Common questions

- Life Insurance can protect your family from any financial crisis

- You leave a completely tax-free inheritance to your dear ones or beneficiaries

- Life Insurance can pay for your funeral expenses

- You can clear your debts and loans with Life Insurance

Tax-Free Savings Account

A Tax-Free Savings Account (TFSA) is a plan that allows you to grow your savings without ever paying tax within your account. This is a rare form of traditional savings accounts where you pay tax on the growth earned by your savings.

Annually, residents of Canada who are at least the age of eighteen are allowed to invest up to $6,000 into their Tax-Free Savings Account. When you deposit into a Tax-Free Savings Account, it is made with after-tax dollars, ensuring that withdrawals that are tax-free can be made at any time. The contribution room is regained once you make the withdrawal.

Your Notice of Assessment (NOA) will tell you if you have any unused contribution room from previous years. The TFSA limit is set by Canada Revenue Agency (CRA) is currently $6,000. The Canada Revenue Agency will charge contributions exceeding the maximum amount a monthly penalty of 1%.

Notable features of Tax-Free Savings Account

- Investment options include a complete range of guaranteed interest options and funds.

- By designating a beneficiary, there is potential for creditor protection and avoiding probate.

- Growth on your savings in tax-free and withdrawals.

- Unused contribution room carried forward to the following year.

- Contribution room can be regained the year following a withdrawal

- Withdrawals do not hamper government benefits such as OAS, GIS, GST credit, etc.

Who should have a Tax-Free Savings Account?

With so much versatility, the Tax-Free Savings Account is an ideal investment option that can benefit most Canadian residents. At any given time, you can obtain your savings without ever paying tax on the growth, making it suitable for any short-term savings goals, including:

- Home renovations

- Buying a vehicle

- Going on a family trip

- Dipping into your emergency savings

A Tax-Free Savings Account is also an excellent option for individuals looking for a different source of income during retirement or for those individuals who expect to be in a higher or equal tax bracket once they retire. Unlike a Retirement Savings Plan, you do not need to convert your Tax-Free Savings Account to an income product at age 71, making it the best option for retired individuals looking for ways to save money on a tax-free basis throughout their retirement. Additionally, income received from a Tax-Free Savings Account does not affect you from receiving Old Age Security (OAS), Guaranteed Income Supplement (GIS), Goods and Services Tax (GST) credit, or other tax credits and income-tested benefits.

×

Life Insurance Quote Form

Choosing the correct type of savings account

“Why should I save money?” There is no simple explanation to that question, to be honest, “why should I save money?” A Retirement Savings Plan (RSP) or a Tax-Free Savings Account (TFSA), which is better? While both these account types are different, each plan offers some essential factors to keep in mind.

| Retirement Savings Plan (RSP) | Tax-Free Savings Account (TFSA) | |

|---|---|---|

| Primary Purpose | Retirement | Investing |

| Annual Contribution Limit | 18% of earned income* | $6,000 annually |

| Unused Contribution Room | Carried forward | Carried forward |

| Taxation on Investment Growth | Growth is tax-free. Tax is only paid when money is withdrawn. | Never required to pay tax on growth. |

| Deductions on Tax | Annual income tax will be reduced with deposits. A refund on tax can be equal to the deposit multiplied by the marginal tax rate. | There is no deduction on tax and contributions are made with after-tax dollars. |

| Withdrawals | Withdrawals do not increase annual contribution room. Withholding tax is charged on the amount withdrawn and the amount reported as taxable income. The income may affect eligibility for government sponsored retirement income programs. | Withdrawals are not taxed and considered “income”. Government sponsored retirement income programs are not affected by the income. They also increase the annual contribution room. |

| Maturity Date | The year when theperson turns 71 | At age 105 |

| Based on the annual contribution limit | ||

| Canada Revenue (CRA) sets the annual limit under specific guidelines. Your Notice of Assessment will inform you if you have contribution room that is unused from previous years. This information does not account for legal, tax or other professional advice. Information is believed to be accurate, butnot guaranteed. | ||

| ® Denotes a trademark of The Equitable Life of Canada Insurance Company. |

* Based on the annual contribution limit ** The annual limit is set under the guidelines of the Canada Revenue Agency (CRA). Your Notice of Assessment (NOA) will let you know if you have any unused contribution room from previous years. This information does not constitute tax, professional, or legal advice. Information is believed to be accurate. However, accuracy is not guaranteed.

Tax-free money exists if you know where to look

With time, money accumulates; it’s not handed to you, despite what advertisements on the television show you. For most individuals, it’s about being committed to investing long-term rather than lottery winnings and windfalls. A ax-Free Savings Account by many can be an investment savings tool that is misunderstood by many. Even though some consider it a short-term investment, most of us do not value this plan’s long-term savings potential. It would leave you surprised knowing that a Tax-Free Savings Account can hold investments like mutual funds, stocks and bonds etc. To find out more details, contact the team at Equitable Life of Canada today.It is a reliable savings tool during your employed years.

Did you know investing in a Tax-Free Savings Account:

- You are not taxed on your investment growth.

- You earn a new contribution room every year if you are eighteen years or older.

- If you have not maxed out your deposits in your previous years, you can make extra deposits.

- Your contribution room is regained in the following years if you do not create a withdrawal.

A Tax-Free Savings Account is an ally during your years of retirement. Many Canadians in their retirement rely on income earned from a Retirement Savings Plan (RSP) or a pension plan. A Tax-Free Savings Account is another source of tax-free income, allowing you to draw income when you require it.

When you use a Tax-Free Savings Account in your retirement, you?

- Are eligible to receive old-age guaranteed income supplement, tax credit, goods and services tax, sales tax, and other income benefits and taxes, regardless of any withdrawals you make from your TFSA.

- Do not need to convert your Tax-Free Savings Account like an income product such as a Retirement Savings Plan (RSP) with age.

- Will not be weighed down with a hefty tax bill on your estate upon your demise.

If you are still unsure about the capability of a Tax-Free Savings Account, you should reconsider. While this example mentioned above may not apply to every individual’s situation, it does show the potential long-term savings plan a TFSA can provide.

Make the money that works for you

Most of us find it a challenge to save money, and the worst part is finding money to save; it is even more difficult. Let’s try to understand that how we can make money that works for us.A great way to save for retirement is to invest in a Retirement Savings Plan (RSP). Every time you make an RSP contribution, you receive a tax refund instantly. Consider using that amount to fund your TFSA instead of spending it. It Is not the first idea that creeps up into the head of many individuals but investing your tax refund helps build your emergency fund to cater to any short-term financial goals you may have.Down the road, a Tax-Free Savings Account is a secondary retirement savings investment. Any withdrawals made from your TFSA will not be reported as income and will not affect your eligibility for specific government benefits such as sales tax, goods and services tax, old age security etc. Let’s consider all the possibilities.

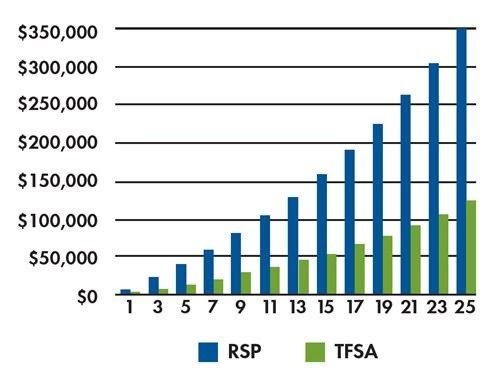

A $7,000.00 Retirement Savings Plan contribution could potentially make a $2,450.00 tax refund. If that refund is invested in a Tax-Free Savings Account, it would be worth $122,778.00 after 25 years. A pretty decent chunk of money you didn’t know you had.

Get the best Insurance Quote from Equitable

Call 1 844-542-4678 to speak to our advisors.