- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

TFSA Contribution Limits & Withdrawal Rules In Canada 2025: What You Need To Know

By Pushpinder Puri

CEO & Founder

- 10 min read

- November 17th, 2025

SUMMARY

The 2025 TFSA contribution limit is set at $7,000, raising the total available Canadian Tax Free Savings Account room to $102,000. The content explains how TFSA withdrawal rules allow money to be accessed without income tax, the impact on government benefits, and how unused TFSA contribution room grows over future years. It also highlights investment options such as mutual funds, GICs, and ETFs, and compares TFSA vs RRSP for flexible savings.

Introduction

Canadians eagerly await the annual update and release of new Tax Free Savings Account (TFSA) contribution figures by the federal government each year. The TFSA limit for 2025 is $7,000, and the total cumulative room available to those who have been eligible to this point since its introduction in 2009 is $102,000. The Tax Free Savings Account (TFSA) is generally considered one of the more flexible and tax-efficient savings options available to Canadians who want to grow investments and save for the future.

We’ve witnessed how customers are employing the TFSA not just for short-term savings goals but also for long-term purposes — retirement, tax planning and even estate planning. With proper guidance, your Canadian Tax Free Savings Account is more than just a place to stash cash. It becomes a device for controlled expansion, guarding government benefits and inner peace.

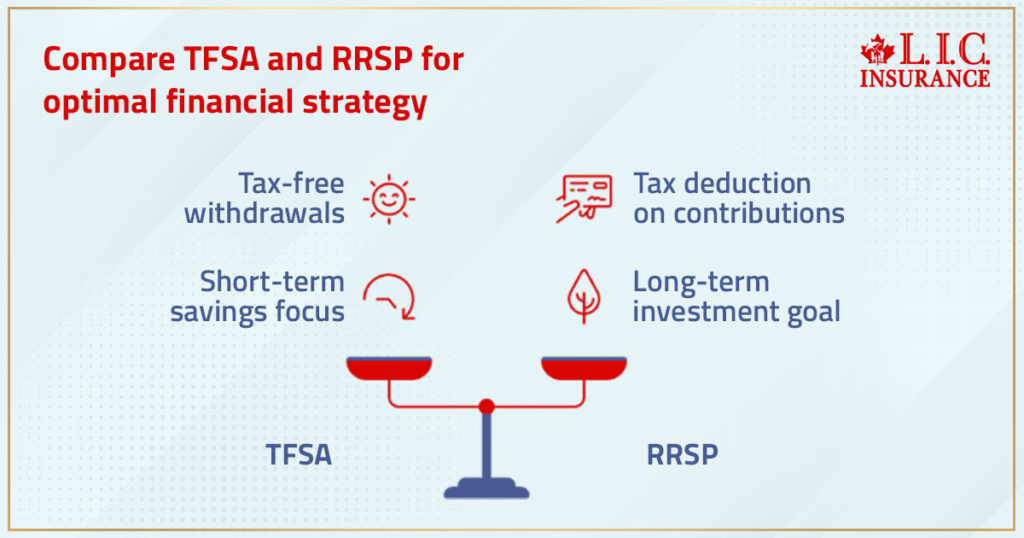

Why A TFSA Is More Than Just A Free Savings Account

When the TFSA was launched in 2009, it was marketed as a straightforward means for Canadians to save and invest their money without having to pay tax on any of it. But its significance has grown over time. Today, a free savings account TFSA is not just one of several tax shelters for short-term savings but also a direct competitor to the Registered Retirement Savings Plan (RRSP) for long-term investing.

RRSPs provide a tax deduction on the way in,and TFSAs provide your savings and eventual withdrawal from tax. That is, you pay no income tax on your withdrawals for a big purchase, retirement or emergency. Not surprisingly, young Canadians — particularly first-time investors — are considering the Tax Free Savings Account when discussing which is better: TFSA vs RRSP strategies.

We help clients by considering them as a whole. The optimum mix of your RRSP and TFSA will depend on your income level, family status and your longer-term financial goals.

Understanding TFSA Contribution Room

The backbone of the program is your TFSA contribution room. It represents the maximum amount you can put into your account in a given year. In 2025, the annual TFSA dollar limit is $7,000, but that’s only part of the calculation.

Your total contribution room is made up of:

- The current year’s contribution limit

- Any unused TFSA contribution room from previous years

- The amount of TFSA withdrawals made in the previous year

For example, let’s say you had $5,000 left over in unused contribution room from 2024, and you withdrew $2,000 last year. In 2025, you could contribute:

- $7,000 (this year’s annual TFSA contribution limit)

- $5,000 (unused contribution room)

- $2,000 (withdrawal amount from 2024)

= $14,000 contribution room for 2025

This flexible formula is what makes the TFSA so powerful. Even if you can’t contribute the maximum every year, your contribution room rolls over indefinitely. That’s why many clients come to us to map out their contributions over future years—so they don’t miss opportunities while avoiding mistakes.

Contribution Limit History: From 2009 To 2025

Here’s a look at the history of annual TFSA limits:

| Year | Annual TFSA Contribution Limit | Cumulative Total |

|---|---|---|

| 2009 | $5,000 | $5,000 |

| 2010 | $5,000 | $10,000 |

| 2011 | $5,000 | $15,000 |

| 2012 | $5,000 | $20,000 |

| 2013 | $5,500 | $25,500 |

| 2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016 | $5,500 | $46,500 |

| 2017 | $5,500 | $52,000 |

| 2018 | $5,500 | $57,500 |

| 2019 | $6,000 | $63,500 |

| 2020 | $6,000 | $69,500 |

| 2021 | $6,000 | $75,500 |

| 2022 | $6,000 | $81,500 |

| 2023 | $6,500 | $88,000 |

| 2024 | $7,000 | $95,000 |

| 2025 | $7,000 | $102,000 |

With this history in mind, clients who were Canadian residents and age 18 or older in 2009 now have access to the full maximum TFSA dollar limit of $102,000.

How To Contribute To Your TFSA

You can contribute to your TFSA in cash or through transfers from a financial institution. We recommend clients double-check their Canada Revenue Agency CRA online account to confirm contribution room before depositing funds.

Eligibility requirements are simple:

- You must be a resident of Canada

- You need a valid social insurance number (SIN)

- You must be at least 18 (or 19 in certain provinces)

Remember: even if you don’t open an account, your TFSA contribution room grows every year you’re eligible. That means opening late doesn’t mean you’ve missed out completely—you can still catch up with unused contribution room.

What Happens If You Over-Contribute?

This is one of the biggest mistakes we see. Some clients overly contribute in their rush to grow wealth, more than the terms of the plan will allow for. The highest amount you are considered to have overcontributed is the most excess in your TFSA on any day during the month (e.g., the peak offending balance determined by time weighted average), and the CRA applies a 1% penalty per month based on that amount.

For instance, let’s say you inadvertently overcontribute $2,000 in January and don’t correct the error until April; you’d owe 1% of $2,000 each month (a total of $60 in penalties). One that you don’t want to see yourself lose.

We help our clients to keep excellent records of their TFSA transactions, helping them avoid any unintentional penalties and remain within their published permitted contributions for TFSAs.

TFSA Withdrawal Rules: How And When You Can Withdraw Money

The beauty of the TFSA lies in its withdrawal rules. Unlike RRSPs, where withdrawals are taxable and reduce your retirement income, TFSAs allow you to withdraw money anytime—without tax consequences.

Key facts:

- Withdrawals don’t count as taxable income

- They don’t affect federal income-tested benefits like Old Age Security (OAS), the Guaranteed Income Supplement (GIS), or the Canada Workers Benefit

- You can re-contribute withdrawn amounts, but only in the following year

Let’s take an example: If you withdraw $5,000 in June 2025, you can only put that $5,000 back starting January 1, 2026, unless you already have spare contribution room. If you re-contribute in the same year without a room, it counts as an excess amount and triggers penalties.

That’s why understanding TFSA withdrawal rules is crucial. We regularly coach clients to plan withdrawals strategically—whether for buying a home, handling emergencies, or supplementing retirement.

Investment Options: From Mutual Funds To ETFs

A TFSA is not just a savings account. It’s a registered plan that can hold a wide range of investments, including:

- Mutual funds

- Exchange-traded funds (ETFs)

- Guaranteed investment certificates (GICs)

- Bonds, stocks, and other qualified products

All growth inside the TFSA—whether capital gains, dividends, or investment income—remains completely tax-free.

The best strategy depends on your goals. Younger clients often choose higher-risk growth products, while retirees may prefer safer investments with stable returns. Our advisors tailor strategies so your TFSA isn’t just sitting idle but working toward your unique objectives.

How The TFSA Protects Government Benefits

Among the advantages offered by the TFSA is that withdrawals are not treated as income for tax purposes. And voilà, it means they won’t be clawing back government benefits like OAS, GIS, EI or CWB. For seniors concerned about clawbacks of old age security or the guaranteed income supplement, the TFSA is a lifebelt.

We’ve known retirees who turned to RRSPs, and it resulted in clawbacks of federal benefits. By moving some of their savings into TFSAs, they could withdraw the money tax-free and keep their benefits.

The Role Of The Canada Revenue Agency CRA

TFSA rules are established and monitored by the Canada Revenue Agency CRA. They keep track of how much you are eligible to contribute, monitor unused contribution room and charge penalties if you over-contribute.

Clients, whose returns have been prepared and filed by mid-April, can log in to their CRA My Account and review their return at the start of the year or any adjustments following e-filing. But the CRA isn’t updated until institutions make their TFSA activity reports, so numbers may not reflect recent contributions.

Our advice is that you keep copies of your own records. This ensures there are no surprises and guards against penalties associated with exempt contributions or non-qualifying investment income.

Management Fees And Hidden Costs

Though TFSAs are very flexible, pay attention to management fees on investments held within them. Mutual funds, ETFs, and even GICs can have fees or commissions that eat into your money’s tax-free growth.

This is where good investment advice comes in. Opting for lower-fee products or understanding the fair market value of assets in your TFSA will ensure that you aren’t giving more to management fees than needed.

Why Canadian LIC Helps Clients Maximize The TFSA

The TFSA is straightforward on the surface, but in practice, mistakes can cost Canadians thousands in penalties, lost growth, or reduced contribution flexibility. We help:

- Calculate the maximum contribution limit for current and future years

- Avoid over-contribution penalties

- Plan withdrawals to maximize tax-free growth and protect federal income-tested benefits

- Tailor investment options—mutual funds, ETFs, or GICs—inside the TFSA for your goals

- Balance your TFSA with RRSPs, RESPs, and other plans

Final Thoughts On TFSA Contribution Limits And Withdrawal Rules In 2025

The 2025 TFSA contribution limit is $7,000, and the cumulative lifetime room since inception sits at $102,000. For Canadians, this is far more than a savings account: It’s how they make educated investment decisions, plan taxes, and protect their wealth.

The trick is using it effectively: respecting contribution room, planning withdrawals under TFSA withdrawal rules and aligning investments with your stage of life. With the right advice, your TFSA is not just a sideline account — it’s one of the pillars of your financial plan.

We’ve shown thousands of families how to build wealth through tax-efficient planning. If you’re getting things started with a bit of change, or more ambitiously directing a large monthly sum to your long-term kitty, the Canadian Tax Free Savings Account can serve you well — provided you know how to use it.

More on TFSA

- A Guide to the Rules of Trading Stocks within Your TFSA: Avoiding Pitfalls and Maximizing Your Benefits

- Why Investors Prefer Tax-Free Savings Accounts To Registered Retirement Savings Plans In Canada

- Can I Get Visitor Insurance with Pre-Existing Conditions?

- Should You Use Your TFSA To Pay For A Super Visa Insurance Plan In Canada?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

A TFSA lets investment income and capital growth build without income tax eating into it. Over time, that tax-free growth creates flexibility for big financial goals. Unlike a registered retirement savings plan, the withdrawals won’t reduce government benefits.

Yes. Mutual funds, ETFs, GICs, and even stocks can all sit inside your free savings account TFSA. The growth on those products—whether dividends, interest, or gains—remains tax-free, giving you more than a simple cash savings tool.

You’re allowed more than one TFSA, but the CRA combines them when calculating your total contribution room. If your deposits across accounts exceed the maximum TFSA contribution limit, the over-contribution penalties apply.

You can withdraw money whenever you need, and the amount adds back to your contribution room in the following year. This means your own TFSA works for both short bursts of saving and longer-term investment advice strategies.

Any unused contribution room carries forward without expiry. This lets Canadians catch up later if money was tight before. It’s why even small deposits now matter—your TFSA contribution room grows regardless of timing.

Yes, fees on mutual funds or ETFs can chip away at your money’s free growth. While the CRA allows investment income to stay tax-free, management fees still impact the fair market value. Choosing lower-cost funds helps keep returns intact.

If you become a non-resident of Canada, you can keep your TFSA open, but you can’t contribute further. Any new deposits would be considered excess amounts and face penalties. The income earned inside still remains tax-free in Canada.

No. TFSA withdrawals don’t show up as taxable income, so they won’t reduce EI or other federal income-tested benefits. That’s one advantage over taxable accounts—TFSA withdrawals count only toward future contribution room.

Exempt contributions are deposits you weren’t eligible to make—like contributing while not a Canadian resident. CRA treats them as an over-contribution, and the highest excess TFSA amount is subject to monthly penalties.

Yes, most financial institutions provide a Tax Free Savings Account Quote online showing current products, interest rates, or the best TFSA rates in Canada. We often compare these for clients alongside RRSPs to tailor the right mix.

Key Takeaways

- The TFSA contribution limit for 2025 is $7,000, bringing the lifetime Canadian Tax Free Savings Account room since 2009 to $102,000.

- Withdrawals under TFSA withdrawal rules stay tax-free and do not reduce federal income-tested government benefits like OAS or GIS.

- Unused TFSA contribution room carries forward indefinitely, letting Canadians catch up in future years.

- A free savings account TFSA can hold investments such as mutual funds, ETFs, GICs, and stocks, all sheltered from income tax.

- Staying under the maximum TFSA contribution limit avoids CRA penalties for over-contributing, which are charged monthly on the excess amount.

- Comparing TFSA vs RRSP shows both have roles; the TFSA offers flexibility while the RRSP focuses on tax-deferred retirement savings.

Sources and Further Reading

- Canada Revenue Agency (CRA): Tax Free Savings Account (TFSA) Program

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account.html - Government of Canada: TFSA Contribution Room and Limits

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account/contribution-room.html - Financial Consumer Agency of Canada: Tax-Free Savings Account Basics

https://www.canada.ca/en/financial-consumer-agency/services/savings-investments/tfsa.html - TD Canada Trust: TFSA Contribution Limits and Rules

https://www.td.com/ca/en/personal-banking/products/investing/tfsa - RBC Royal Bank: TFSA Contribution and Withdrawal Information

https://www.rbcroyalbank.com/investing/tfsa/

Feedback Questionnaire:

We’d love to know how Canadians are experiencing the TFSA in 2025. Your input helps us understand the real struggles and provide better guidance.

IN THIS ARTICLE

- TFSA Contribution Limits & Withdrawal Rules In Canada 2025: What You Need To Know

- Why A TFSA Is More Than Just A Free Savings Account

- Understanding TFSA Contribution Room

- Contribution Limit History: From 2009 To 2025

- How To Contribute To Your TFSA

- What Happens If You Over-Contribute?

- TFSA Withdrawal Rules: How And When You Can Withdraw Money

- Investment Options: From Mutual Funds To ETFs

- How The TFSA Protects Government Benefits

- The Role Of The Canada Revenue Agency CRA

- Management Fees And Hidden Costs

- Why Canadian LIC Helps Clients Maximize The TFSA

- Final Thoughts On TFSA Contribution Limits And Withdrawal Rules In 2025

Sign-in to CanadianLIC

Verify OTP