do you and your spouse need different investment strategies?

- Will either of you withdraw soon, or is this a 10-year play?

Once we have that picture, we match you with real investment products—not just interest rates on a landing page.

It’s personalized. It’s strategic. And it’s focused on your real life, not just the theoretical maximums.

Why Couples Should Review Their TFSA Strategy Every Year

Every January, the TFSA contribution room increases. And every January, thousands of Canadians either forget to contribute or unknowingly overcontribute.

We offer annual TFSA check-ins for all our clients. We look at:

- New contribution room

- Your current balance and growth

- Market trends affecting your portfolio

- Your spouse’s account status

- Your household’s upcoming financial goals

It’s like a financial health check-up—built specifically around your TFSA strategy.

And yes, we even remind you if you’ve forgotten something. Because couples who plan together grow together.

Final Thoughts: TFSAs Are Simple—Until They’re Not

When used properly, TFSAs are one of the most powerful tax-free tools in Canada. But for couples, especially those juggling careers, kids, and competing goals, it’s easy to get confused.

- Contribution limits aren’t shared.

- Overcontributions lead to penalties.

- Spousal gifts are allowed—but must be tracked.

- Withdrawals reset the room next year—not immediately.

- Every investment choice matters.

So if you and your spouse want to maximize your TFSA strategy in 2025, don’t leave it to guesswork or generic advice.

Let us help you understand your options, stay compliant, and build a tax-free savings plan that truly reflects your shared future.

We’re here. We’ve got experience. And we’re ready to guide you—together.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

No, transfers between TFSAs held by different individuals—including spouses—cannot be done directly without triggering a sale. The investments must be sold in one account and contributed as cash into the other spouse’s TFSA, assuming they have available room.

No, marriage or common-law status has no impact on individual TFSA contribution limits. Each spouse continues to receive their own annual limit, and CRA tracks it separately under their individual SIN.

No penalty applies if both spouses use shared logins for convenience, but it’s critical to remember that each TFSA account remains tied to the individual. Misusing funds or assuming shared ownership could lead to tax confusion.

Yes, spouses can be named as TFSA beneficiaries or successor holders directly through the account provider. Doing this avoids probate and ensures the surviving spouse can continue holding the account tax-free if structured correctly.

Not at all. TFSA eligibility depends on age (18 or older) and Canadian residency status—not income. Even spouses with no employment or taxable income can open and contribute to a TFSA within their annual limit.

Key Takeaways

- TFSAs Are Always Individual Accounts

Spouses cannot open joint TFSAs, but each partner is entitled to their own annual contribution limit tracked under their SIN. - Spousal Gifting Is Allowed—But With Care

One spouse can gift money to the other to contribute to their TFSA without triggering attribution rules, making it a smart long-term savings strategy. - Contribution Limits Are Separate And Must Be Tracked Individually

Overcontributing—even through a gift—can result in CRA penalties. Always verify each partner’s TFSA contribution room before transferring funds. - Successor Holder Designation Can Preserve Tax-Free Status After Death

Naming a spouse as a successor holder (not just a beneficiary) ensures the TFSA continues to grow tax-free even after the original holder passes away. - Income Doesn’t Affect TFSA Eligibility

Even if one spouse has little or no income, they can still open and contribute to a TFSA as long as they are 18+ and a Canadian resident. - Comparing The Best TFSAs In Canada Matters

Interest rates, fees, and investment options vary widely across institutions. A personalized tax-free savings account quote helps choose the best fit for each spouse’s financial goals.

Sources and Further Reading

- Government of Canada – Tax-Free Savings Account (TFSA) Overview

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account.html

Official CRA page detailing TFSA eligibility, contribution room, and tax treatment. - Canada Revenue Agency – TFSA Contribution Room Calculator

https://www.canada.ca/en/revenue-agency/services/e-services/e-services-individuals/account-individuals.html

Use “My Account” to view personal TFSA limits and manage contributions. - Financial Consumer Agency of Canada (FCAC) – TFSAs Explained

https://www.canada.ca/en/financial-consumer-agency/services/investing/tax-free-savings-accounts.html

Straightforward breakdown of TFSA types, features, and comparisons to RRSPs. - MoneySense – TFSA Tips for Couples

https://www.moneysense.ca/save/investing/tfsa/tfsa-strategies-for-couples/

Insightful article on how couples can maximize their combined TFSA benefits. - Wealthsimple – TFSA Basics and Common Mistakes

https://www.wealthsimple.com/en-ca/learn/tfsa

Educational guide on how TFSAs work and how to avoid common contribution errors.

Feedback Questionnaire:

We’re conducting a short survey to better understand the questions and concerns Canadians have about Tax-Free Savings Account (TFSA) rules for spouses in 2025. Your responses will help us offer clearer guidance and better financial tools for families. This should take less than 2 minutes.

Thank you for helping us support more Canadian families in navigating TFSA rules effectively.

Your privacy is protected — your contact details will never be shared without your permission.

IN THIS ARTICLE

- TFSA Rules For Spouses In Canada (2025): Who Can Contribute And How

- Understanding What A TFSA Is And What It’s Not

- Who Can Contribute To A Spouse’s TFSA?

- TFSA Contributions Limit In 2025: Get TFSA Contribution Room Information

- What Happens If You Contribute Too Much?

- How Couples Can Maximize Their TFSA Strategy Together

- Choosing The Best TFSAs In Canada: It’s Not One-Size-Fits-All

- Spousal TFSA Withdrawals: Can You Take Out Money For Your Partner?

- How To Get A Tax-Free Savings Account Quote That Actually Fits You

- Why Couples Should Review Their TFSA Strategy Every Year

- Final Thoughts: TFSAs Are Simple—Until They’re Not

Sign-in to CanadianLIC

Verify OTP