- Understanding How Does a Whole Life Insurance Policy Work: A Comprehensive Guide

- Key Takeaways

- Understanding Whole Life Insurance Policies

- The Cash Value Component: Growth and Access

- Death Benefits and Beneficiaries

- Comparing Whole Life Insurance to Term Life Insurance

- Customizing Your Whole Life Insurance Policy with Riders

- Evaluating Insurers and Policies

- Summary

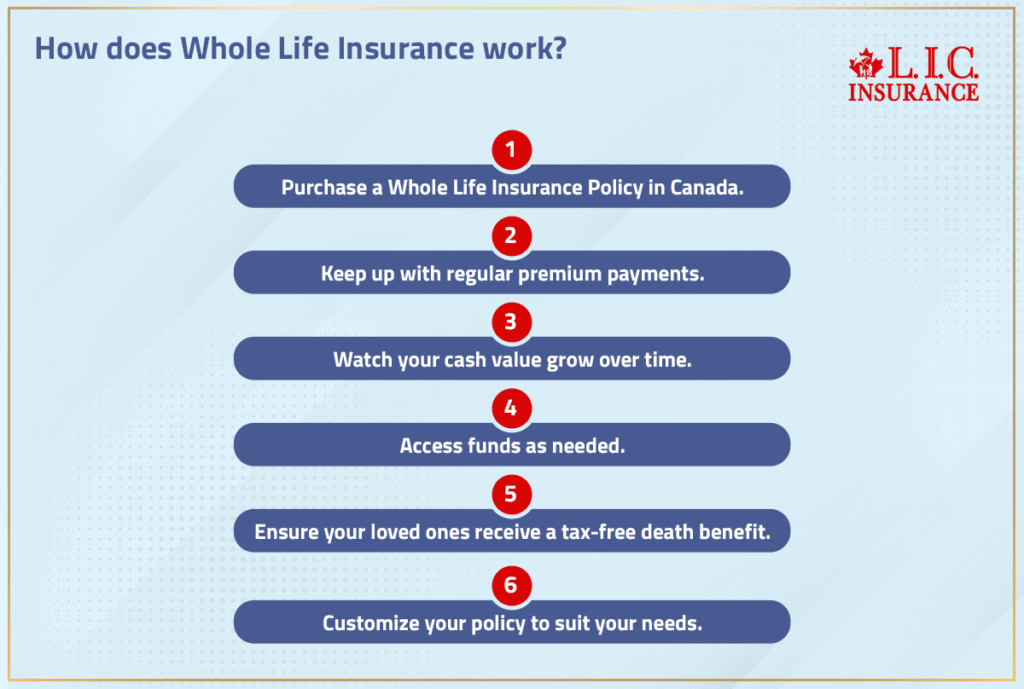

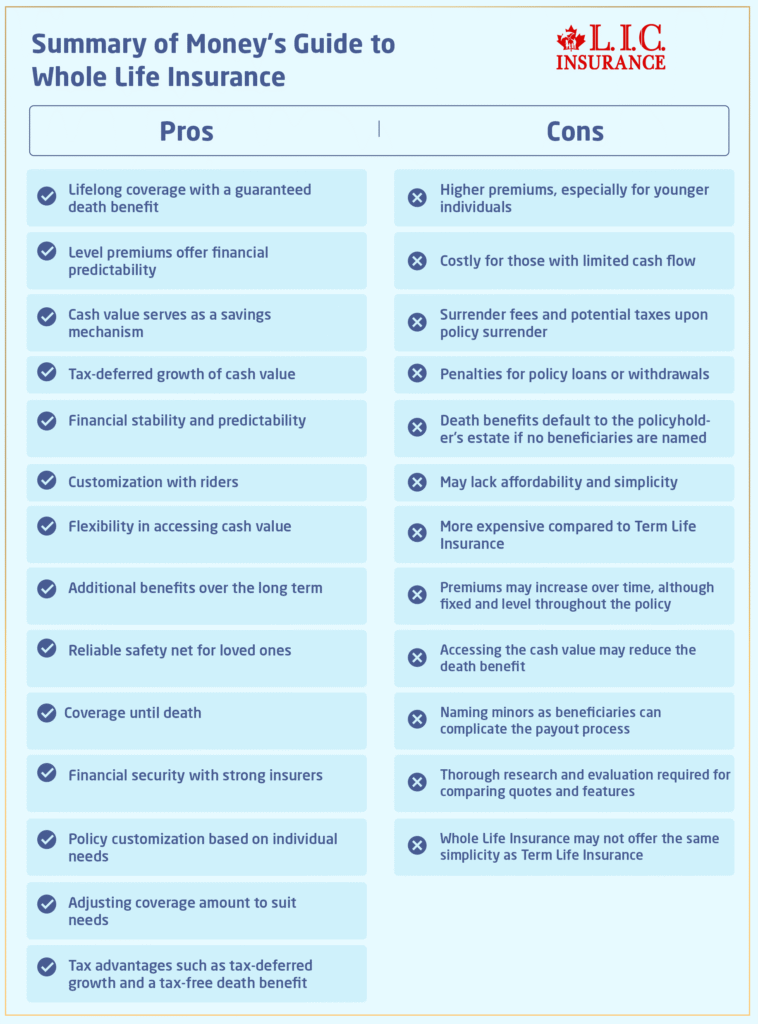

As the name suggests, a Whole Life Insurance Policy is a type of permanent life insurance that provides coverage for the policyholder’s entire life. Unlike Term Life Insurance, which covers a specific period, a permanent life insurance policy like Whole Life Insurance and Universal Life Insurance provides lifelong coverage with guaranteed death benefits and level premiums for the insured’s entire life. This type of policy is often seen as a cornerstone of long-term financial planning, offering a level of stability and predictability that few other financial products can match.

Understanding how life insurance works, especially in the context of a Whole Life Insurance Policy, is quite simple. The policyholder pays regular premiums, which are allocated to cover death benefits, the insurer’s operating costs and profits, and contribute to the policy’s cash value. This cash value is a distinctive feature of Whole Life Insurance, serving as a savings mechanism that grows over time and can be accessed in various ways.

Key Takeaways

- Whole Life Insurance provides lifelong coverage with level premiums and a cash value component, which is different from Term Life Insurance, which only covers a specific period.

- The cash value of Whole Life Insurance grows tax-deferred and can be accessed via loans, withdrawals, or surrender, and its growth and use have several financial implications, including potential taxes on gains.

- Choosing the right whole life policy involves evaluating insurers’ financial strength and policy features, with options to customize coverage through riders and the necessity to select and update beneficiaries carefully.

Understanding Whole Life Insurance Policies

As the name suggests, a Whole Life Insurance Policy is a type of permanent life insurance that provides coverage for the policyholder’s entire life. Unlike Term Life Insurance, which covers a specific period, a permanent life insurance policy like Whole Life Insurance and Universal Life Insurance provides lifelong coverage with guaranteed death benefits and level premiums for the insured’s entire life. This type of policy is often seen as a cornerstone of long-term financial planning, offering a level of stability and predictability that few other financial products can match.

Understanding how life insurance works, especially in the context of a Whole Life Insurance Policy, is quite simple. The policyholder pays regular premiums, which are allocated to cover death benefits, the insurer’s operating costs and profits, and contribute to the policy’s cash value. This cash value is a distinctive feature of Whole Life Insurance, serving as a savings mechanism that grows over time and can be accessed in various ways.

Key Components of a Whole Life Policy

Three fundamental elements form the foundation of a Whole Life Insurance Policy: the guaranteed death benefit, level premiums, and the cash value component. The guaranteed death benefit is a fixed sum of money that is paid out to the beneficiaries upon the death of the policyholder. This benefit is particularly attractive as it provides a reliable safety net for the policyholder’s loved ones.

The second component, level premiums, offers financial predictability. The premiums are calculated based on the insured’s life expectancy and remain consistent throughout the policy’s term. This means that the policyholder pays the same amount each month without increases.

Lastly, a portion of these premium payments contributes to the cash value component, which grows over time and offers an additional layer of financial security.

How Premiums Are Allocated

Whole Life Insurance premiums get distributed between the death benefit and the cash value component., and they remain level for the life of the policy. As the policyholder ages, the cost of insuring their life increases, which influences how premiums are allocated between the cash value and the insurance cost.

Interestingly, once enough cash value has accrued, it can be used to pay the premiums, achieving a ‘paid up’ status. (Note: This depends on the specific policy design and whether dividends or paid-up additions are used.) This unique feature not only enhances the policy’s appeal but also demonstrates the financial flexibility offered by Whole Life Insurance.

The Cash Value Component: Growth and Access

The cash value component plays a vital role in a Whole Life Insurance Policy, which can provide a source of funds that policyholders can access during their lifetime. This feature adds flexibility and additional benefits to the policy. This feature essentially acts as a forced savings account, which grows over time on a tax-deferred basis. The cash value doesn’t accrue immediately upon purchasing the policy. It typically grows slowly in the early years, and the timeline depends on the insurer, fees, and the policy structure. The insurance company invests the cash value, and it grows at a fixed rate set by the insurer, typically ranging from 1% to 3.5%.

(Update for 2026: In Canada, cash value growth is not always a simple fixed rate. Some Whole Life Policies have guaranteed cash value growth, while participating Whole Life Policies may also grow through dividends, which are not guaranteed.)

Policyholders can access the cash value in their Whole Life Insurance Policy in different ways. These include withdrawals, loans, and even surrendering the policy. It’s important to note that these methods of accessing the cash value come with their own implications, which we will discuss in more detail shortly.

Tax-Deferred Growth

The tax-deferred growth of the cash value component of Whole Life Insurance offers several advantages:

- The cash value is not subject to taxes as it increases.

- This tax-deferred growth allows the money in the cash value to compound more quickly because it’s not reduced by taxes each year.

- Faster accumulation of cash value leads to increased financial benefits.

Moreover, dividends paid by the insurance company to the policy’s cash value are generally not taxable. (However, dividends in participating Whole Life Policies are not guaranteed and can change over time.) This tax advantage, combined with the guaranteed minimum rate of return on the cash value and its fixed growth rate, enhances the policy’s stability and predictability for the insured.

Some policies offer guaranteed growth, while others rely partly on dividend performance. Not every Whole Life Policy has a “fixed growth rate.”

Accessing Cash Value: Loans, Withdrawals, and Surrenders

Whole-life insurance policyholders can tap into their policy’s cash value through loans, withdrawals, or a policy surrender. Policy loans offer financial flexibility during emergencies, and the best part is that they do not have tax implications. Policy loans are often tax-free, but tax consequences can apply depending on the policy’s Adjusted Cost Basis (ACB) and how much is borrowed.) However, any outstanding loan balance and interest will reduce the death benefit.

Withdrawals from the cash value of a policy have the following characteristics:

- They are tax-free up to the amount of premiums paid.

- Withdrawals are generally tax-free up to the policy’s Adjusted Cost Basis (ACB), not simply the premiums paid.)

- Excess withdrawals over the premiums paid may be taxable.

- Canada: Amounts above ACB are generally taxable as income.)

- Excess withdrawals could lead to a reduction in the death benefit.

Finally, surrendering the policy allows a policyholder to:

- Access the accumulated cash value

- But at the cost of surrender fees and potential taxes on the gains

- Terminate the policy, which means forfeiting the death benefit.

Death Benefits and Beneficiaries

The death benefit represents a crucial feature of Whole Life Insurance. This is a predetermined sum that the insurance company pays out to the beneficiaries upon the death of the policyholder. It’s important to note that this payout is generally not subject to income tax. The policyholder can distribute the death benefit in varying percentages among multiple beneficiaries.

However, if no beneficiary is named on a Whole Life Insurance Policy, the death benefit defaults to the policyholder’s estate. This could potentially cause delays and extra costs. In certain states, spouses may automatically have rights to a portion of the death benefits, requiring written consent for naming other beneficiaries. In some situations, provincial family law, separation agreements, or court orders may affect beneficiary rights, so beneficiary updates should be handled carefully. Beneficiaries can choose to receive the death benefit as a lump-sum payment, in installments, or converted into an annuity.

Guaranteed Death Benefit

The guaranteed death benefit stands as a key characteristic of a Whole Life Insurance Policy. This is a payout that the insurance company promises to pay to beneficiaries upon the policyholder’s death. To ensure this guaranteed death benefit, policyholders must regularly pay their premiums. The amount of this benefit remains constant throughout the life of the policy and is paid out tax-free to the beneficiaries.

Unlike Term Life Insurance, which only pays a death benefit if the policyholder dies within a specified term, a Whole Life Insurance Policy ensures the death benefit is payable at any time as long as premiums are paid and the policy is in force. This provides a level of certainty and peace of mind that policyholders highly value.

Choosing and Updating Beneficiaries

It’s essential to carefully select and update beneficiaries when managing a Whole Life Insurance Policy. This process requires consideration of who will first receive the death benefit and who should receive it if the primary beneficiary cannot. This typically occurs due to life events such as marriage, divorce, or the birth of children. It’s also worth noting that policyholders can designate a wide range of candidates as beneficiaries, including family members, trusts, estates, charities, or legal entities.

Special considerations must be taken when naming minors as beneficiaries due to complications in the payout process, which can be managed by appointing a guardian or establishing a trust. Beneficiary designations can be revocable, allowing the policyholder to make changes at any time, or irrevocable, which are locked in unless the beneficiary consents to a change.

Beneficiaries may not receive automatic notification of their status and should be informed by the policyholder about the policy’s existence and instructed on how to make a claim in the event of the policyholder’s death.

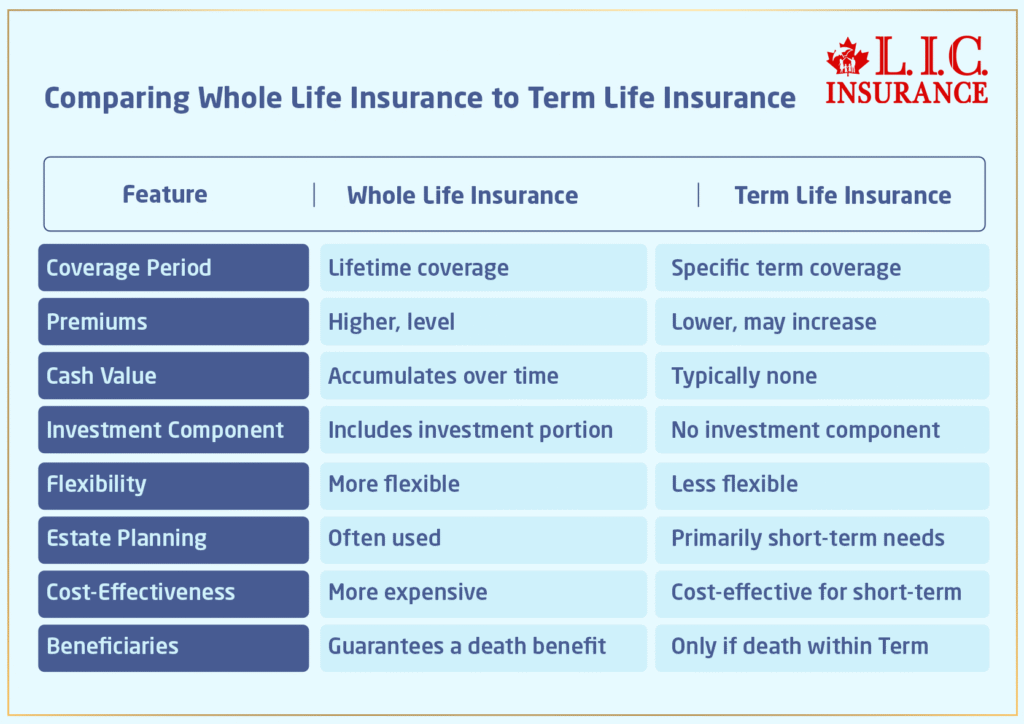

Comparing Whole Life Insurance to Term Life Insurance

But how does Whole Life Insurance stand up against Term Life Insurance? There are some key differences to consider. Term Life Insurance offers coverage for a set duration, like 10, 20, or 30 years, and benefits are only paid if the insured person dies within this term. On the other hand, Whole Life Insurance covers the insured person until death, regardless of when that might be.

Moreover, Whole Life Insurance includes a cash value component, which is absent in Term Life Insurance. This means there is an investment component in Whole Life Insurance that can provide financial benefits over time, whereas Term Life Insurance purely provides a death benefit.

Whole Life Insurance Canada: Quick Answers Before You Choose

If you’re researching canada, you’re likely trying to figure out what is Whole Life Insurance canada and whether it fits your long-term plan. A simple way to explain it is this: Whole Life Policy life insurance provides permanent coverage plus a built-in savings element that can grow over time.

Many people ask how much does life insurance cost before they even look at features. The truth is, pricing varies based on age, health, coverage amount, and whether the policy is participating or non-participating. That’s why comparing quotes matters, especially when weighing term vs Whole Life Insurance canada—term coverage is usually cheaper upfront, while whole life can provide lifelong protection and cash value growth.

One reason people choose whole life is the long-term value. The Whole Life Policy benefits can include stable premiums, lifetime coverage, and access to savings through cash value life insurance canada, which may be used through policy loans or withdrawals depending on the policy structure and tax rules.

Coverage Length and Premiums

In terms of coverage duration, Term Life Insurance provides coverage for a fixed period, such as 10, 20, or 30 years, while Whole Life Insurance provides coverage for the insured’s entire lifespan. This means that Whole Life Insurance can offer coverage that matures at ages like 90, 100, or 120, providing a level of long-term security that Term Life Insurance simply can’t match.

In terms of premiums, Term Life Insurance typically has lower initial premiums compared to Whole Life Insurance. This reflects its coverage for a specific term and the absence of cash value accumulation. However, these premiums can increase during each renewal period.

On the other hand, Whole Life Insurance premiums are higher but fixed and level throughout the life of the policy, offering financial stability and predictability, which is an important factor to consider when evaluating life insurance costs.

Cash Value vs. No Cash Value

Whole Life Insurance and Term Life Insurance differ significantly in terms of the cash value component. This difference is important to consider when choosing the right insurance policy for your needs. In a Whole Life Insurance Policy, a portion of the premiums paid is allocated to cash value, which can grow over time. This cash value component serves as a type of savings account within the policy that the policyholder can access in various ways.

In contrast, Term Life Insurance:

- It does not have a cash value component

- It has no investment component or cash accumulation

- If the policyholder outlives the term of the policy, no benefits are paid out. Therefore, while Term Life Insurance may be cheaper initially, it lacks the cash value component that can provide financial benefits over the long term.

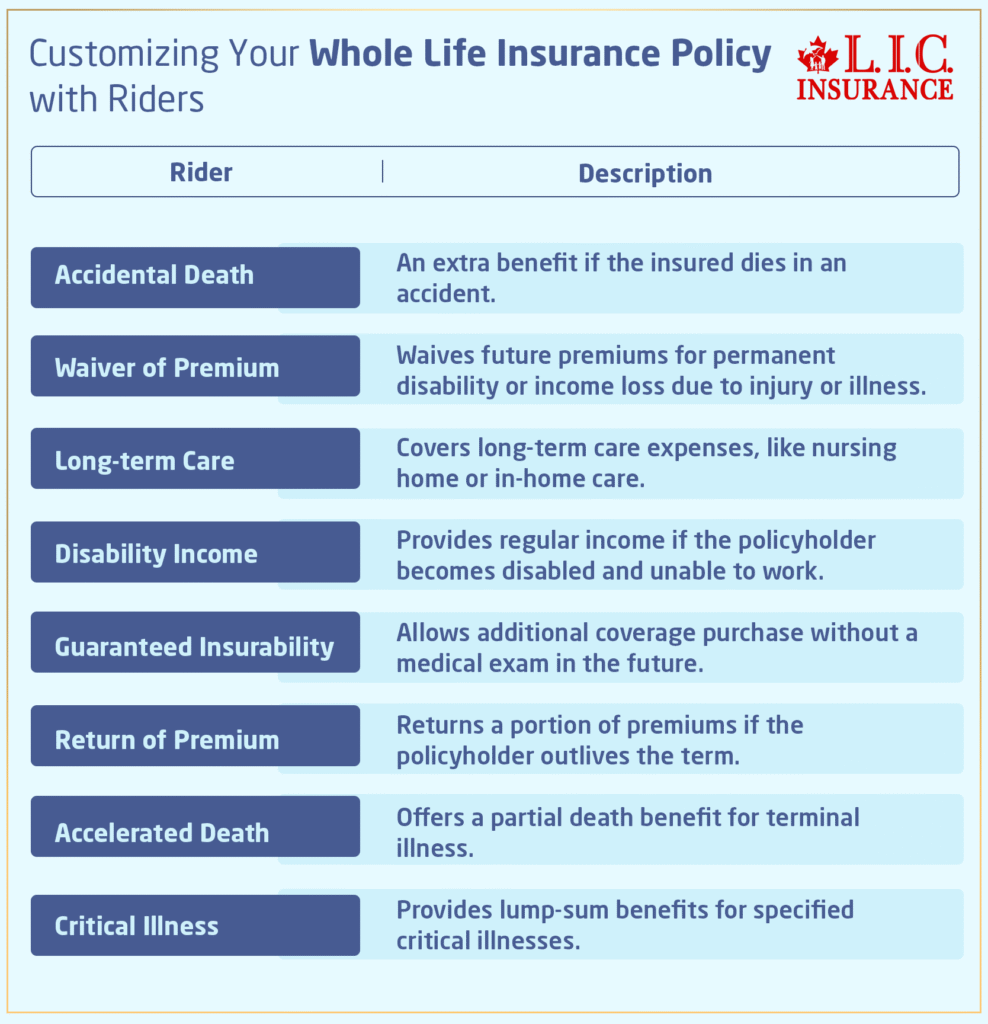

Customizing Your Whole Life Insurance Policy with Riders

Riders introduce a level of adaptability and personalization to Whole Life Insurance policies. Riders are optional provisions that can be added to a policy to enhance its coverage. These riders add specific conditions or benefits to the policy, allowing policyholders to tailor their coverage to their specific needs and circumstances. Some common riders include:

- Accidental death benefit rider

- Waiver of premium rider

- Long-term care rider

- Disability income rider

- Guaranteed insurability rider

By adding these riders to your policy, you can customize your coverage and ensure that it meets your unique needs.

Before purchasing a policy, policyholders should ensure it includes the specific riders they want, as the types and costs of riders vary between insurance companies. Some common riders include options like:

- Return of premium

- Waiver of premium

- Accidental death

- Long-term care

- Critical illness

Common Whole Life Insurance Riders

Policyholders have a range of popular riders to consider while personalizing their Whole Life Insurance Policy. An Accelerated Death Benefit rider allows policyholders with a terminal illness to access part of the death benefit amount while still alive, which can be essential for paying for end-of-life care.

Another popular rider is the Waiver of Premium Rider. This excuses the policyholder from paying future premiums if they become permanently disabled or lose income due to injury or illness before a certain age. Riders like these can add significant value to a policy and provide additional peace of mind for policyholders.

Evaluating Insurers and Policies

In the process of considering a Whole Life Insurance Policy, it’s vital to assess both the insurance companies and the particular policies they propose. A financially strong insurance company has a better chance of being around in the future to pay out claims, thus ensuring policyholder security. It’s also important to compare Whole Life Insurance quotes from several insurers to find the best rate for the same coverage.

Thorough research on insurers is crucial to confirm they are among the top-performing Whole Life Insurance companies. Investigating an insurer’s complaint index through the National Association of Insurance Commissioners website can provide insights into their customer service reputation.

Financial Strength Ratings

Financial strength ratings matter immensely for life insurance companies since these ratings reflect the insurer’s capacity to fulfill its financial obligations. And ensure the payment of significant benefits upon claims. Major credit rating agencies like A.M. Best, Fitch, Moody’s, and Standard & Poor’s assess the financial stability of insurance companies and their ability to fulfill long-term commitments.

Strong financial strength ratings suggest that a Life Insurance company is well-positioned to honour its policies, even many decades into the future, and provide policyholders with confidence in the company’s longevity and reliability. Financially strong insurers often have a conservatively invested portfolio and a history of paying dividends to policyholders, reflecting their commitment to financial obligations.

Comparing Quotes and Features

In the process of evaluating Whole Life Insurance policies, it’s essential to juxtapose quotes and features from a variety of insurers. The internal rate of return (IRR) of Whole Life Insurance policies’ death benefits is crucial to compare, as it reflects the efficiency at which premiums are used towards the expected death benefit.

When all other factors, like financial ratings and death benefits, are equal, the policy with the highest IRR at the lowest premium is often the better choice. Comparing different insurers’ policy illustrations, which forecast policy performance over time, is essential in determining the best Whole Life Insurance Policy. Working with an independent broker can be beneficial, as they can offer guidance and scenarios from multiple insurers to assist in a comprehensive policy comparison.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQ's

The main disadvantage of Whole Life Insurance is that it is much more expensive than Term Life Insurance and may have higher premiums. This can be a financial challenge for individuals who are young or have limited extra cash available.

The cost of a $1 million-dollar Whole Life Insurance Policy can vary based on factors such as age, health, and policy type. On average, a 30-year-old non-smoking male in good health can expect to pay around $954 per month for such a policy, which is significantly more expensive than Term Life Insurance. Pricing varies widely by insurer and policy design. It’s safer to mention a range instead of a fixed monthly number to avoid inaccuracies.

A whole life policy pays out the death benefit to beneficiaries upon the insured’s death, and it also accumulates cash value over time, which can be accessed through policy loans, withdrawals, or surrender.

You can make money with Whole Life Insurance by using it as an investment through methods such as withdrawing or taking a loan on the cash value, creating generational wealth, collecting dividends, or surrendering the policy if it’s no longer needed.

The key components of a Whole Life Insurance Policy are the guaranteed death benefit, level premiums, and the cash value component, ensuring a secure investment for the future.

The Whole Life Insurance monthly cost in Canada is influenced by various factors, including age, gender, health status, smoking status, coverage amount, and the insurance company’s underwriting criteria.

The Whole Life Insurance monthly cost is typically fixed for the duration of the policy. However, premiums may vary based on factors such as the insurance company’s financial performance and adjustments to mortality rates. Whole Life premiums are usually guaranteed and do not change once issued. “Company performance” affects dividends in participating policies, not the base premium.

To calculate the Whole Life Insurance monthly cost, you can use online calculators provided by insurance companies or work with an insurance agent who can provide personalized quotes based on your individual circumstances.

Yes, many insurance companies in Canada offer the option to pay Whole Life Insurance premiums monthly, in addition to quarterly, semi-annually, or annually. This flexibility allows policyholders to manage their budgets more effectively.

Some insurance companies may offer discounts on Whole Life Insurance premiums, such as preferred rates for non-smokers or discounts for bundling multiple insurance policies with the same provider.

Generally, the Whole Life Insurance monthly cost tends to increase with age, reflecting the higher risk of mortality as policyholders grow older. However, purchasing a policy at a younger age typically results in lower premiums. The cost is higher if you buy at an older age, but premiums are typically level after the policy is issued.

Yes, some insurance companies allow policyholders to change the frequency of premium payments to lower the Whole Life Insurance monthly cost. However, it’s essential to consider the long-term impact on the total cost of insurance.

The Whole Life Insurance premiums paid on a monthly basis are generally not tax-deductible. However, the death benefit received by beneficiaries is typically tax-free, making Whole Life Insurance an attractive option for estate planning.

Some insurance companies may offer discounts for policyholders who choose to pay their Whole Life Insurance premiums annually instead of monthly. This can result in savings over the long term.

Yes, policyholders have the flexibility to adjust their coverage amount, which can affect the Whole Life Insurance monthly cost. Increasing coverage typically results in higher premiums, while decreasing coverage may lower the monthly cost.

Life insurance comes in various forms, each with its unique way of providing financial protection. Let’s explore if life insurance is good for you or not..

Consider this: If you were to unexpectedly pass away, would your loved ones, like your spouse or child, face financial challenges in meeting expenses?

A. Yes, my absence would leave a significant financial gap for someone in my life.

B. No, currently, no one relies on me financially.

Select the option that best reflects your situation and discover if life insurance is the right choice for you.”

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com